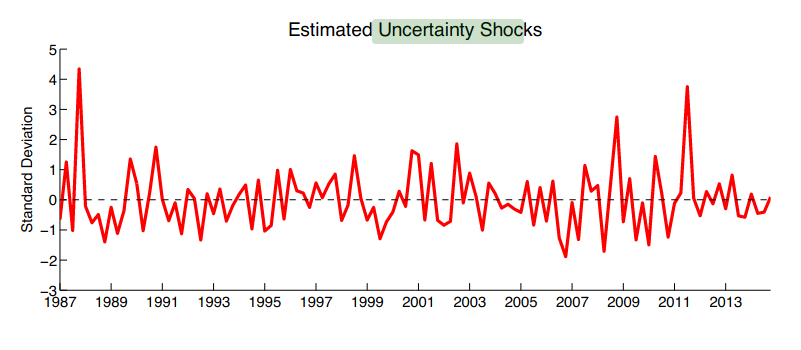

Hi Prof Pfeifer, may I revive this thread? It seems uncertainty shocks (I guess same as time-varying stochastic volatility per the title of this thread) can be used to identify sources of a cluster of small or large volatilities, right? For example, by allowing time-varying volatility for all structural shocks in a given model, one can check the estimated uncertainty shocks for which ones had, say, a lower volatility over the period of interest, i.e., if you are seeking to explain something like sources of the great moderation.

In other words, checking whether bad (good) luck caused a given period of high (low) volatility (with many shocks as candidates) using Basu’s approach is appropriate, right? Like no concerns for identification issues here, I guess.