Hello, everyone!

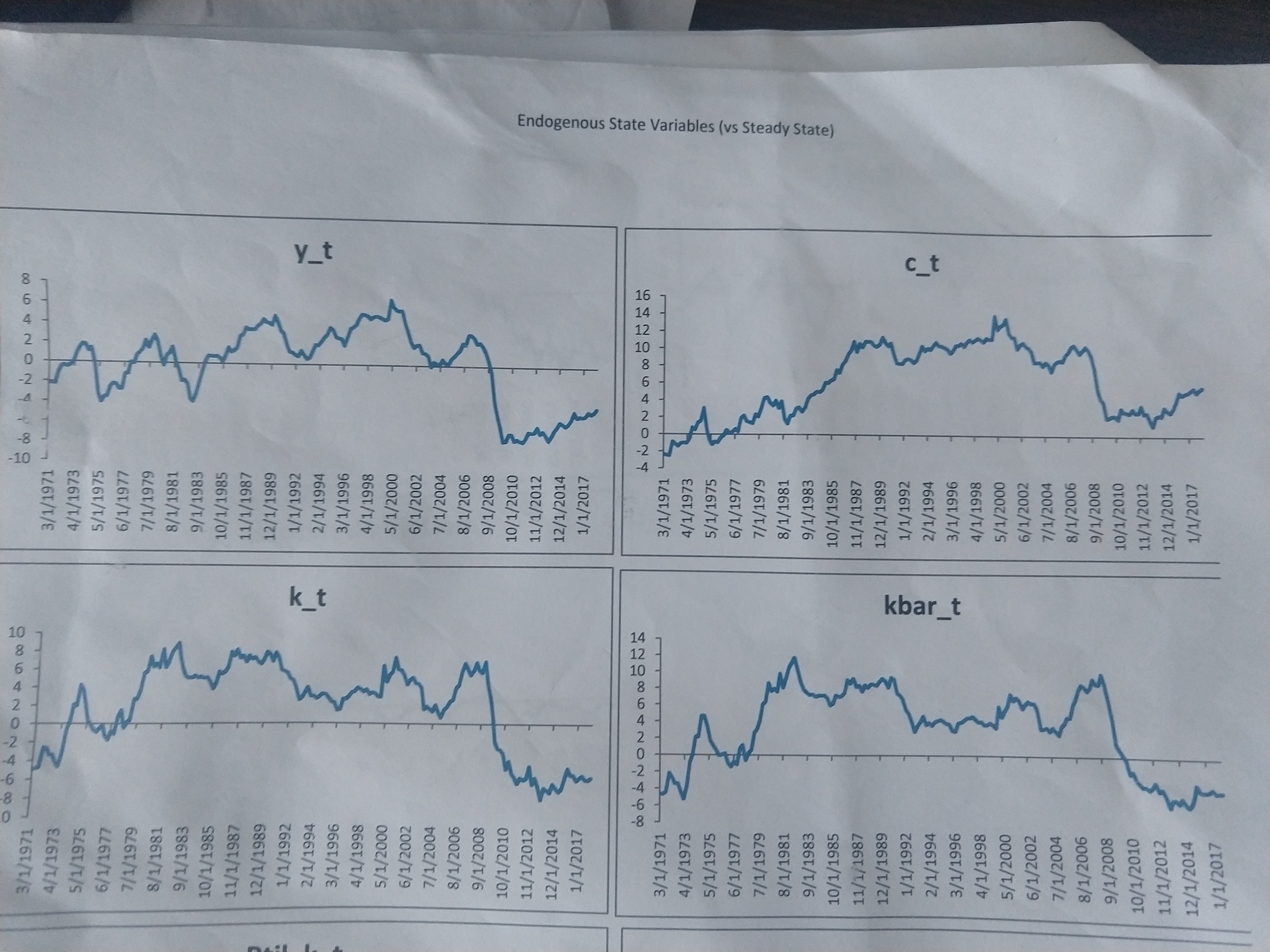

I have been trying to estimate\simulate the time-series of deviation of endogenous variables from their steady states based on medium-scale DSGE model (written by Smets and Wouters (2007)). I want to compare how model generated variables perform relative to the real data. ‘Figure1’ attached to this message summarizes what I am trying to achieve. I thought ‘Smoothed Variables’ obtained after estimation works for that purpose. However, they are exactly the same as observable variables.

Therefore, I simulated the model right after the estimation, with the command stoch_simul(order=1, hp_filter=1600, periods=216). I chose the ‘periods’ option to be 216 because I want to study the data from 1966Q2 to 2020Q1. I do not know whether I am doing right or not. Could somebody tell me if I am in the right direction?

Also, I found some discussions about using the posterior-function after estimation to simulate the endogenous variables. Therefore, I am trying to obtain simulated variables by using posterior-function. However, I got the following error message:

“EXECUTE_POSTERIOR_FUNCTION: Execution of prior/posterior function led to an error. Execution cancelled.

Brace indexing is not supported for variables of this type.”

I do not know what is the error. Could somebody help me with this? Also, is there any difference between the use of stoch_simul option and posterior_function after estimation command? I mean do we get different results? I have attached the complete file as an attachment to this question.

Thank you very much for your time and help.

Regards,

Niraj

SmetsandWouters(2007).zip (40.2 KB)