I have several exogenous processes in my model.

In my steady state, I set the values of these processes to their long-run mean specified in the AR process.

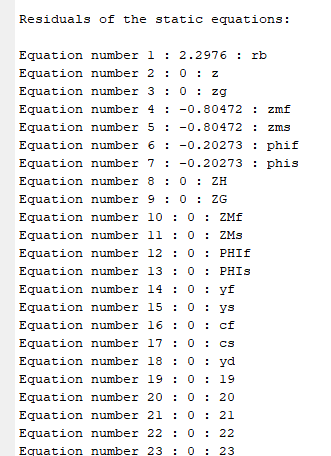

When the autocorrelation parameter is set to zero, everything runs fine and steady state residual is zero. But when I change the autocorrelation parameter to a positive number, I get the error that the steady state is not found.

See file attached.

dsge3.log (2.9 KB)

fveq.m (2.2 KB)

You only uploaded the log-file, not the mod-file.

Apologies. New to MATLAB. Here is the mod file.

dsge5.mod (5.6 KB)

nssol.m (1.3 KB)

With your specification for the AR process:

x_t=\bar x + \rho x_{t-1}+\varepsilon_t

you have in steady state:

x=\bar x + \rho x\Rightarrow x=\frac{\bar x}{1-\rho}, which will only be equal to \bar x for \bar x=0.

Specify your process as

x_t=(1-\rho)\bar x + \rho x_{t-1}+\varepsilon_t

and the steady state will indeed by \bar x.

Of course. That was a blunder from me. Thanks a lot.