Dear all,

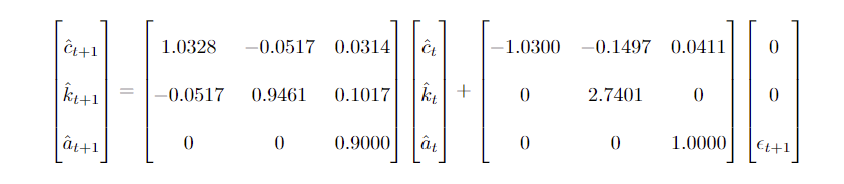

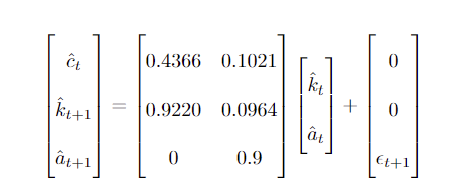

My question is that I have got the evolution function of a simple RBC model as in the picture, with c is consumption, k is capital and a is technology, and e is white noise, (all variables are log linearized). and thus I have got the policy function. So how do I calculate the theoretical covariance matrix based on these equations? Thanks ahead!

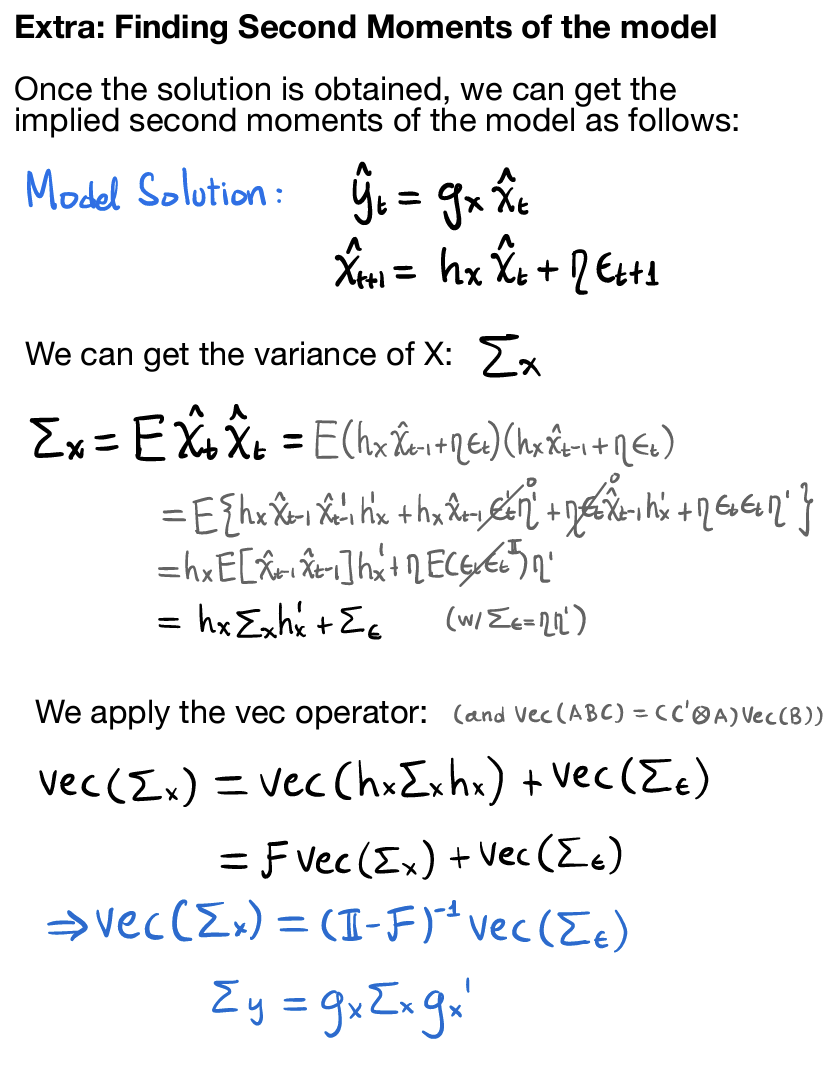

Yep, I first calculate the covariance matrix of (kt , at) by solving a matrix equation, and then I calculate the covariance of ct and (kt, at). But I have a new question, how do I calculate the autoregression matrix of these variables?

If the formula above is the solution to your model (endogenous as a function of states, a, k), then you can obtain the covariance matrix of the states, and the corresponding variance of your decision variables vector implied by the parameters you got: