Hi,

Can anyone help me with /give me some inputs on why I cannot compute the steady state value in my estimated real business cycle model?

Thank you in advance!

/Helena

rbc_romer.mod (955 Bytes)

Hi,

Can anyone help me with /give me some inputs on why I cannot compute the steady state value in my estimated real business cycle model?

Thank you in advance!

/Helena

rbc_romer.mod (955 Bytes)

Try

steady_state_model;

A = 1; %Normalization

r = 1/cbeta-1 + cdelta;

c = (1-calpha) * ((r/calpha)^(1/(calpha-1)))^(calpha);

lab=c/((r-cdelta)*(c/(1-calpha))^(1/calpha)+c);

k=(c/(1-calpha))^(1/calpha)*lab;

inv = cdelta*k;

y = k^calpha*(A*lab)^(1-calpha);

c = y-inv;

w=c;

end;

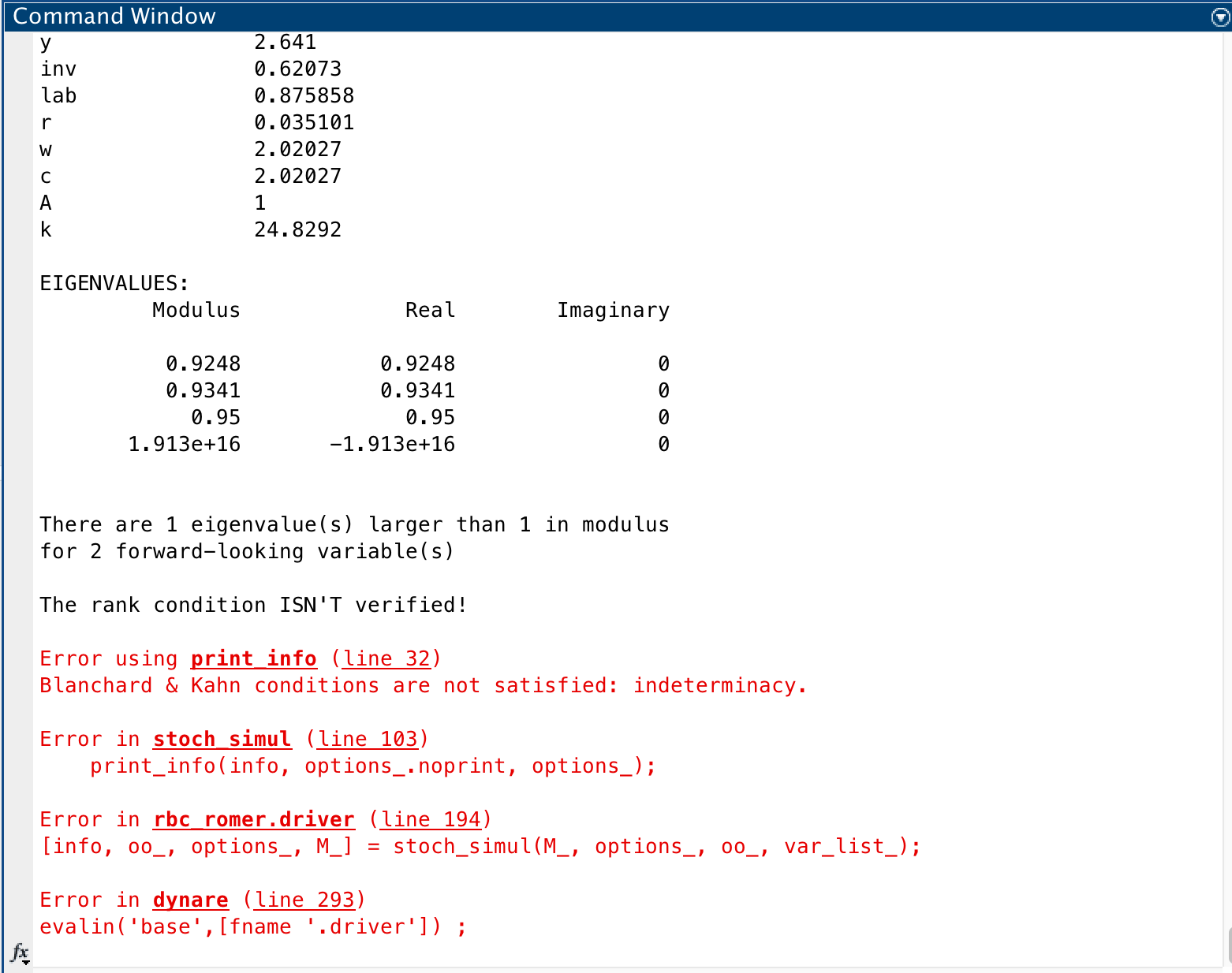

Note that your timing for capital is strange. That may be the reason for the Blanchard-Kahn conditions failing.

As I said above:

Check the timing.

By predetermine the variable capital (k), I can simulate the dynare code and obtain a result.

Thanks for your help