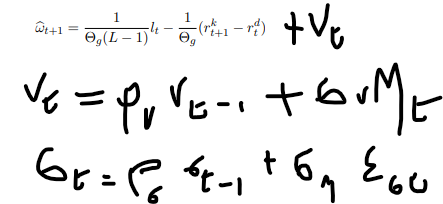

I wonder if a sound way to include a risk shock in a Bernanke, Gerlter and Gilchrist financial accelerator model could be having the log-linear default threshold as evolving autoregressive with stochastic volatility. Would it be isomorphic to a risk shock in levels?

E.g. the model would include this log-linear condition for omega: