Hi

I am not yet conversant with Dynare and I am running into issues trying to estimate the neoclassical DSGE model from del negro (2010). I am almost certain my steady-state model is incorrect

CanadaADTData.xlsx (23.3 KB)

but I am unsure how to improve it. I have included my dataset, where I log differenced output and hours worked. The error I am getting is as follows: Residuals of the static equations:

Equation number 1 : 0 : 1

Equation number 2 : 0 : 2

Equation number 3 : 0 : w

Equation number 4 : 0.037071 : r

Equation number 5 : -1.3297 : y

Equation number 6 : 0 : 6

Equation number 7 : 0 : k

Equation number 8 : 0 : 8

Equation number 9 : 0 : a

Equation number 10 : 0 : 10

Equation number 11 : 0 : gy_obs

Equation number 12 : 0 : gh_obs

Error using print_info

The steadystate file did not compute the steady state while simulation has been running.

CanadaADTData.xlsx (23.3 KB)

My .mod is as follows:

var y c k i h w r a A_tilda B gy_obs gh_obs;

/*

y - output

c - consumption

k - capital

i - investment

h - labor

w - wage

gy_obs- observed output

gh_obs- observed hours worked

r - rental rate of capital

a - technology shock

A_tilda - trend component of technology

B - exogenous preference shifter

*/

varexo e_a e_b; // the exogenous variables

// Parameters that need to be calibrated

parameters beta upsilon delta alpha B_star gamma Rho_a Rho_b sigma_a sigma_b;

%----------------------------------------------------------------

% 2. Calibration

%----------------------------------------------------------------

beta = 0.99; % Discount rate

upsilon = 2; % Aggregate labor supply elasticity

delta = 0.025; % Depreciation rate of capital

alpha = 0.66; % Output elasticity of capital

B_star = 1; % Exogenous preference shifter level

gamma = 1.03; % Trend growth rate

Rho_a = 0.01; % AR(1) technology shock parameter

Rho_b = 0.8; % AR(1) preference shock parameter

sigma_a = 0.01;

sigma_b = 0.01;

%----------------------------------------------------------------

% 3. Model

%----------------------------------------------------------------

model;

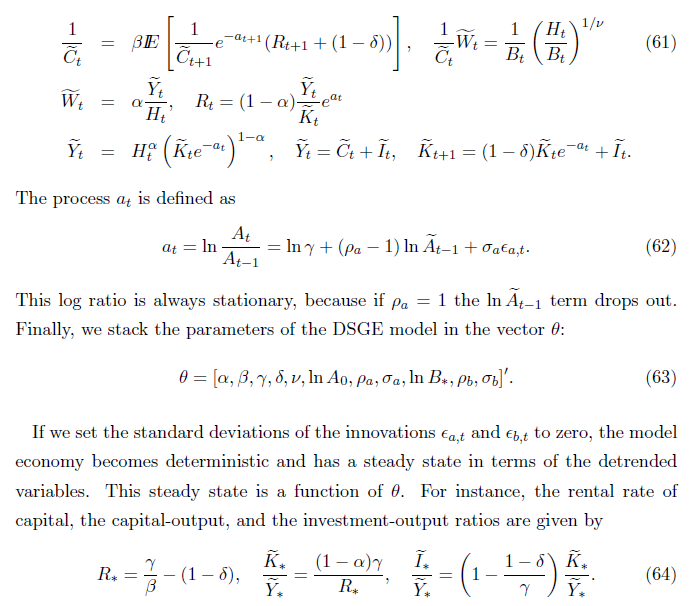

1/c = beta*((1/c(+1))*exp(-a(+1))*(r(+1) + (1 - delta)));

(1/c)*w = (1/B)*(h/B)^(1/upsilon);

w = (1-alpha)*y/h;

r = (1-alpha)*(y/k)*exp(a);

y = (h^alpha)*(k*exp(-a))^(1 - alpha);

y = c + i;

k = (1 - delta)*k(-1)*exp(-a) + i;

// Log-linearized technology shock process

log(A_tilda) = Rho_a*log(A_tilda(-1)) + e_a;

a = log(gamma) + (Rho_a - 1)*log(A_tilda(-1)) + e_a;

// Exogenous preference shifter process

log(B) = (1 - Rho_b)*log(B_star) + Rho_b*log(B(-1)) + e_b;

// measurement equation for gy_obs

gy_obs= y-y(-1);

// measurement equation for gh_obs

gh_obs= h-h(-1);

end;

varobs gy_obs gh_obs; // output and hours worked

steady_state_model;

// Technology Adjustment (a = log(gamma) in steady state)

a = log(gamma);

// Exogenous preference shifter process (B = 1 in steady state)

B = 1;

A_tilda=1;

// Define steady-state values for h, k, and y

h = 1; //

k=1;

// Production Function (using k)

y = h^alpha * k^(1 - alpha)* (1/gamma)^(1-alpha);

// Wage Equation

w = (1 - alpha) * y / h;

// Labour Supply and Demand Equation (c in terms of w and h)

c = w / h^(1 / upsilon);

// Interest Rate Equation (r in terms of beta, gamma, and delta)

//r = (1-alpha)*(y/k)*gamma;

// Euler Equation (R in terms of gamma, beta, and delta)

r = (gamma/beta)-(1-delta);

// Capital Accumulation Equation (i = y - c)

i = y - c;

// Now, calculate k from the investment equation:

//k = i / (1 - (1 - delta) * (1 / gamma));

// Resource Constraint (y = c + i is already ensured by the equation above)

// Define the steady-state values for variables

k = i / (1 - (1 - delta) * (1 / gamma));

// Measurement Equation for Output Growth (gy_obs)

gy_obs = 0;

// Measurement Equation for Labour Growth (gh_obs)

gh_obs = 0;

end;