Dear all,

I built a DSGE model to compare the effects of several monetary policies.

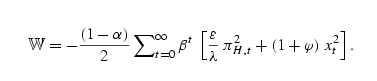

The welfare loss function is in the form of Woodford (2003) and Galí and Monacelli(2005).

I bulit a m.file in matlab:

“- (1- alpha)/2 beta ( epsilon/lambda * oo_.var(3,3) + (1+ phi)*oo_.var(2,2) )”

I have two questions as following.

(1)Numerical value of oo_.var are a little different according to different times of MH algorithm.

How much times should MH algorithm be? 10000 times?or 250 times?

(2)I’m not familiar with welfare analysis,so ask a basic question. In some articles,they also did different types of shocks on welfare losses,for example , technology shocks ,monetary policy shocks, etc(I’m not sure whether other shocks are not taken into account, only taking one kind shocks ?). I want to ask them how they did it. oo_.var has only one aggregate volatility?

Thank you in advance for answering my questions.