Is it because the output gap, inflation rate, and the price level are all just the zero line? Thus, they do not respond at all to monetary policy shock if monetary policy is optimal?

In the paper by Stéphane Adjemian, Matthieu Darracq Pariès, and Stéphane Moyen, for example, there are no results for monetary policy shock under Ramsey model. I expected this, but is my reason above correct?

So that IRFs of monetary policy shock (from a baseline model with Taylor rule) can just be compared with the zero line (which is IRFs of monetary policy shock from a Ramsey equilibrium)?

When you are computing the optimal policy under commitment (Ramsey olicy), you are looking for the best possible policy. Why would you add a random shock to it?

Oh, I see. Thanks! So in evaluating policies (maybe even including suboptimal policies), we do not need to add a monetary policy shock?

Here is my problem though: (maybe, not a problem, but my lack of knowledge)

-

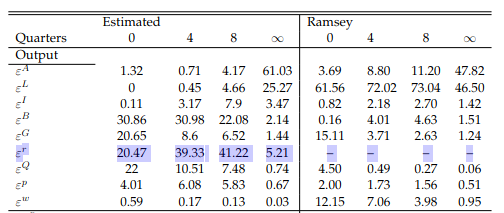

Using an estimated DSGE model and simult_, I have found that cost-push shocks are not important for fluctuations in output and inflation for economy A.

-

Now, I can get Ramsey optimal policy results under a cost-push shock. But cost-push shock itself is not important for the economy of interest (i.e., economy A).

I guess we are only using cost-push shock to compute optimal monetary policy numerically so it does matter, yeah?

If we had an optimal monetary policy in a closed-form expression, then perhaps we can compare monetary policy shocks under optimal policy and under sup-optimal policy? Thank you.

In most cases, optimal policy can’t be computed in close form solution. I miss the point of have a monetary policy shock under optimal policy, because the resulting policy wouldn’t be optimal anymore.

You want to compare the effect of an exogenous shock when using different policies. You don’t want to study the effect of a shock that modifies a policy

Thanks for the clarification. I think I misunderstood this statement from Gali (2015) chapter 5.

“The (optimal) policy (i.e., in chapter 4) requires that the central bank responds to shocks so that the price level is fully stabilized”. Of course, Ramsey’s optimal policy does not require full stabilization, but if I may ask, the shocks in that statement exclude monetary policy shocks, right?

And if I understand, adding a shock to an optimal rule will make it not optimal because inflation and output gap would no longer be zero, for example, under full price stabilization?

We add monetary policy shocks to a non-optimal feedback rule. For Ramsey, you replace this rule be an optimal response of the central bank. The rule would never include random shocks as they will not be optimal. In fact, the interpretation of monetary policy shocks is often that they are policy mistakes.

How does the feedback rule work though in the real world, if I may ask?

In the model,

- monetary policy shocks affect the interest rate

- interest rate affects inflation and output expectations

- expectations affect inflation and output

- inflation and output then affects interest rate (feedback)

In the real world,

I sometimes think monetary policy shocks (resulting from, say, exogenous exchange rate depreciation or some exogenous event)—affect expectations and hence output and inflation. Output and inflation then affect interest rate (the policy). So like the feedback is not really observed in the real world unless the monetary policy committee meets more than once in a quarter.

For an annual model, the feedback rule seems plausible in the real world as the monetary policy committee meets many times in a year. Are my thoughts correct? I asked a similar question in an earlier post…so I will delete that.

There are two aspects to consider here:

- The short-term interest rate in quarterly models is usually not the policy rate, but some money market rate that can indeed react immediately (e.g. the effective federal funds rate).

- most feedback rules contain a monetary policy shock that captures deviations from the pure feedback rule. If the monetary policy committee meets too late, it will show up as a shock given the variables on the right-hand side.

Like even if the monetary policy committee does not meet or meets too late, the effective federal funds rate can still change (via the shock), right? If I understand…

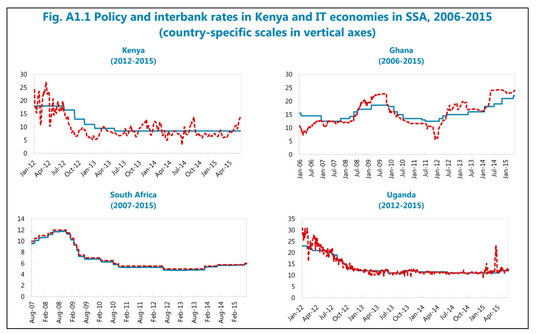

Also, it seems the effective rate (i.e., the average overnight interbank rate) can deviate quite substantially from the policy rate itself.

For the US, the effective rate closely follows the policy rate like in South Africa below…but for countries like Ghana, it is not the case. In this case, is it still better to use the effective rate to estimate the model or the actual policy rate? Maybe policy rate since policy rate is typically used to estimate reaction functions in reduced-form models for Ghana. Or better, look for a market rate that reacts immediately to the policy rate…but if none exist then use the policy rate?