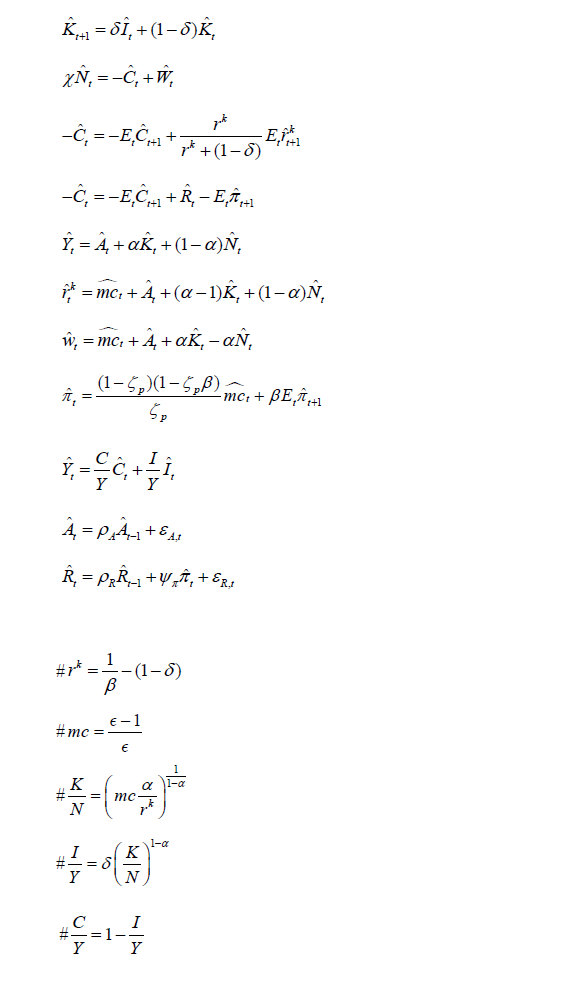

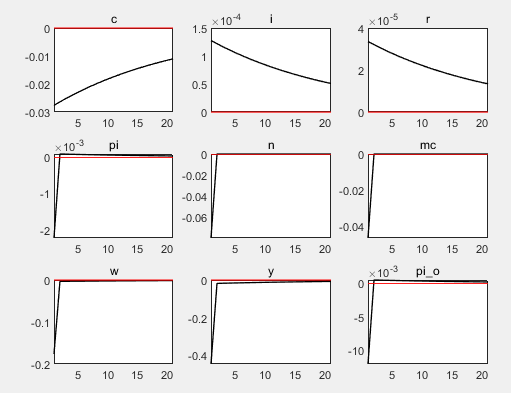

@DAXIA Your results look very strange. Is this a first order approximation? @jordima I don’t immediately spot anything strange. Are you sure this is not just regular economic behavior without investment adjustment costs?

Pretty much every model fit to the data that includes capital has some form of adjustments costs. The missing empirical hump-shape is often given as the reason for that.

Hi Jordima!

May I ask did you solve this problem (NK model with capital stock but having an undesirable IRF)?

I have made a similar model just now and confronted the same problems. And I am also wondering why most of the NK models without capital stock and any forms of investment.

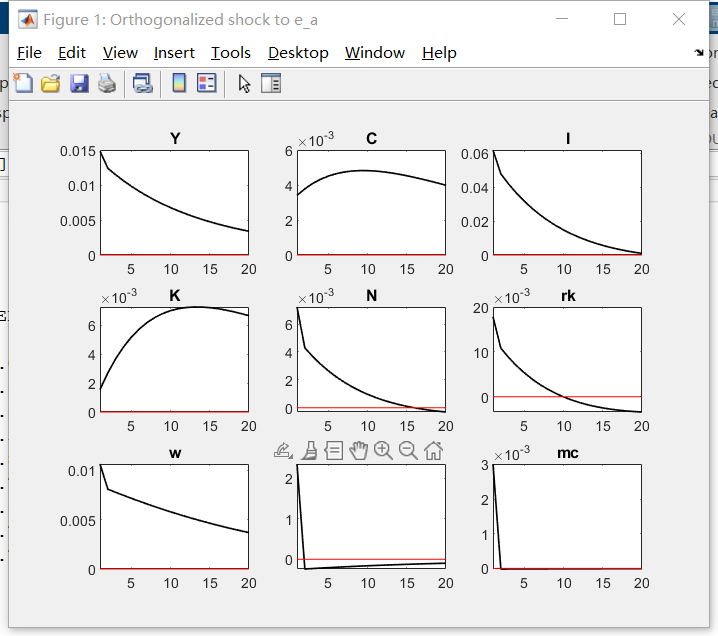

I added investment adjustment costs into the model and got an undesirable IRF.

@jpfeifer

Dear Professor Jpfeifer,

I have added investment adjustment costs into NK model, while it didn’t make any difference. May I ask how to improve this situation?

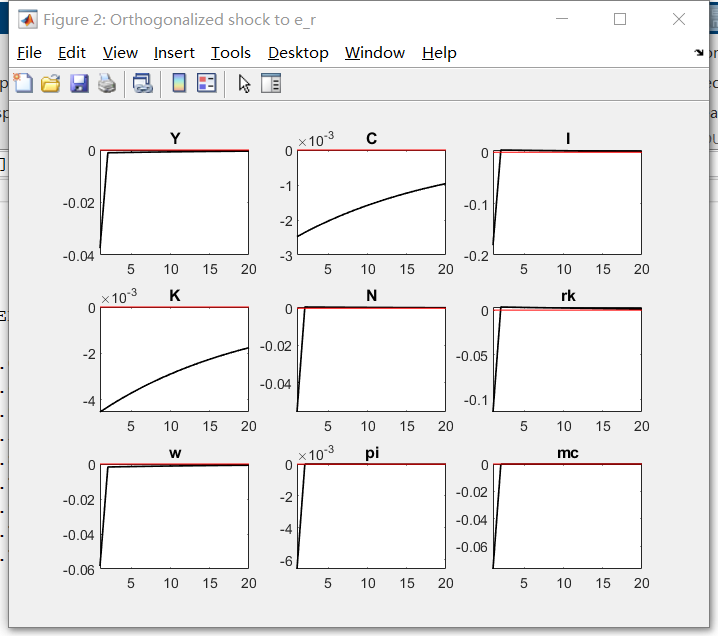

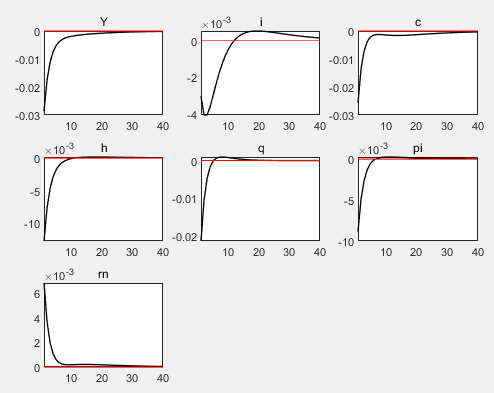

Professor Jpfeifer, it seems that I have solved this problem.

Your reminding is very important to me. I tried to change the objective function of intermediate firms, and the IRFs turns much smoother, and they conform with the expectation.

There are two points, I think.

If a slow convergence speed is needed, then letting the household contain C-gamma*C(-1) might be useful.

To let the intermediate firm as the sector of accumulating capital stock (and there is an adjustment cost of investment) might be useful for making IRFs smooth