Dear Professors,

I’ve just started learning dsge models, and I need your help.

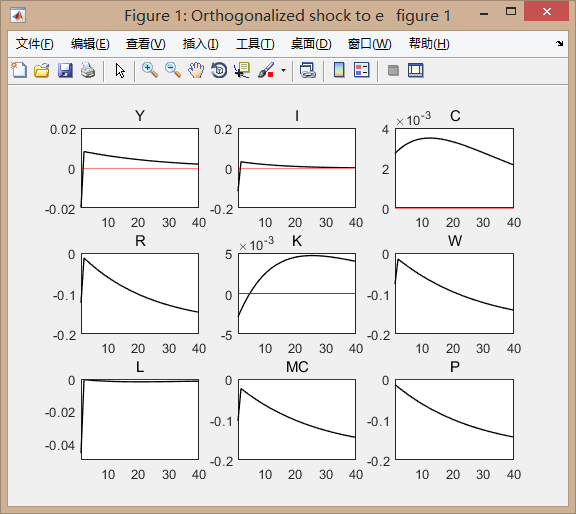

I’ve been reading the book Understanding Dsge Models: Theory and Applications and when I reach Chapter 3, I found few mistakes about the dynare code. So I fixed it by adding Taylor rules, but the impulse function graphs turned out to be really wierd. There are kinks in some graphs, but it’s impossible in a basic NK model. Every simulation should be smooth. Could someone help me pointing out the reason? Thank you so much!!!

image|560x500

chap3.mod (1.6 KB)

{kind=link}

Why is your model a mixture of linearized and nonlinear equations?

Thank you so much for answering my question. TheThe code is from the appendix of the book. The model is a log linear form and the few lines above the linear functions with# is the variable value at steady state.

Sorry, I missed that the whole model is linearized. I think your definition of marginal costs is problematic. It seems to be real marginal costs, but in the Phillips Curve you again detrend it by the price level.

Thanks again for your reply. The wage, rent and marginal cost are all in nominal form in the code so it might seems like there are both nominal mc and real mc. I also write a new one with real price levels but the results are quite the same. Actually I think I found the reason but I cannot explain it for now. Yesterday I found that when I switch the correlation between interest rate and the lagged interest rate in Taylor rules from 0.8 to 0.1 or even smaller, the irf results turns out to be normal and smooth. Do you know the answer for that?

Interest rate smoothing determines how strongly the central bank can react to contemporaneous developments.

Thank you!! I guess maybe it’s the autocorrelation of the interest rate that cause the irf image showing kink point.

Which box are you referring to? Usually, for Laffer curves you need to loop over parameters. There are various examples in the forum.

1 Like

very tanks