I have a question related to stationarity. Should the variables used for estimation pass statistical stationarity tests?

From your paper, ‘A Guide to Specifying Observation Equations for the Estimation of DSGE Models’, I understand the variables must be non-trending/stationary.

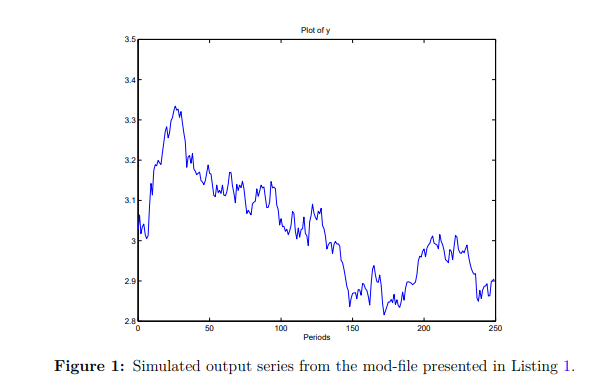

I have US data on inflation and interest rates from 1959 to 2009. They are non-trending but they fail KPSS and ADF tests for stationarity in levels. And figure 1 from the paper (simulated output) seems to have a trend over long periods. It looks like the decline in the inflation rate and interest (US data) since 1980s…and may fail stationarity tests.

Can we conclude that stationarity is assumed in the model? That is, even though it fails statistical stationarity tests, we assume that these variables (inflation and interest rate) are stationary. Is it also why inflation and interest rates are used in VAR-type models in their levels even when they fail statistical stationarity tests? Kinda confusing, right? Like on what basis can we say a variable is stationary…visual inspection? statistical tests? I am trying to understand these issues.