Hi,

I’m new at Dynare trying to replicate a code of a paper. I want to add Bayesian estimation but something went wrong.

dynare sw_2020.mod

Starting Dynare (version 5.1).

Calling Dynare with arguments: none

Starting preprocessing of the model file ...

Found 61 equation(s).

Evaluating expressions...done

Computing static model derivatives (order 1).

Computing dynamic model derivatives (order 1).

Processing outputs ...

done

Preprocessing completed.

STEADY-STATE RESULTS:

Y 2.89875

C 1.71006

I 0.608939

G 0.579751

L 1

Ld 1

Ih 0.608939

Yw 2.89875

K 24.3576

u 1

w 1.75682

wr 1.75682

mrs 1.59711

Pi 1

Pir 1

pk 1

pw 0.909091

f1 3096.91

f2 1939.07

x1 10.3851

x2 11.4237

vp 1

vw 1

Q 26.6813

QB 30.7424

RF 1.01248

RB 1.00753

Rd 1.00503

Rre 1.00503

Rtr 1.00503

M1 1.24827

M2 1.2011

mu 0.596469

Lam 0.995

fw 0.739456

f 0.738369

b 0.0386595

re 0.289875

d 16.9432

n 4.2358

lambda 0.0351955

phi 4.7452

Omega 3.01855

fcb 0.00108644

bcb 0.00848624

bG 0.0471458

A 1

theta 0.658515

logY 1.06428

logC 0.536531

logI -0.496037

logLd 0

logPi 0

logRd 2.00502

exr 2.95588

logQ 3.28396

C_obs 0

Y_obs 0

I_obs 0

Pi_obs 0

Rd_obs -1.45347

You did not declare endogenous variables after the estimation/calib_smoother command.

Posterior IRFs, smoothed variables will be computed for the 61

endogenous variables of your model, this can take a long

time ....

Choose one of the following options:

[1] Consider all the endogenous variables.

[2] Consider all the observed endogenous variables.

[3] Stop Dynare and change the mod file.

[4] Consider all the endogenous and auxiliary variables.

options [default is 1] = 1

Initial value of the log posterior (or likelihood): -77566642549.1891

==========================================================

Change in the posterior covariance matrix = 1.

Change in the posterior mean = 0.96.

Current mode = 33978768.7551

Mode improvement = 77532663780.434

New value of jscale = 5.8706e-08

==========================================================

==========================================================

Change in the posterior covariance matrix = 5.378e-11.

Change in the posterior mean = 0.90175.

Current mode = 37713413.4273

Mode improvement = 3734644.6723

New value of jscale = 4.2326e-08

==========================================================

错误使用 chol

矩阵必须为正定矩阵。

出错 gmhmaxlik_core (第 194 行)

dd = transpose(chol(CovJump));

出错 gmhmaxlik (第 100 行)

[PostMode, PostVariance, Scale, PostMean] = gmhmaxlik_core(fun, OldPostMode, bounds, gmhmaxlikOptions, Scale, flag, MeanPar, OldPostVariance, varargin{:});

出错 dynare_minimize_objective (第 336 行)

[opt_par_values, hessian_mat, Scale, fval] = gmhmaxlik(objective_function, start_par_value, ...

出错 dynare_estimation_1 (第 211 行)

[xparam1, fval, exitflag, hh, options_, Scale, new_rat_hess_info] = dynare_minimize_objective(objective_function,xparam1,options_.mode_compute,options_,[bounds.lb bounds.ub],bayestopt_.name,bayestopt_,hh,dataset_,dataset_info,options_,M_,estim_params_,bayestopt_,bounds,oo_);

出错 dynare_estimation (第 118 行)

dynare_estimation_1(var_list,dname);

出错 sw_2020.driver (第 894 行)

oo_recursive_=dynare_estimation(var_list_);

出错 dynare (第 281 行)

evalin('base',[fname '.driver']);

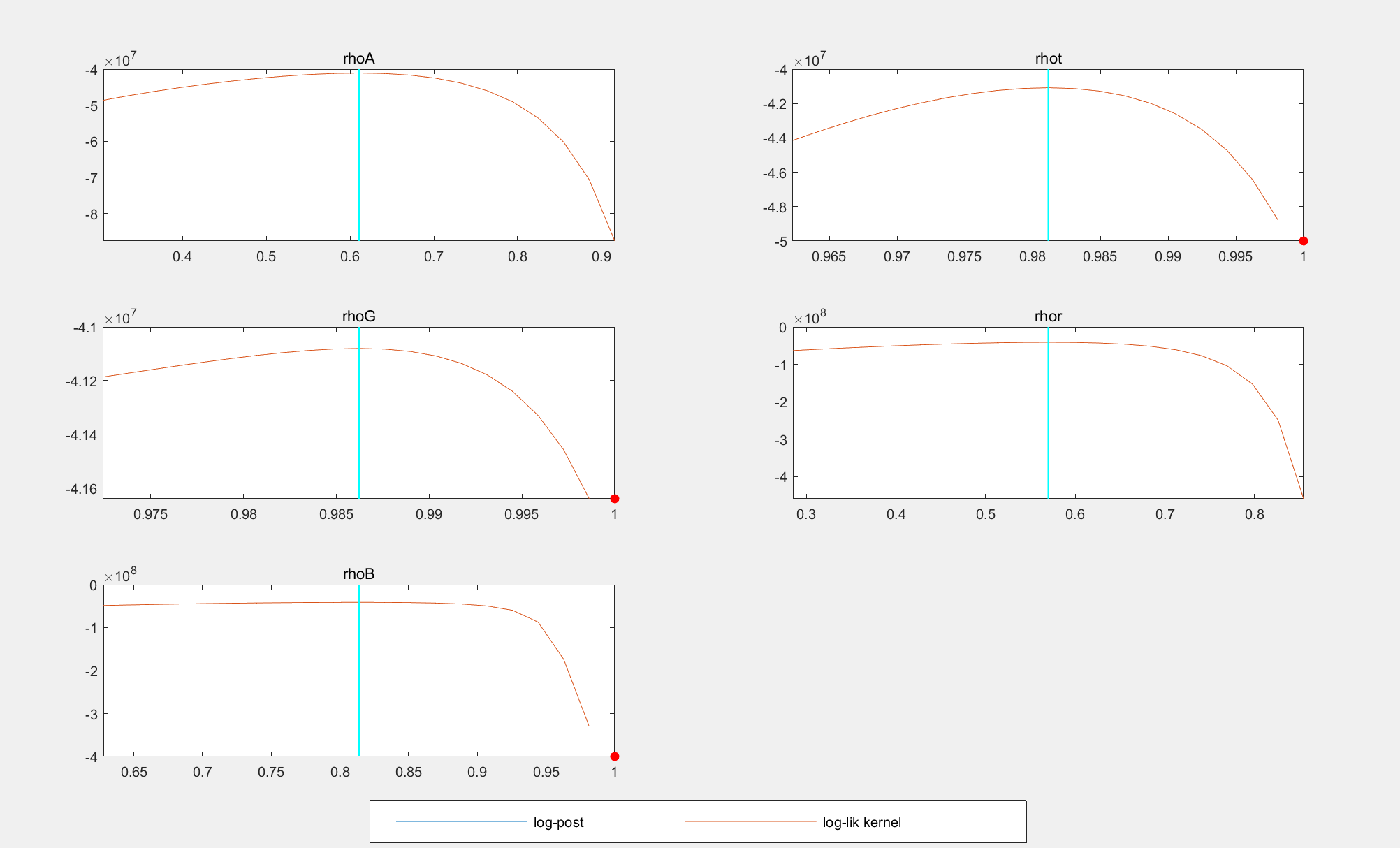

If the estimated_params only have

rhoA, 0.9 , 0 ,2, beta_pdf, 0.80 , 0.10;

rhot, 0.9, 0 ,2, beta_pdf, 0.80 , 0.10;

rhoG, 0.9 , 0 ,2, beta_pdf, 0.80 , 0.10;

rhor, 0.9 , 0 ,2, beta_pdf, 0.80 , 0.10;

rhoB, 0.9, 0 ,2, beta_pdf, 0.80 , 0.10;

the code can be run. Then the mode_check_plots looks like:

I don’t know how to tackle the problem, please help me.

sw_2020.mod (9.4 KB)

data_123.m (3.0 KB)

+sw_2020.rar (23.3 KB)