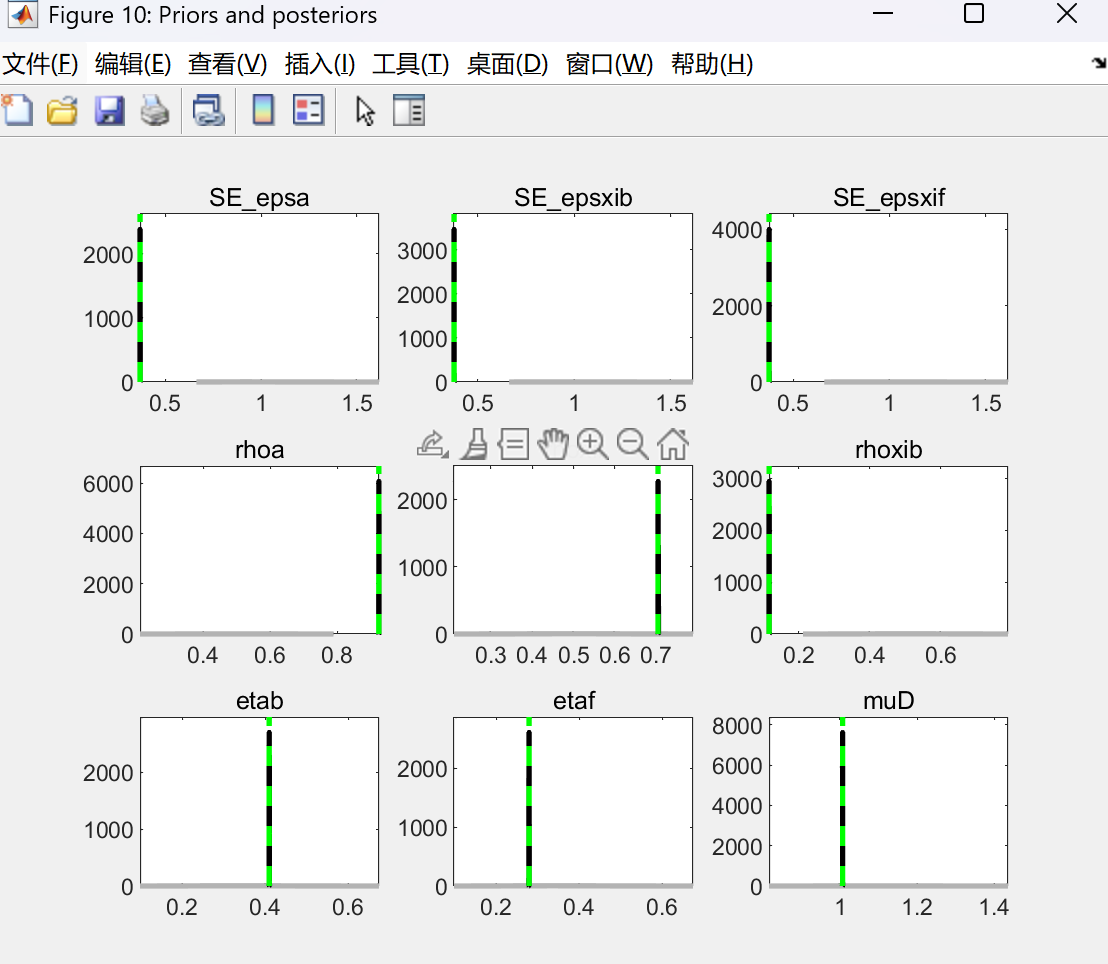

Dear professor, when I do bayesian estimation,the posteriors are straight lines, even if the acceptance ratio lies in 25%-33%.The data cotains GDP consumption and bankloan,I take log,seasonally adjusted and do HP filter.Please help me how to solve this problem,thanks in advance.

estimate_data.xlsx (7.6 KB)

Data_Bayesian.mod (7.4 KB)

That is because the identity matrix is very inefficient for sampling and with the few draws you are sampling do not properly sample the posterior space. You can see this when you inspect the trace plots.

Thanks professor, but when I do not use “mcmc_jumping_covariance=identity_matrix” command, dynare will report " chol Matrix must be positive definite." How to solve this problem?

That suggests a problem with mode-finding that you should solve in the first place