I have estimated a DSGE model (bayseian) in Dynare and I want to find out what the probability of a given shock is? How should I approach this? The shocks follow a standard AR process where the innovation is i.i.d. normal distribution. But I cannot make any meaning of it if I use a normal distribution to calculate the probabilities. The size of the shocks (1 std) is simply too small to have a significant probability when comparing it to a normal distribution (0,1). For instance, if I want to calculate the probability of a foreign interest rate shock which is large enough to decrease inflation by 1 per cent.

Could you elaborate what the problem is? Normally, you would simply compute the number of standard deviations needed and then read of the probability from the CDF of the standard normal distribution.

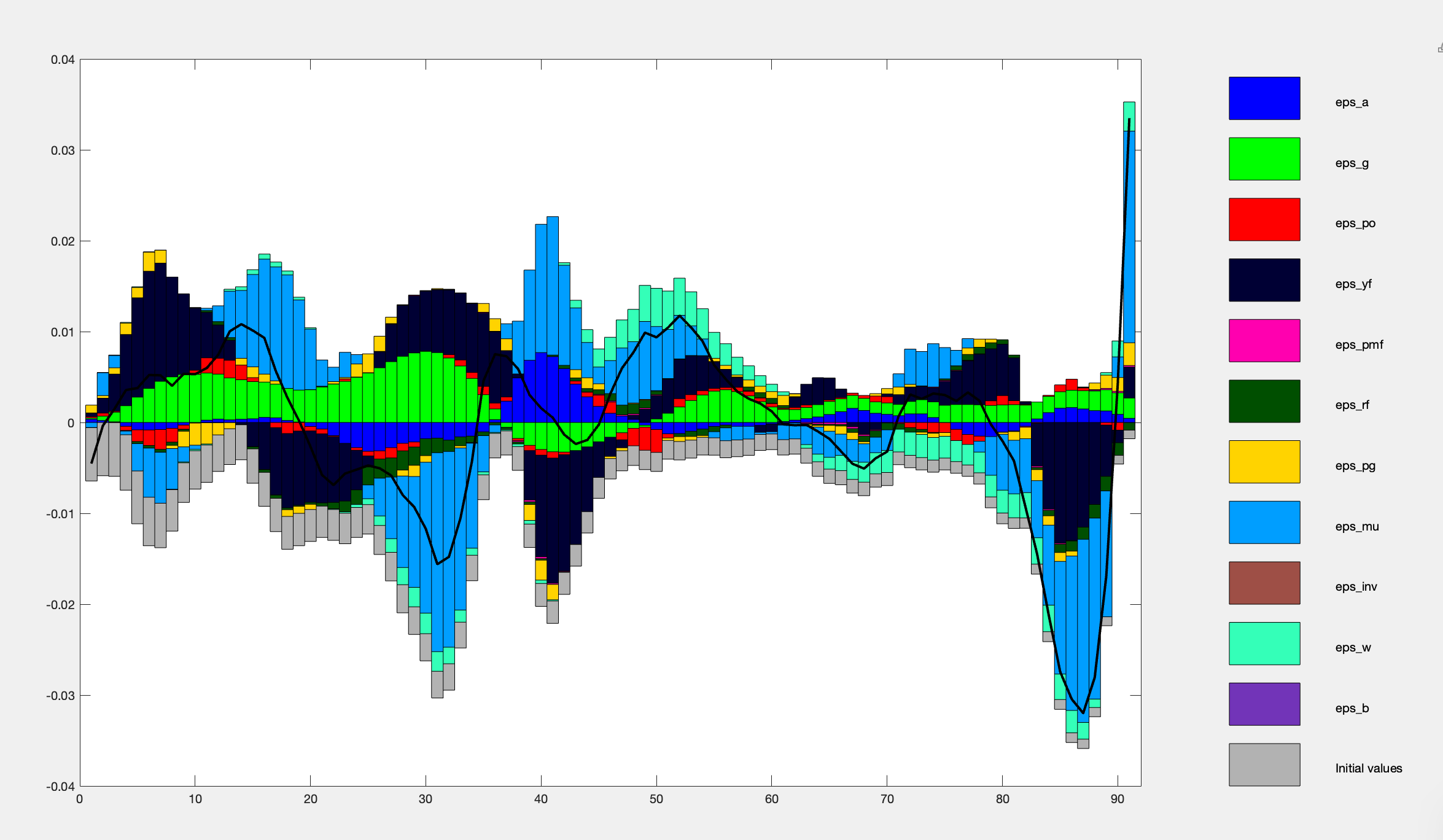

Thanks for the quick response. That is also my understanding of it. I tried using this approach to find the probability of a ‘disastrous event’, but the effect of the shocks in my model is just too small to reach the levels of a disastrous event - the probability for the event goes to zero. The thing I am confused about is how the model can attribute the shocks to have an effect of 1 pp. on inflation when I am looking at the historical decomposition. Is there a good reason for this?

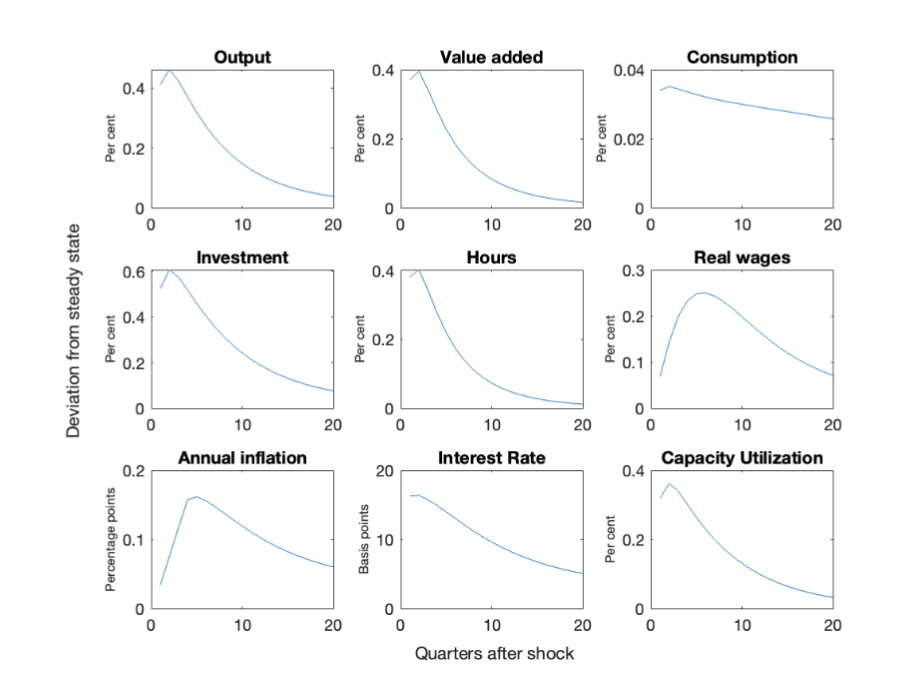

For instance, I have calculated the following variance of a foreign demand shock

var eps_yf = 0.01708^2

The effect of a 1 std foreign demand shock is 0.05 pp on inflation when I look at the IRF.

When using the CDF of a standard normal distribution, the event of a foreign demand shock to make inflation increase by 1 pp is basically zero.

When I look at the historical decomposition, the world demand shock explains a 1 pp deviation from the trend in inflation around COVID-19 (seen in the figure as black columns around 86 quarters)

I am also interested in the topic.

To compute the probability of the shock, I compute the cdf of the sequence of the released shock… Am I right?

p_risk = gamcdf(oo_.SmoothedShocks.eps_risk,0.001, 0.002);

(Given the fact that the shock has been estimated with a Gamma ,0.001, 0.002)