Dear all,

I am confused on the calculation method in the paper of “Capital controls and optimal Chinese monetary policy“, which is published on JME 2015.

Here I attach the DYNARE CODE and the paper downloaded from the author’s website.

And the key part of the code is below:

Here comes by question:

Since in they write their model in log_liearizing way, why they define welfare in a recursive way which Prof. Pleifer said should only be used in no-linear model? And what is the relationship between a recursively defined welfare function in the paper and the welfare calculation equation in the MOD file, which is “welf = -(1/(1-beta))C_ssPhi_l*(eta/2)*L_ss^(eta-1)*oo_.var(2,2);”. And the latter seemingly only cares about the variance of labor.

That is hard to tell. I haven’t read the paper, but they are explicit about the limitations of their approach in footnote 9. Using a recursive definition of utility is always fine, the problem is that the constraints are linearized, which is not generally correct.

With respect to welfare only depending on the variance of labor, it might be some algebraic transformation that gives rise to this expression. You might need to ask the authors.

Hello Prof. jpfeifer, I’m a neophyte to the Macro and to this forum. Code replications are really exciting!!

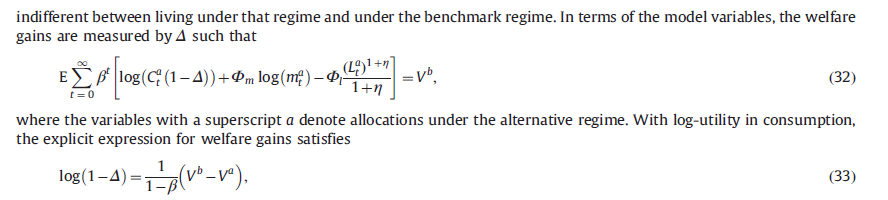

Following this topic and the same paper, on page 12 equation (33), is it wrong?

SInce equation (32) can be rewritten as: V^a+\mathbb{E}\sum\beta^t\log(1-\Delta)=V^b,

(33) seems to be: \frac{1}{1-\beta}\log(1-\Delta)=V^b-V^a?

Please tolerate my naive questions! Thank you in advance.

My next question is that I’m now proposing a similar paper like this JME paper, but my utility function is:

\frac{C^{1-\sigma}}{1-\sigma}-N

Namely, the consumption is CRRA and labor is linear form.

Before welfare analysis part, this setting enjoys very neat expressions in many FOCs and contraints calculations. Then I got stucked. Is there a concept called “labor equivalence”? such that: \mathbb{E}\sum \beta^t* [ \displaystyle\frac{{C^a}^{1-\sigma}}{1-\sigma} - N^a(1+\Delta)] = V^b

Here \Delta is the welfare loss that generated by shifting from benchmark model to alternative policies. We then still have an explicit expression of \Delta, if intentionally pursue the analytical way like this JME paper.

Very informative! Actually I have searched your similar answers, regarding Born & Pfeifer (2018), in some prior posts. I will resort to the numerical methods of Dynare at the first place!

If I have more leisure time, I will still try “labor equivalence”, as a purely counterpart treatment of the aforementioned JME paper.