When I implement monetary policy news via simult_ function I got some weird IRF which I think might be due to the endogenous response of the Taylor rule. In fact what I have in mind is a known shock at say period true but the interest rate might stays peg up to when the shock happen.

Any ideas on how I cloud shut down the taylor rule before the shock?

Thank you for you answer professor

For the anticipation phase in my mind the nominal interest rate should stay at the steady state or zero and only react when the shock materialize (some kind of peg and then revert to the Taylor rule)

I don’t know if I’m doing it the right way to have what I want?

I would like to have a forward guidance experiment. At T0, the central bank credibly announces a one-period increase in the nominal interest rate, to be implemented in period T, and commits to keeping the nominal interest rate at its initial level (That I want to normalize to 0 or the steady state level) between periods 0 and T-1, independently of the evolution of inflation and output gap. after the shock at T+1 it restores the Taylor rule.

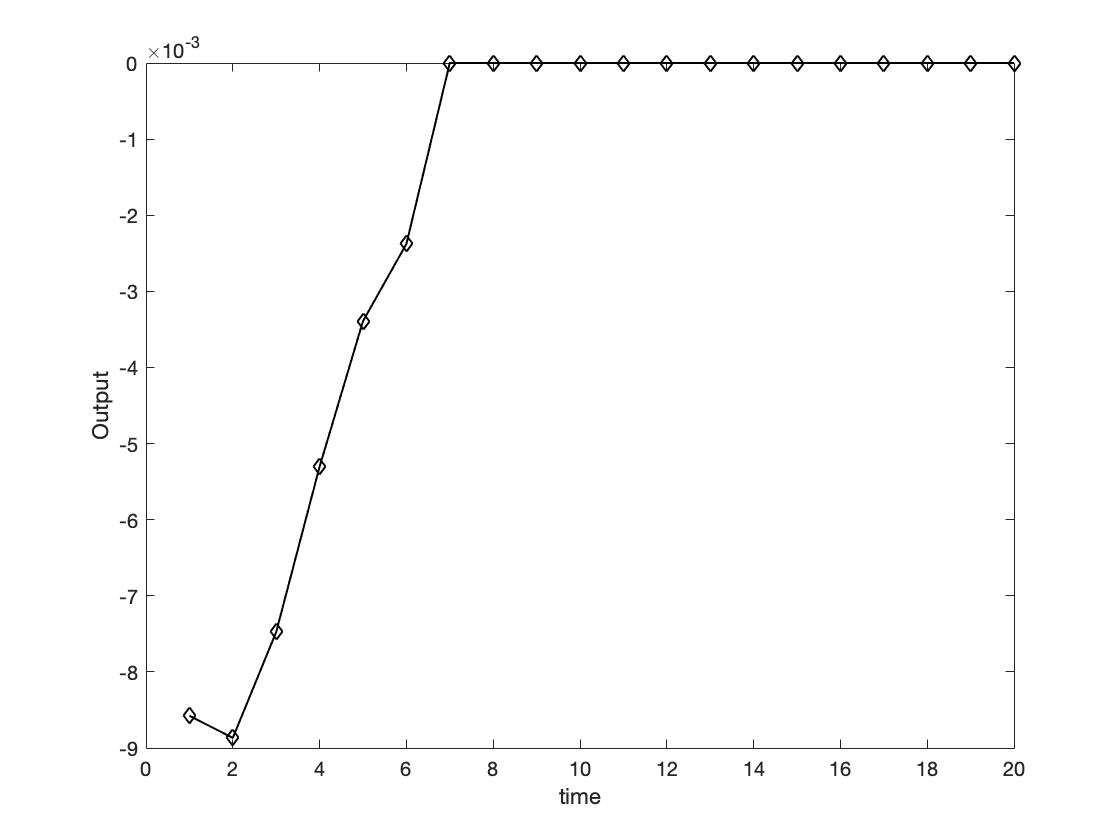

Thank you very much. I finally came out with a “solution” from this topic @ Taylor Rule and Forward Guidance suggested by @valerio88 . I completely shut down the Taylor rule using R=R_ss*exp(nu).

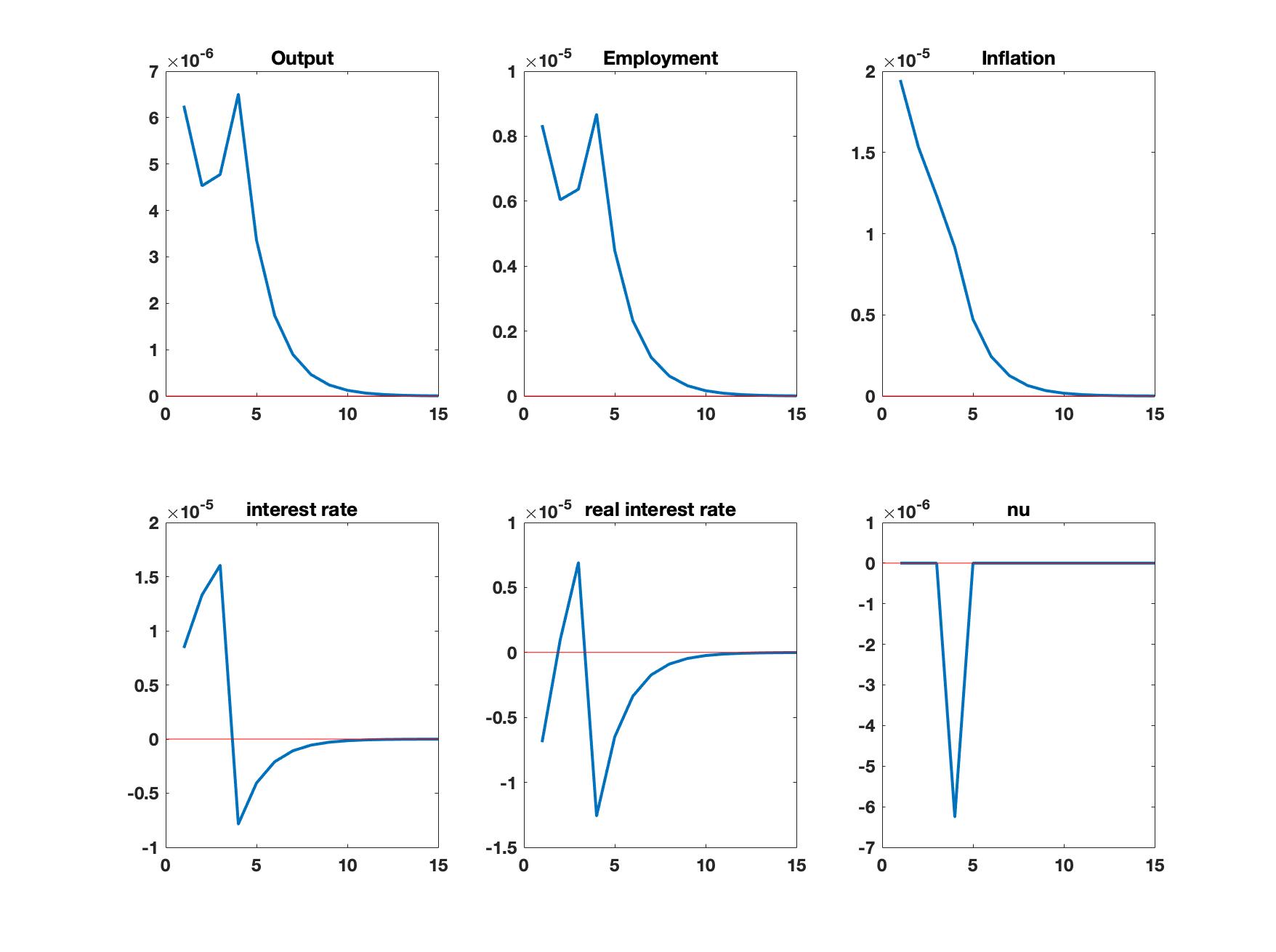

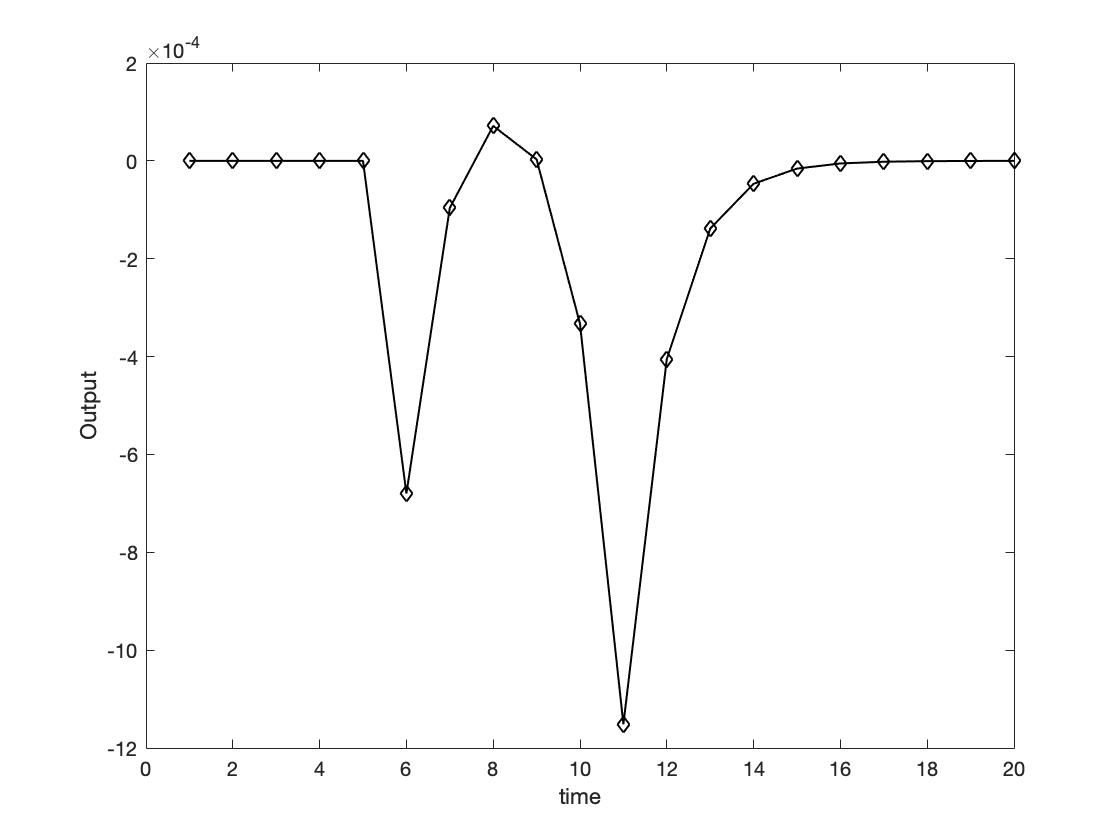

1-The model find a solution in this context with the Rotemberg setup (figures below) but fail to solve the perfect foresight with Calvo setup. Do you have any idea of what may cause this problem?

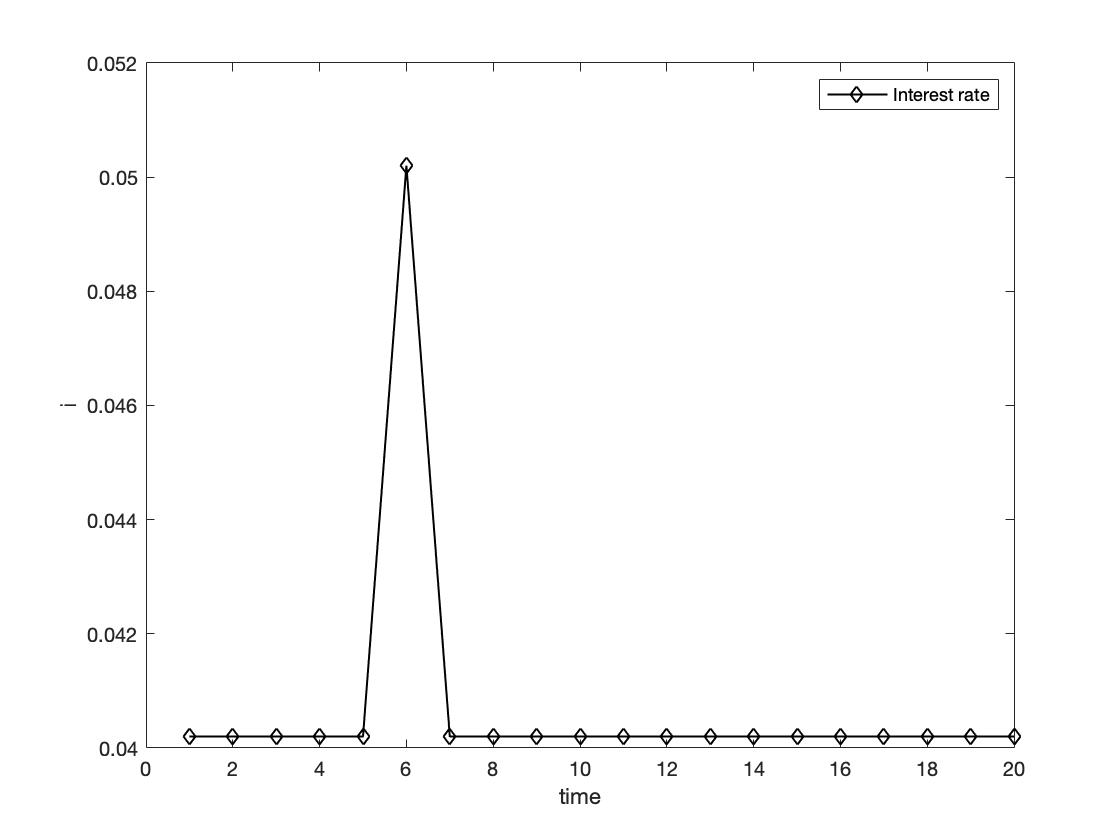

2-When I try the same simulation with the Taylor rule R/R_ss=(R(-1)/R_ss)^rho_r*((exp(pi)/exp(pi_ss))^(phi_pi)*(Y/Y_ss)^(phi_y))^(1-rho_r)*exp(nu) , the model run in both specification but there is no anticipation movement (figure below). Is this normal?

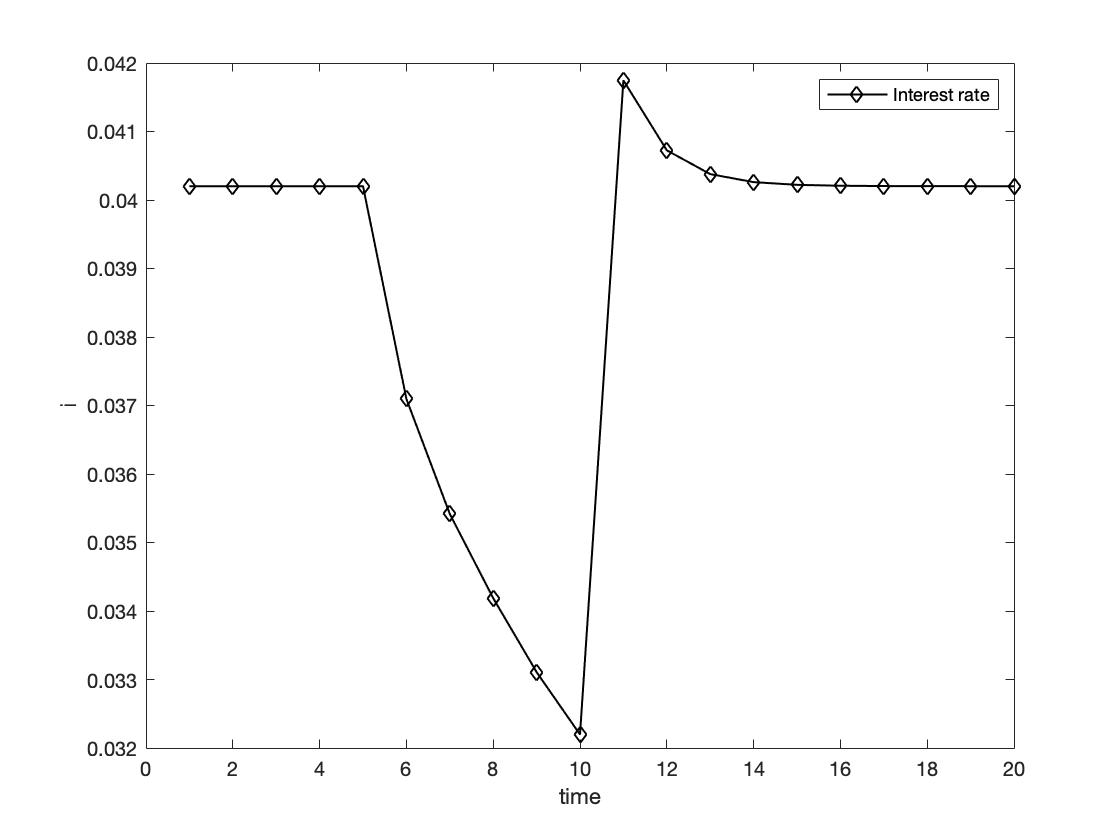

I still don’t understand what you are doing. It seems you are permanently pegging the interest rate. That violates the BK conditions and typically results in non-converging simulations. Usually, you have the central bank reverting to the Taylor after the forward guidance period.