Hi everyone, I am a student in DSGE.

I have a confusion of my modeling.

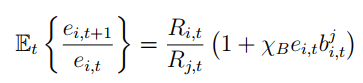

I build a uncovered interest rate parity:

de(+1) = r_h - r_f + chi_B*b;

(linerized, in line 174)

And I build a managed floating exchange system in a expansion taylor rule:

r_h = rho*r_h(-1) + (1-rho)*(phi_r*pi_h + phi_rer*de) + e_r_h;

( ‘phi_rer’ is the parameter of exchange rate, and ‘de’ means ‘e/e(-1)’ , in line 163)

like this:

Is it repetitive modeling? In other words, does this result in a single mechanism between interest rate and exchange rate being modeled repeatedly?

Thank you very much!

Here is the code:

nk2c0104.mod (8.0 KB)