Hi everyone

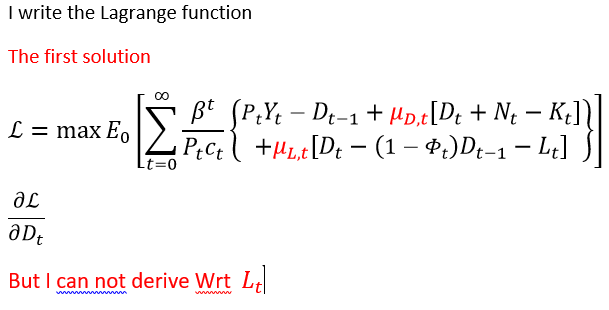

I have an optimization problem in my DSGE model and I doubt how to solve it. thank you for taking me out of this doubt. Because if I make a mistake, I will face bigger problems in Dynare.I know optimization, but having a dynamic constraint on my optimization problem makes it a bit complicated. Thank you in advance for your kindness

I will not write the expectation operator for simplicity.

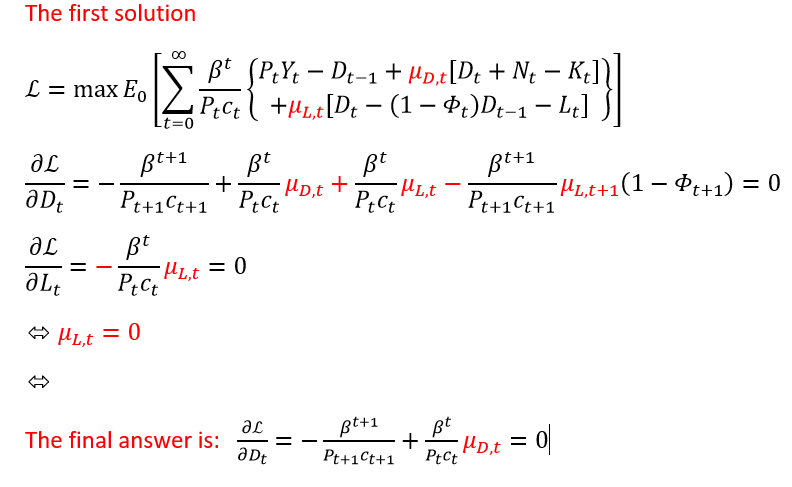

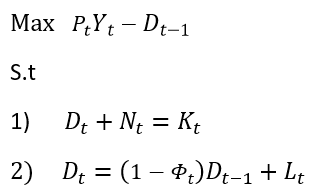

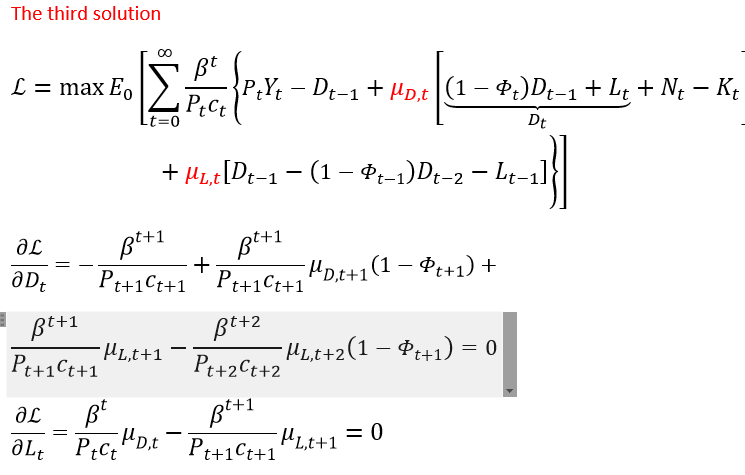

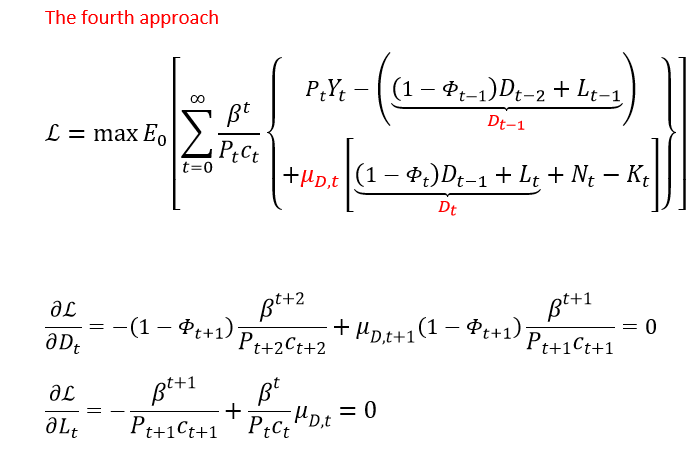

My optimization problem in the simplest case is as follows

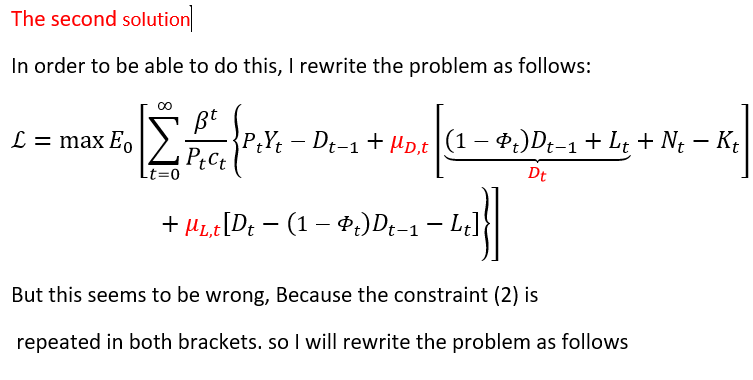

Which solution do you think is the best?. The third and fourth solutions seem to be more correct than the others. Please take me out of this doubt. Is there a better way to solve this problem?