That looks like a numerical overflow due to your numbers being to big and disparate in size. Zero profits is a result of constant returns to scale and competitive factor markets.

@jpfeifer thank you, that was my first hint. I actually have a way bigger model with different industries, and more inputs (energy, materials). All inputs are very different in size, which ultimately lead to Dividends being non zero. I departed from a super simple model, and had the same because of this size problem.

I actually do not mind having dividends. Since I cannot just simply resolve the problem, I was careful in adding the dividends to the budget constraint of households owning the firms.

That is not valid. These dividends result purely from numerical error. You need to appropriately normalize your model variables to circumvent this issue.

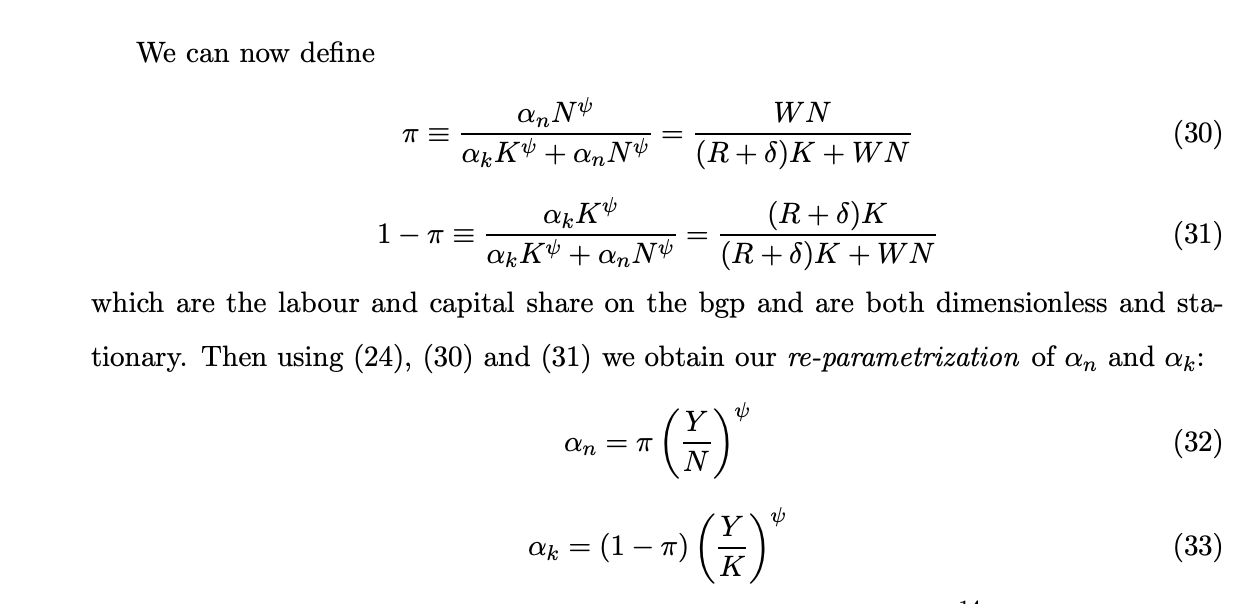

What I did is simply parametrize the parameter shares from national account data for capital, labor etc following Cantore and Levine reparametrization:

If then, I multiply the per capital value of K by total labor, I end up with the right value for K used in this sector. But I just spotted an issue in the calibration. In resolving this issue, I end up finally with zero profit. However, I’ll still get at SS the value for K_f and KL that you just mentionned.

But that should allow you to normalize. You can measure capital in dollar or millions of dollars. Similarly, you can measure hours in hours or in thousands of hours.

What do you mean with big? You could even just normalize GDP per capita to 1 and work with shares of total GDP for other data. Total investment per capita would then be about 0.2.

Regarding the Cantore and Levine reparametrization of CES consumption functions, the distribution parameters add up to 1, while for production functions they do not restrict the distribution parameters to add up to 1.

Can I do the same thing for CES consumption function with different goods, where I do not restrict the distribution parameters to equal to 1 ?