Dear all,

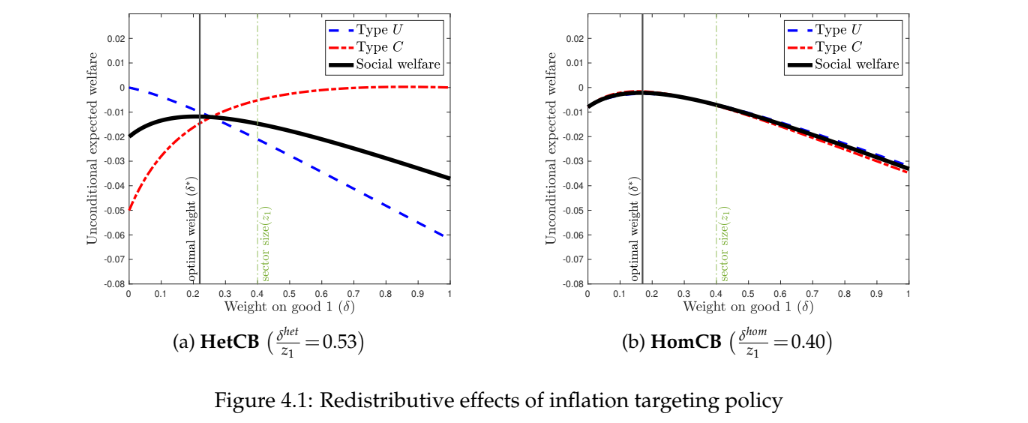

I would like to ask for advice on how to conduct a welfare analysis in Dynare. I am trying to replicate the results from “Optimal Monetary Policy under Heterogeneous Consumption Baskets” by Seunghyeon Lee. I have derived the entire model and implemented the log-linearized (first-order approximation) system of equations in Dynare. However, I am currently unable to reproduce the graph where delta is the parameter on good 1 in the Taylor rule.

The author defines welfare as “the expected welfare of each type (measured as deviations from the deterministic steady state).” Could you please advise me on the following:

- Which order should the utility function be in the

.modfile?

// log utility

U_U = log(cU_level) - nU_level^(1 + varphi)/(1 + varphi);

U_C = log(cC_level) - nC_level^(1 + varphi)/(1 + varphi);

// First order approximation of log utility

U_U = cU - nU_level^(1 + varphi)*nU;

U_C = cC - nC_level^(1 + varphi)*nC;

// Second order approximation of log utility

U_U = cU - nU_level^(1 + varphi)*nU -0.5*cU^2-0.5*varphi*nU_level^(1 + varphi)*nU^2;

U_C = cC - nC_level^(1 + varphi)*nC -0.5*cC^2-0.5*varphi*nC_level^(1 + varphi)*nC^2;

Lowercase letters denote deviations from the steady state.

- Which order should I use when running the simulation? Could you please check if this is correct?

stoch_simul(order = 2, periods=1000, irf = 0);

- I do not need to implement the the system of equations with the second-order approximation manually in Dynare, right?

I calculate the sum of discounted utilities in a separate .m file, but the result I get is not correct.

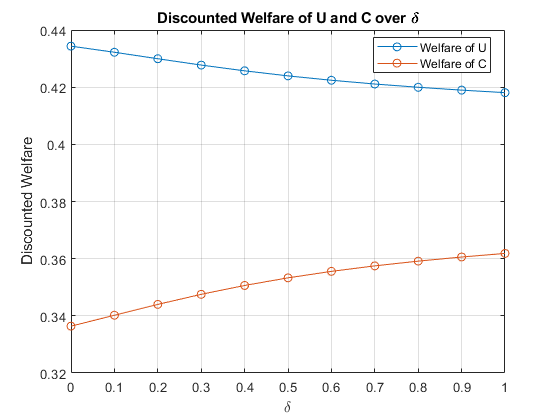

This is my result for the HetCB case.

Thank you very much in advance.