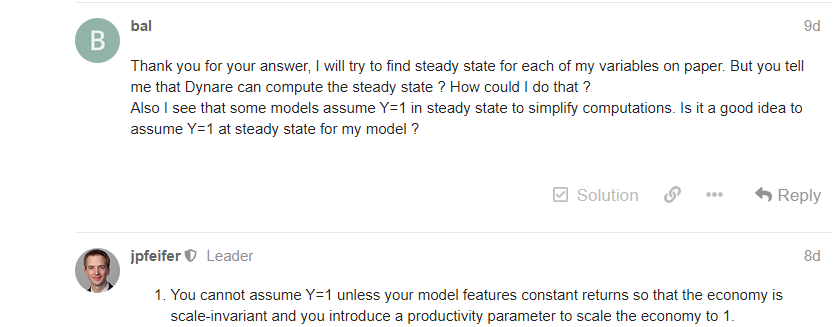

Hello, I am trying to do a DSGE model in Matlab, I have all the steady state equations on paper and pencil but I fail to find values for all variables. Here is my mod file: new.mod (6.6 KB)

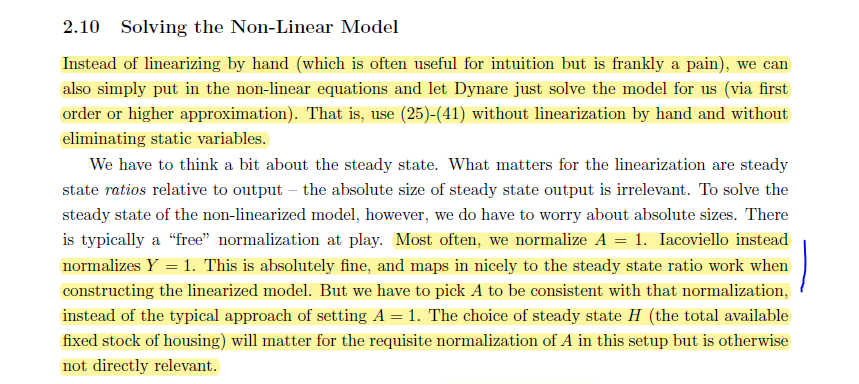

Indeed, since I have constant return to scale,  I have tried to assume Y=1 to simplify the calculations. But it leads me to a problem:

I have tried to assume Y=1 to simplify the calculations. But it leads me to a problem:

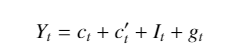

My market clearing equation is okay: all sums to 1 at steady state.

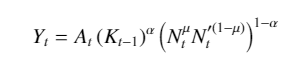

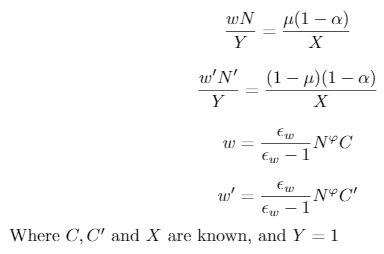

However the production function does not equal to 1. It’s because I have used other equations to determine N, N prime and wages. I used these equations to determine N, N ‘, w and w’:

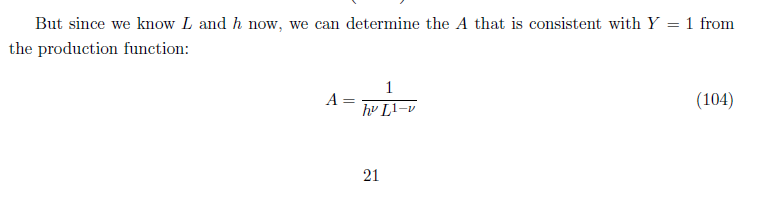

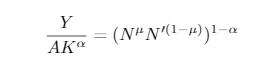

I have tried to use the production function, make Y=1, and since I know K I can express N in function of N '.

Where Y=A=1 and K is known

But then I fail at finding on paper and pencil a value for N, N prime and w and w’

Do you have an idea how can I assume Y=1 and still have the market clearing and the production function equal to 1 ? Do you recommand me another way to solve my steady states ?