Dear professor @jpfeifer,

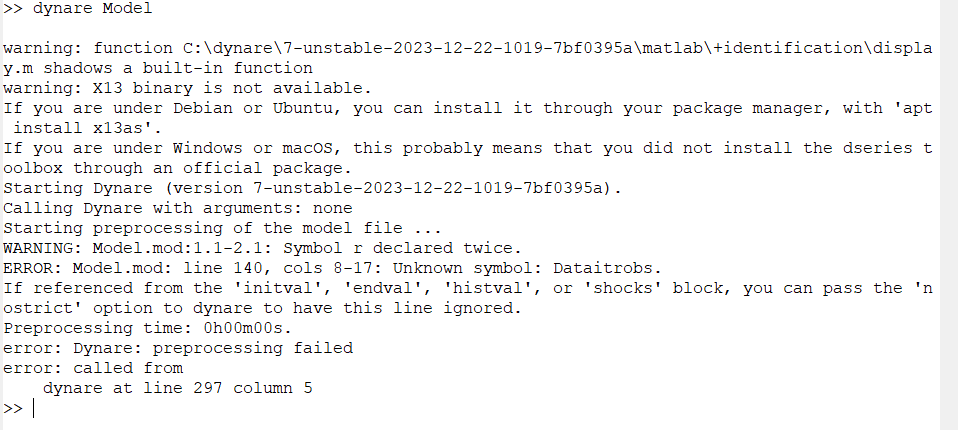

@stepan-a is not responding, so could you help me instead please? I obtain error message that symbol r is declared twice, although I introduce the variable in the model block and steady state model block once only. Thank you.

Modeln.mod (3.7 KB)

reestimate model.m (371 Bytes)

data1.mat (4.9 KB)

You have in your first line:

var dc dr dm dpi din r h x a e z v y k in c d m w r q n tau lambd ksi pi c_obs m_obs in_obs pi_obs r_obs Dataitrobs Dataitpiobs Dataitmobs Dataitinobs Dataitcobs;

Perfect, I corrected this.

However, now I obtain this error:

The steadystate file did not compute the steady state

Model1.mod (3.7 KB)

data1.mat (4.9 KB)

reestimate model.m (371 Bytes)

You forgot to set the steady state of the observables:

Model1.mod (3.7 KB)

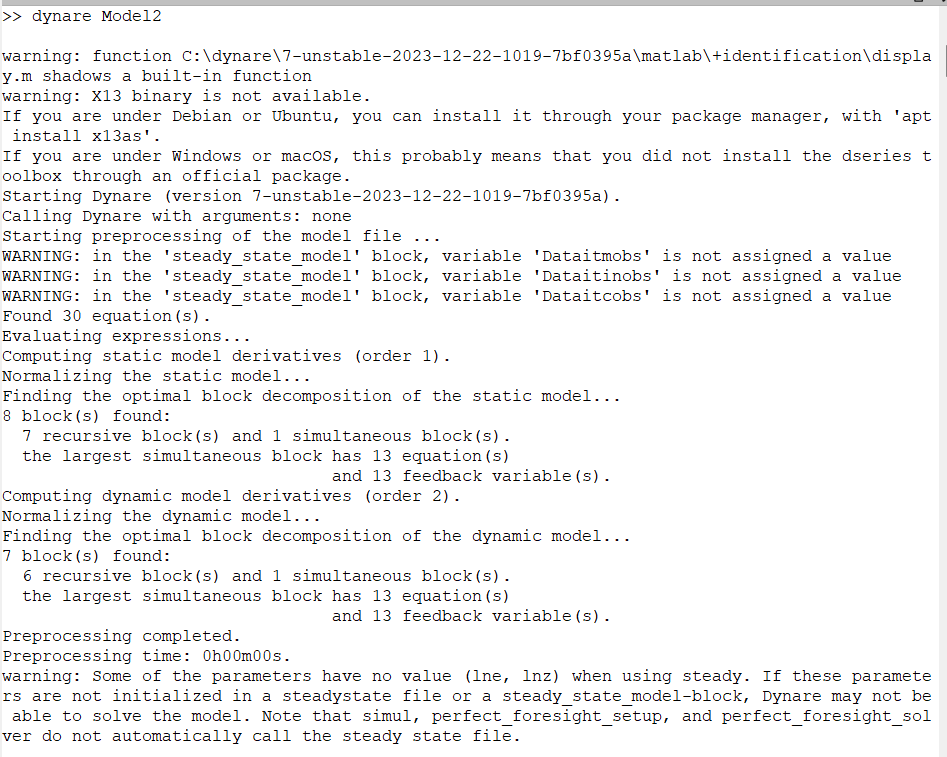

But now I obtain this error:

I can't find a datafile (with allowed extension m, mat, csv, xls or xlsx)

Model2.mod (3.7 KB)

data1.mat (4.9 KB)

reestimate model.m (371 Bytes)

Check the naming of your data file.

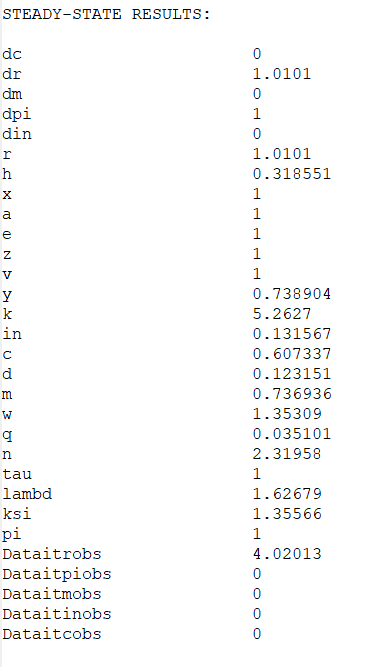

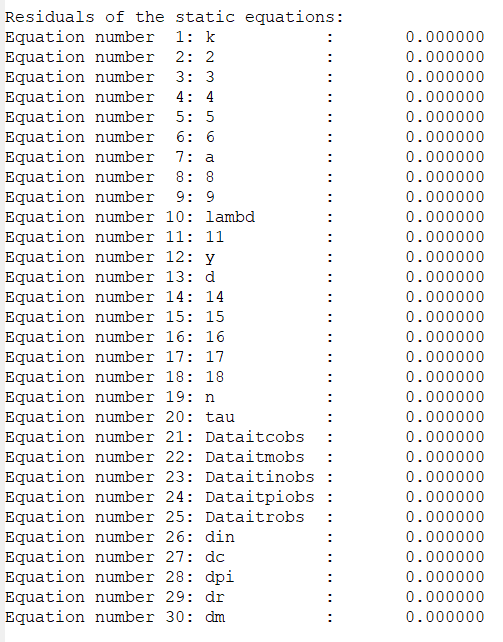

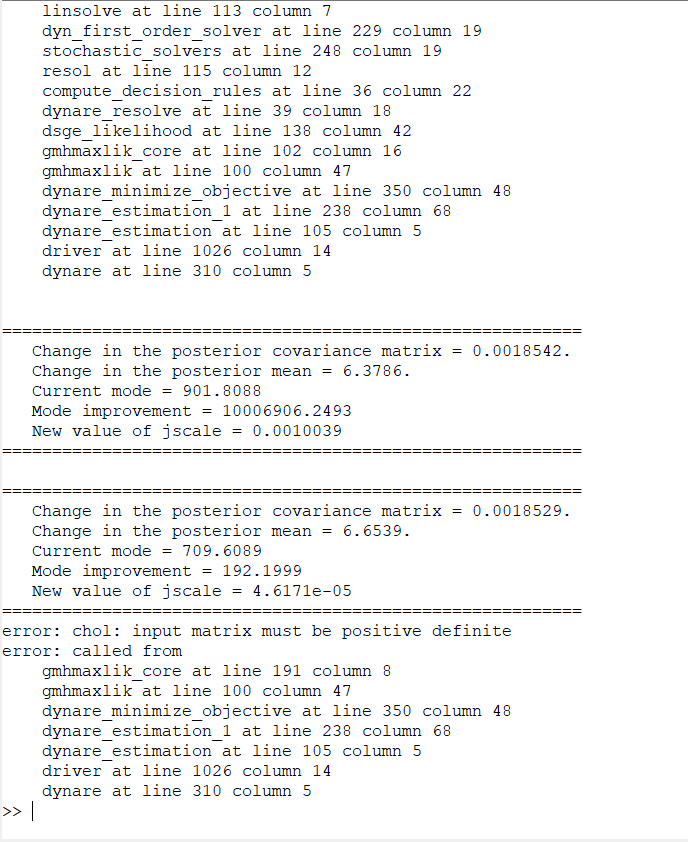

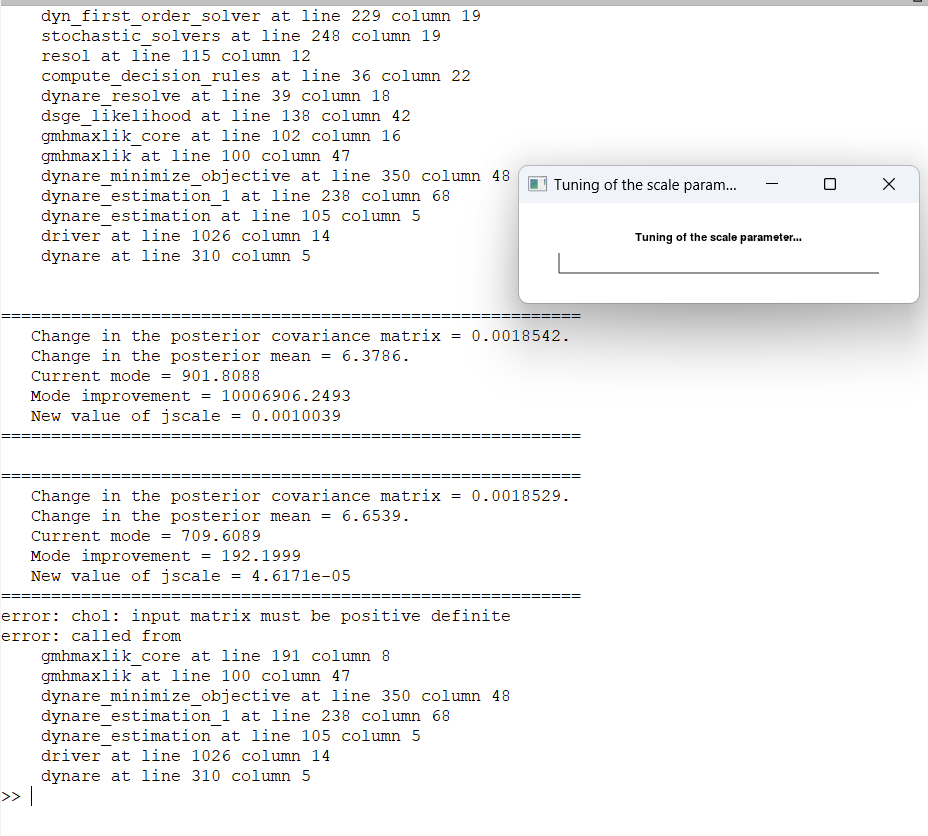

Perfect, I can partially run the file, however at some point i get this error message:

error: chol: input matrix must be positive definite

Can I just ignore it?

Always provide the full error message.

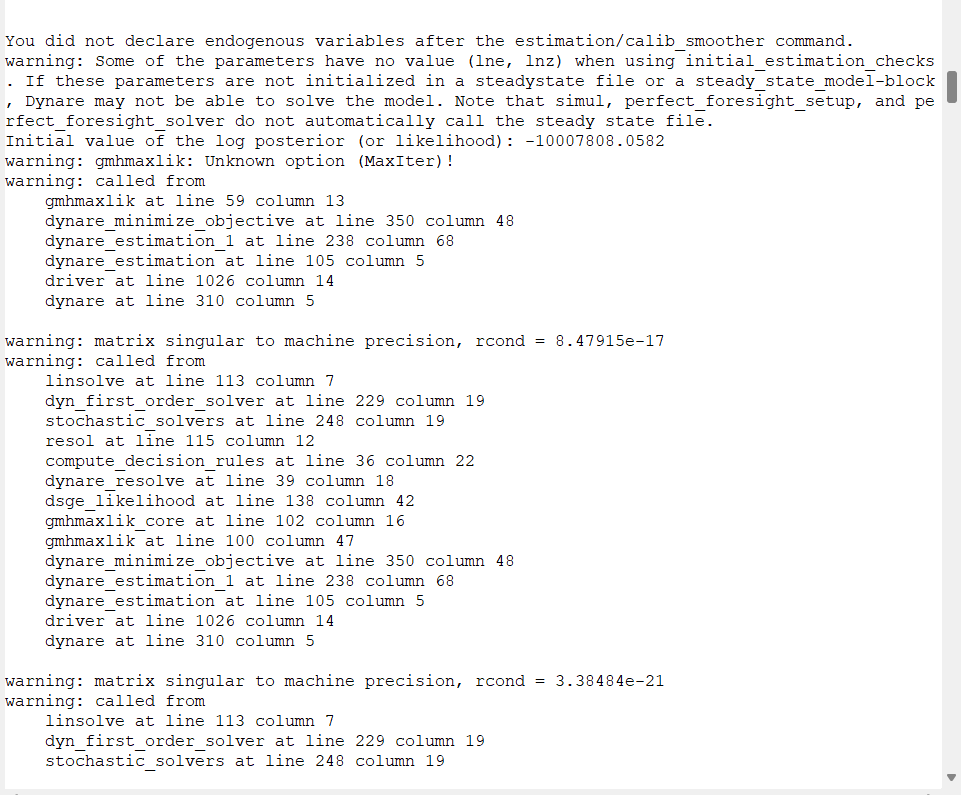

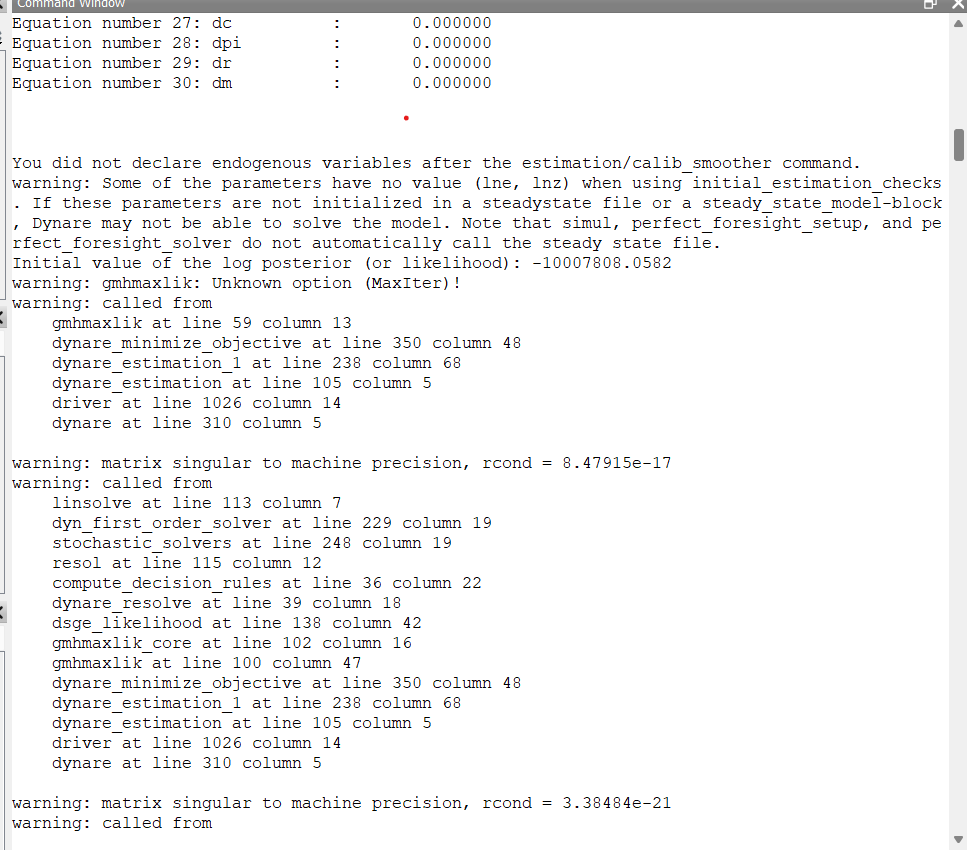

Please find the entire output in the attachment.

Dear professor,

I provided the entire error message, as you requested. Is there anything else I can provide? The reply is much appreciated in advance!

This suggests that something during estimation goes completely wrong. Already the value of the initial likelihood suggests that an error codes was triggered.

Dear professor Pfeifer,

- I think I should first make the original estimation file work, before proceeding to adding function

- For some reason I can run Bayesian estimation, but not ML. As soon as I replace intervals with mean values of estimated parameters, I obtain error message.

Any advice will be much appreciated!

Model4Bayes.mod (3.7 KB)

Model3 ML.mod (3.6 KB)

You did not provide the data file.

Thanks a million for the reply dr. Pfeifer. Here is the data file:

Data1.xlsx (19.3 KB)

Why can I run the Bayesian but not the ML estimation?

The ML files does have a different set of observables not contained in the data file.

I’m sorry for the mistake, the correct file is in the attachment.

Model5.mod (3.5 KB)

It seems you are running into the “dilemma of absurd parameter estimates” of ML estimation that led An/Schorfheide to advocate Bayesian estimation.

Okay, I will try to run my structural parameter stability tests using Bayesian and not ML estimation.

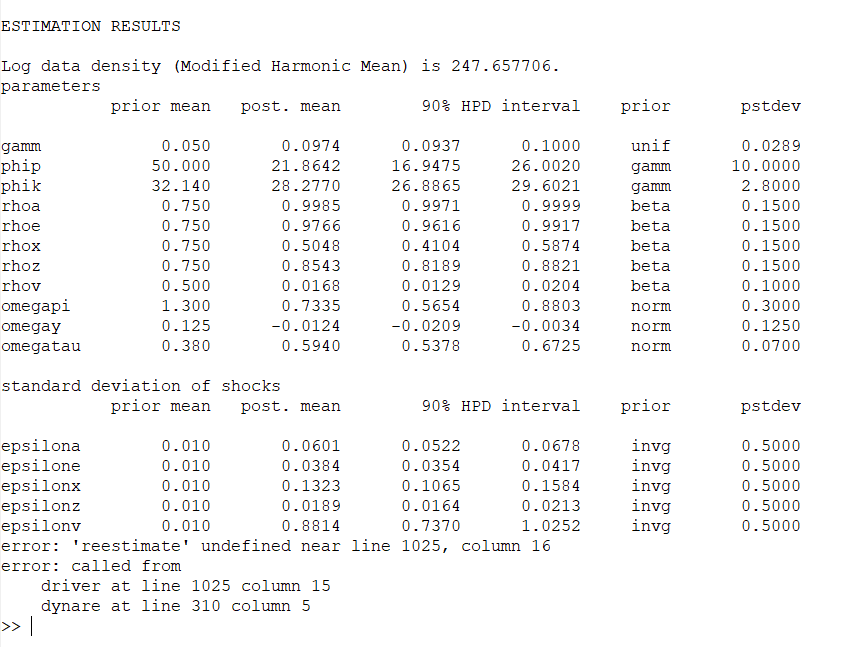

Second, the estimation looks good, but then I obtain an error “reestimate undefined”:

Model6.mod (4.0 KB)

data1.mat (4.9 KB)

reestimate model.m (371 Bytes)

Again, check the naming of your files. The file you want to run has a different name in your upload.

Thank you professor, I can run the file perfectly now. However, my master’s thesis advisor told me I can’t use this parametric bootstrapping method in case I use the Bayesian estimation.

Given that the paper by Röhe that I’m trying to replicate uses ML estimation, is there any chance for me to run ML estimation too, even with “dilemma of absurd parameter estimates”? Or is this dilemma consequence of my problematic observation data?

Here’s my output:

Model6.log (25.6 KB)