Equation number 1 : -1.7259e-05 : Y_T

Equation number 2 : -4.6338e-05 : Y_N

Equation number 3 : 3.8e-05 : K_T

Equation number 4 : -3e-05 : K_N

Equation number 5 : 5.4213e-05 : IM

Equation number 6 : 0 : x

Equation number 7 : 0 : 7

Equation number 8 : 0.055757 : 8

Equation number 9 : 5.2081e-05 : 9

Equation number 10 : -5.7641e-06 : 10

Equation number 11 : 5.6118e-06 : 11

Equation number 12 : 0.00010487 : 12

Equation number 13 : 0 : C

Equation number 14 : 0 : P

Equation number 15 : 0 : L

Equation number 16 : 0 : pi

Equation number 17 : 0.001092 : W

Equation number 18 : 7.965e-05 : 18

Equation number 19 : 0 : 19

Equation number 20 : -9.77e-06 : P_T

Equation number 21 : -9.77e-06 : 21

Equation number 22 : 9.1902e-05 : C_F

Equation number 23 : -2.8233e-05 : 23

Equation number 24 : -2.8233e-05 : 24

Equation number 25 : 0 : 25

Equation number 26 : 0 : 26

Equation number 27 : 0 : 27

错误使用 print_info (第 32 行)

Impossible to find the steady state (the sum of square residuals of the static equations is 0.0031). Either the model doesn’t have a steady state,

there are an infinity of steady states, or the guess values are too far from the solution

I can find a steady state but there are singularity issues

STEADY-STATE RESULTS:

Y 0.814175

Y_T 0.647485

Y_N 0.351949

C 0.513208

C_T 0.246459

C_N 0.267616

C_F 0.0414797

P 6.82761

P_T 7.36303

P_N 6.31239

P_F 4.23785

P_FT 4.57019

K_T 11.9851

K_N 2.8113

L 0.299434

L_T 0.15499

L_N 0.14445

W 10.7659

I 0.465718

I_T 0.35955

I_N 0.0843359

IM 0.114022

TB -0.164745

pi 1

r 0.00755668

ex 1.95987

x 1

MODEL_DIAGNOSTICS: The Jacobian of the static model is singular

MODEL_DIAGNOSTICS: there is 3 colinear relationships between the variables and the equations

Relation 1

Colinear variables:

Y_T

Y_N

C

C_T

C_N

C_F

P

P_T

P_N

P_F

P_FT

K_T

K_N

L

L_T

L_N

W

I

I_T

I_N

IM

TB

ex

Relation 2

Colinear variables:

x

Relation 3

Colinear variables:

Y

Y_T

Y_N

C

C_T

C_N

C_F

P

P_T

P_N

P_F

P_FT

K_T

K_N

L

L_T

L_N

W

I

I_T

I_N

IM

TB

ex

Relation 1

Colinear equations

6 7 16 19

Relation 2

Colinear equations

6 16 19

Relation 3

Colinear equations

6 7

MODEL_DIAGNOSTICS: The singularity seems to be (partly) caused by the presence of a unit root

MODEL_DIAGNOSTICS: as the absolute value of one eigenvalue is in the range of ±1e-6 to 1.

MODEL_DIAGNOSTICS: If the model is actually supposed to feature unit root behavior, such a warning is expected,

MODEL_DIAGNOSTICS: but you should nevertheless check whether there is an additional singularity problem.

MODEL_DIAGNOSTICS: The presence of a singularity problem typically indicates that there is one

MODEL_DIAGNOSTICS: redundant equation entered in the model block, while another non-redundant equation

MODEL_DIAGNOSTICS: is missing. The problem often derives from Walras Law.

The timing of your capital also seems wrong to me. Maybe you should recheck the model equations carefully.

Sorry to bother you. I’m really new to dsge model and I have so many problems can’t handle. I’ve checked the model and didn’t find any problems. Do you have any advices to the singularity problem or the IRF plot? Thank u very much !!

One issue is that both your variables for capital should be predetermined variables, check the Dynare documentation. Also there is the problem with the singularity. This, as the output tells you, most often comes from the fact that you have included redundant equations but left out important ones. For anyone but you, it is almost impossible to say which ones these are as only you know your model well.

Typically, people start from a working model code and than extend it. I guess you did something similar. So what you should do, especially if you are new to DSGE modelling and Dynare, is to go back to a smaller and easier understandable model that actually works and from there extend one feature at a time.

To your first question, no you cannot simulate the model, ie draw IRF’s, if you not solve the issues explained above.

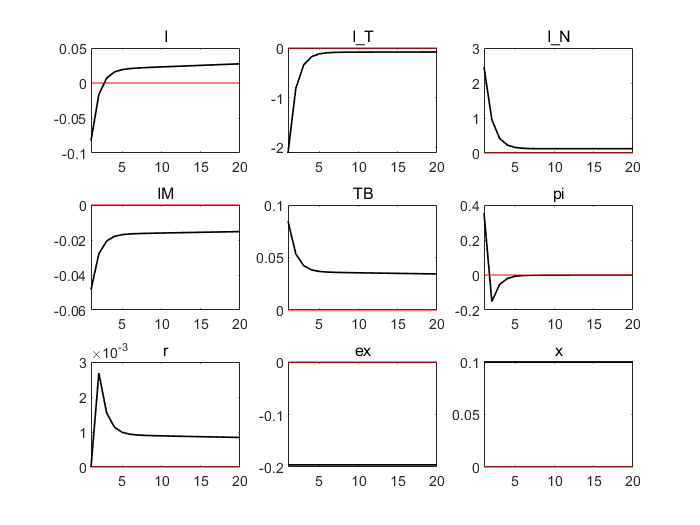

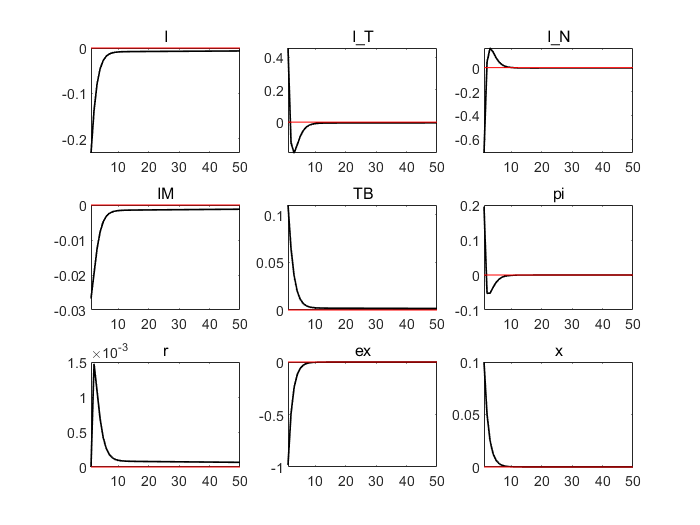

I just got the IRF results. But it seems to be wrong. I used stoch_simul()

Why the variable “x” and “ex” are constant? I set a positive shock to the disturbing term of “x”, and “ex” is supposed to be negatively correlated to “x”. The other variables are also strange. Because they can’t return to the steady state.

Were my results wrong?

PLEASE HELP ME!!! THANKS!!!