I constructed a model based on Iacoviello(2010) Housing market spillover … , and have some modification.

I exclude monetary sector so all variable presents in real term. I alter patient agent’s housing consumption that patient agent can only rent houses from agent2 , to see how houseprice and houserent act under borrowing constraint.

Some IRFs seems reasonable, but non-durable output(yc) and housing output(IH) seems weird, fltctuates up and down, a little like a oscillating shape, and some variables don’t come back to zeros.

I’ve check model several times but I could not found any mistake from timing and paras. Wish someone can give me some direction.

Here attach a code for log-linearized model, Thank you very much.model.mod (6.9 KB)

Your IRFs do not look unusual. Some overshooting is quite common and all IRFs come back to 0 in reasonable time

Maybe I care too much about the tail that can hardly to perfectly match to zero.

Thanks a lot for your answer !!

If your model features capital, the households will consume just a little bit more out of the capital stock for a long time due to the permanent income hypothesis/consumption smoothing.

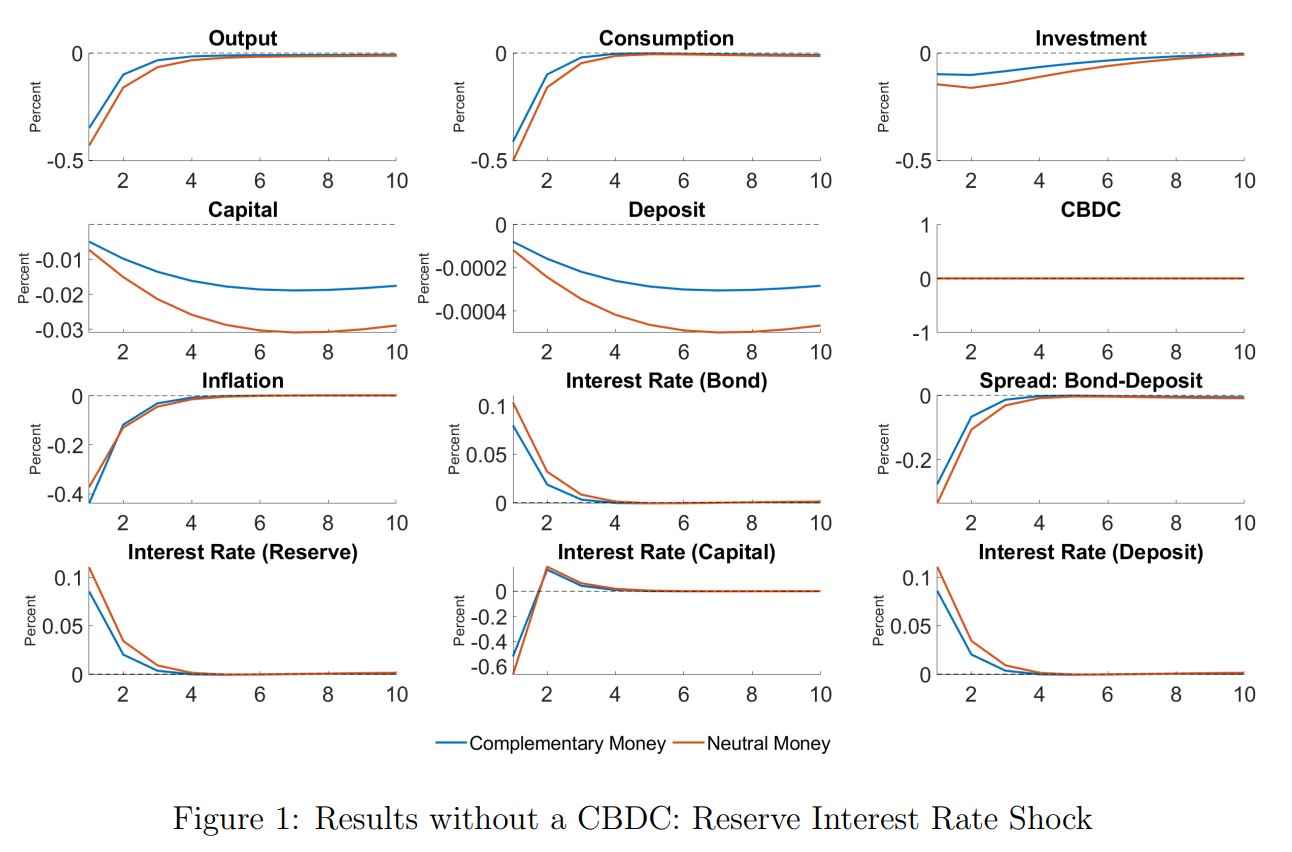

Good afternoon, I am trying to replicate a paper, and specifically, the Impulse response function graphs where there is a central bank reserve interest rate shock.

My dynare code produces these graphs:

y - output, c - consumption, i - investment, k - capital, d - deposits, i_s - bond rate, r_k - capital return, i_d - deposit rate, pi - inflation.

The original paper’s IRF graphs are as follows:

What bothers me is that except for output and inflation, other variables’ graphs do not match exactly. Is there a way to tell what is exactly causing this mismatch? Is it timing issue, or parameter misspecification? Or wrong initial values setup?

Thank you. My dynare code and the original papers are attached.

no_CBDC.mod (1.3 KB)

Central Bank Digital Currency and Transmission of Monetary Policy 1.pdf (1.8 MB)

Replicating papers is hard. You can check for mistakes and inconsistencies but often the only way to proceed is to get hold of the replication files.