What is the difference? What role does the term (1-\phi_R) play?

If I have a non-linear stationary model (i.e. there is no variable P_t only \Pi_t), is it possible to specify a price level targeting rule? Or if I would like to analyze annual inflation, how could I do it? since annual inflation would imply P_t/P_{t-4}, and again, P_t is absent in my model.

Searching in the forum I found that a possible solution would be to specify in the model something like: P_t=P_{t-1}\Pi_t

But given that in my model the steady state inflation is 1.0075, I don’t know what the value of P_{t} would be in the steady state for the residuals of this equation to be zero.

The first version explicitly shows that the interest rate is a convex combination of a smoothing term with weigth \phi_R and a feedback term with weight 1-\phi_R. The second version is equivalent if you adjust the exponents to reflect \tilde \phi_Y=\phi_Y(1-\phi_R).

I am not sure I understand the second question. If there is steady state inflation, how can you have a price level target?

Regarding the inflation that I specified in the Taylor rule above, I have \Pi_t=P_t/P_{t-1} and therefore \Pi =1.0075 which is a quarterly target value, but if instead of having the quarterly inflation, I would like to have the annual inflation in the taylor rule, i.e. \Pi^{annual}_t= \frac{P_t}{P_{t-4}}, how should I introduce it in dynare since the model doesn´t have the variable P_t? should I build it as

I have a general question regading the Taylor rule. Do the inflation and the gross interest rate move in the same direction in the NK DSGE models?

For example, when we have the following equation in a nonlinear model in Dynare:

Having a contradictionary monetary policy shock (rise in R) will end up in increasing in the inflation through the above Taylor rule or the inflation can drop and move in the opposite direction?

Thank you so much for your reply.

I have some difficulties in understanding the mechanism and it would be great if you can help me with that. I have already read your post here:

If we consider a simple taylor rule such as R_t/R_{ss}=(Π_t/Π_{ss})^{ϕ_Π}S_t

A change in EPS_R in the above equation, means a contradictionary mondetary policy shock as its sign is positive in the equation and it definitely increases the real interest rate (r_t=R_t-\Pi_t) no matter if we can see a posive or negative nominal interest rate (R_t). Is this true?

The IRF of Real Interest rate with respect to the above shock is negative (I added the following equation in my nonlinear model : r_t=R_t/\Pi_{t+1}) in the model. Is this OK or it must be positive as the result of the contradictionary policy?

I know in the NK models, the Euler equation pins down the nominal interest rate ,R_t, and the Taylor rule pins down the inflation , \Pi_t but how these equation reacts when we have a contradictionary monetary policy shock? I thought the shock starts to propagate into the model through the Taylor rule and it increases R_t and then the increase in the nominal interest rate would decrease the current consumption and so on.

It there any formal way (adding a term or removing a variableother than changing the parameters) to be followed in order to get rid of the overcompensation (of the initial increase due to the shock) you mentioned in your reply to get the nominal and real interest rate in the same direction?

I guess your model is more complicated than the standard three equation model. In Gali’s textbook it is shown that the ex ante real interest r_t-E_t{\pi_t} increases, while the nominal rate can go either way, depending on the feedback parameters and the show persistence. In a nutshell, the logic is that there is endogenous feedback in the Taylor rule and the interest rate is jointly determined. Thus, the specific IRFs may depend on the various model elements.

Thank you so much for your reply. I really appreciate your help.

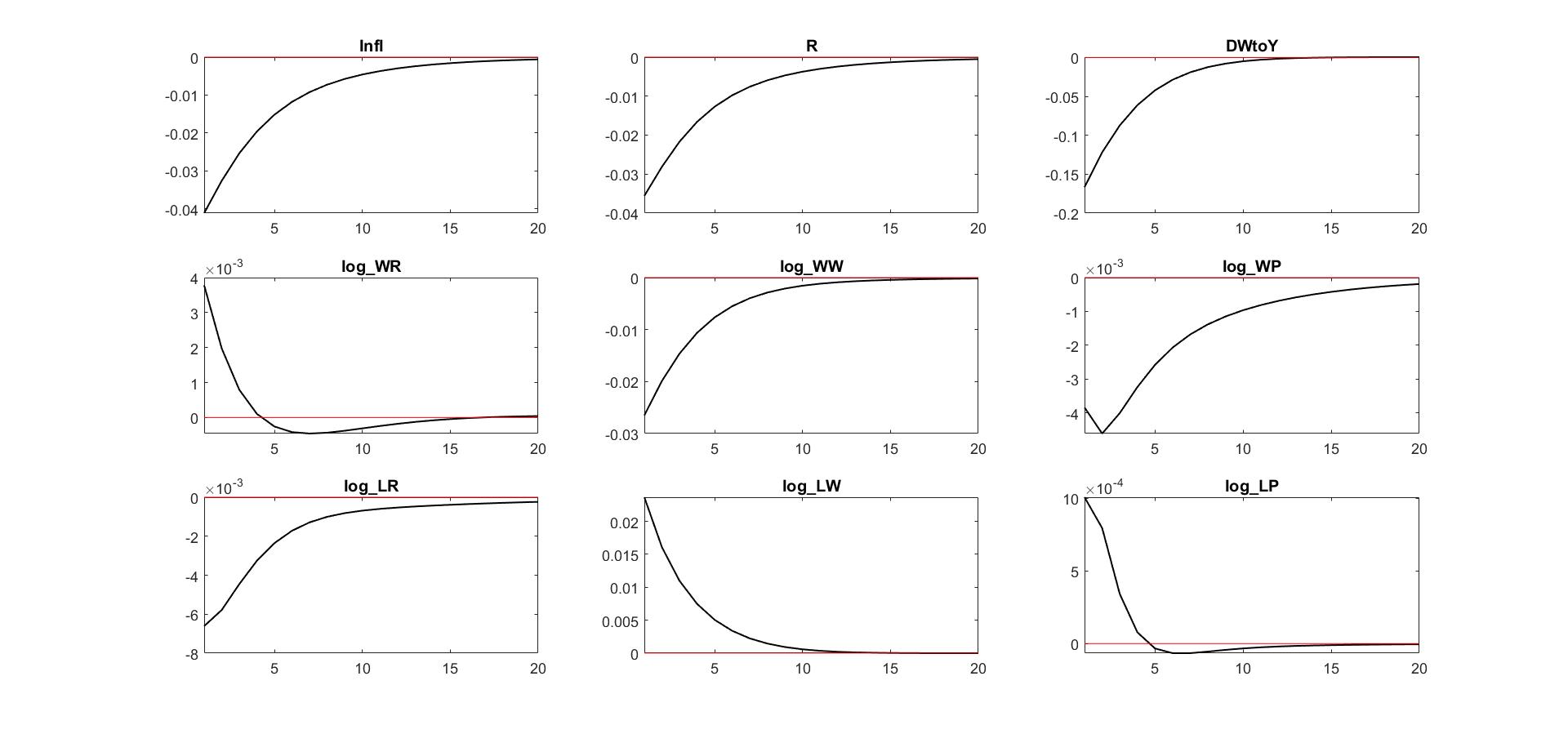

Whenever I run the code, no matter what values I consider in my Taylor rule for \phi_R and \phi_Y , Inflation (Infl) drops more compared with the nominal interest rate R. Is this normal? I attached both my code and the IRF results here. S is the AR(1) proces for the monetary shock and I have three agents in this economy. I am using Rotemberg setup for the price stickiness.

Thank you a lot for your reply Prof. Pfeifer.

I did not get what you mentioned. What do yo mean by saying “Actual inflation should be mostly unrestricted”. Should I change anything in the code or in the considered Talor rule? Is there any way that helps me to get higher inflation than the nominal interest rate?

Thanks a lot.

In the attached file, I have a positive monetary policy shock and EPS_R increases. As you mentioned before, it means that I have a contractionary monetary policy and the real interest rate (real_t=R_t/\pi_{t+1}) must rise but It really did not occur and log_Realinterestrate negatively responded.

I also have a simple taylor rule R_t/R_{ss}=(\pi_t/\pi_{ss})^{\phi_\pi}S_t and a normal Euler equation \beta_RE_t(\lambda_t(+1)R_t/\lambda_t\pi(+1))=1;

As I understand correctly, these two equationes pin down R_t and \pi_t. In many models, I can see that the inflatoin change less compared with the nominal interest rate. I was wondering if there is any problem with my Taylor rule as it always give me a higher change in the nominal interest rate. Could not it end up in having a negative real interest rate and that’s the reason of having a negative real interest rate?

As another agent in the economy can use Housing as a collateral to borrow b_t \leq LTV \times House_t\times \pi_{t+1}/R_t, the real rate plays an important role in my model.

I Hope my explaination helps.

It’s hard to tell because your model features a complicated transmission mechanism. I don’t have a good intuition what’s happening here. Did you try to go step by step to see which feature causes your findings.

Here, t is quarterly frequency, right? So Π^{annual}_t is like annualized quarterly inflation, right? I have quarterly inflation data for my country (like t is quarterly frequency) but the inflation rate is computed as (P_t/P_{t−4})-1. Thus, inflation rate between one quarter in year 1 to same quarter in year 2.

I think that makes the inflation rate annualized quarterly inflation and thus I can apply similar technique when interest rates are annualized to de-annualize the inflation rate too, right?