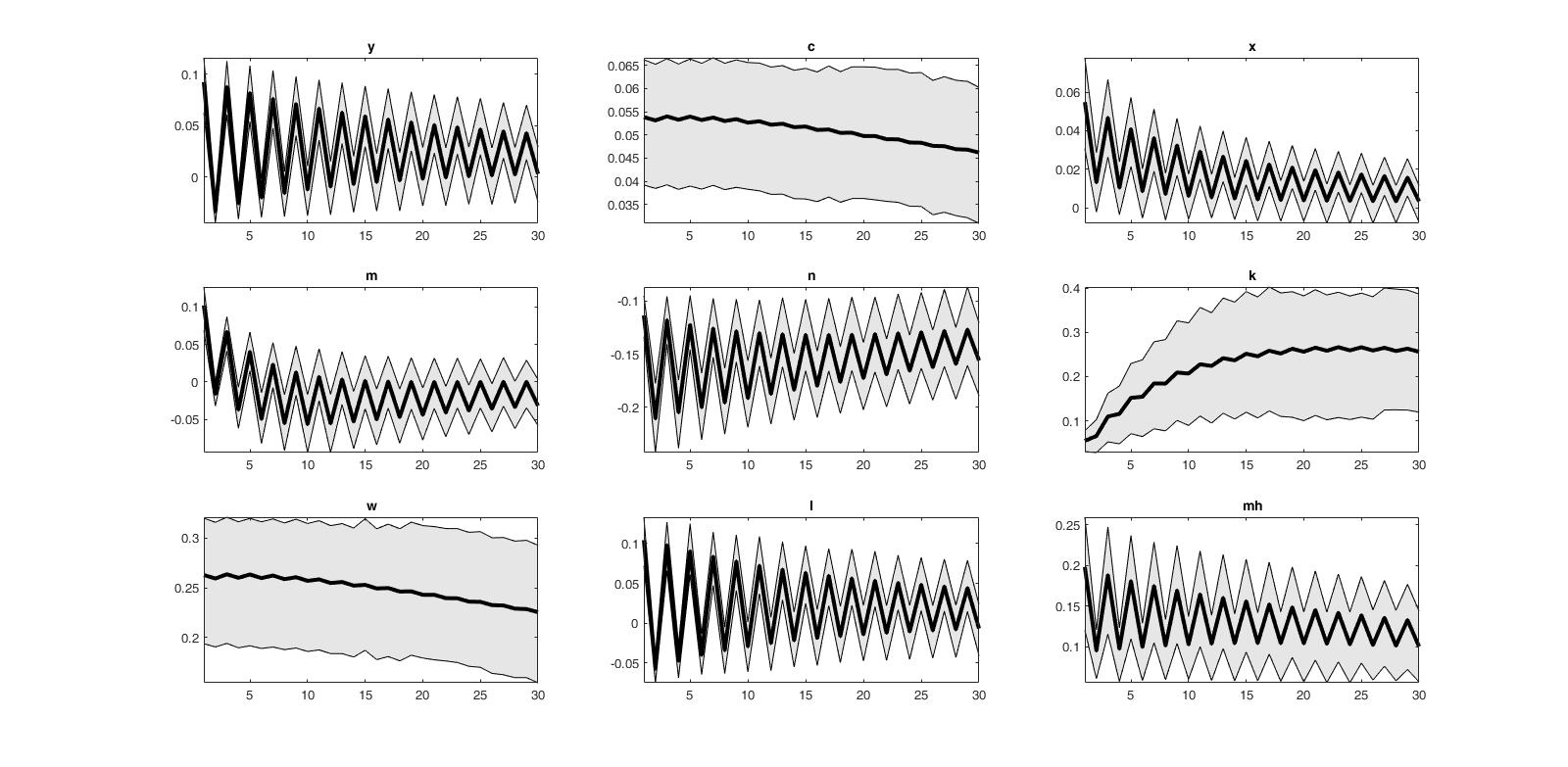

Hello. Some time ago, I encountered error “Blanchard & Kahn conditions are not satisfied: no stable equilibrium” when estimating the model, which was resolved by changing the Lambda parameter, but after estimation, I encountered diagonal and zigzag diagrams. What do you think is the problem?

Typically, the problem is a timing error somewhere that you “fixed” by changing a parameter to introduce a complex root. As a result your model shows oscillatory behavior.

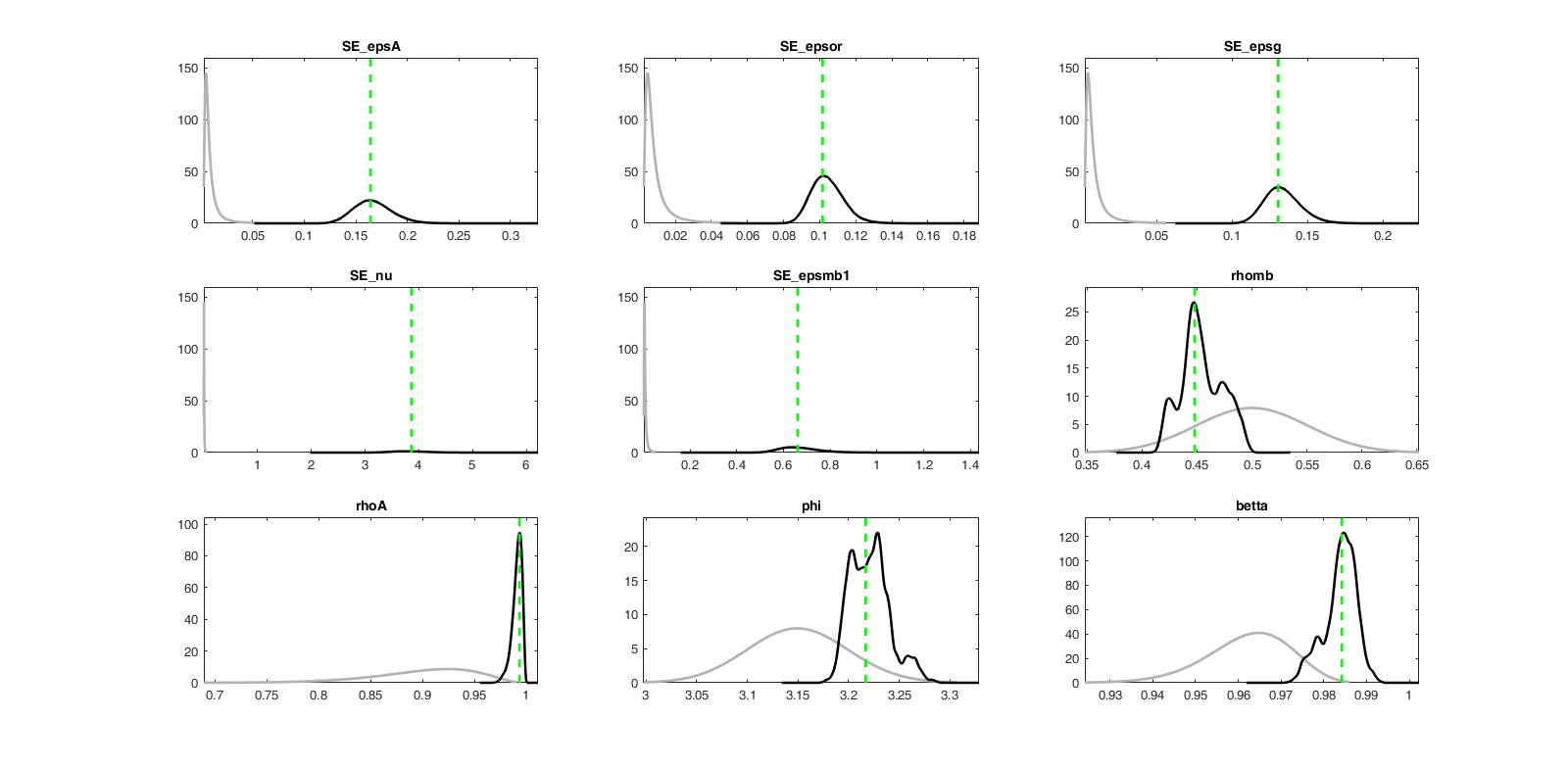

When I run the check command, the values of eigenvalue change with the change of Lambda and number of other variables. Do the results of this estimate depend on this?

My simulated model works and during estimation, for example, with Lambda = 1, the answers are normal, but with Lambda = 0, it shows oscillatory behavior in IRF. These problems were caused by adding mb1(bank liquidity) to the model and changes to the model. Do you think there is a timing problem?

It depends on which steady state values become negative. It’s obviously a problem if e.g. consumption or production were negative.

If the model works as expected for some parameter values but not for others, this suggests that you should consider the weird parameter region as a priori unlikely. You may want to restrict your prior to exclude them.

1.In the model, the steady state values for the deposit and domestic credit variables are negative.

2. I did not understand the second one. What exactly should I do? Can you give me some advice?