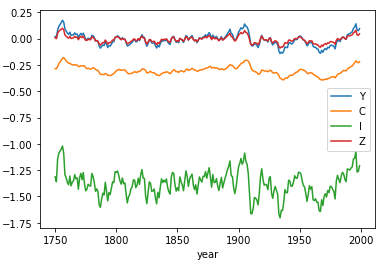

When I detrend log of observed data with hp-filter algorithm, fluctuations of the series are typically around zero. But when I write a model in dynare in levels, take logs of the variables, and use hp_filter option, the simulated series does always fluctuate around zero. I know the mean does not matter much, kind of. But why the fluctuations of some model variables are sometimes not around zero, here C and I.