Dear professors,

I have a few questions about conducting optimal policy analysis. I am just a beginner at doing this excercise. I have tried so far two different methods: using fminsearch and csminwel ( I am aware of another option of csolve from Born & Pfeifer (2018). My model is a big scale model with 120 eqs.

-

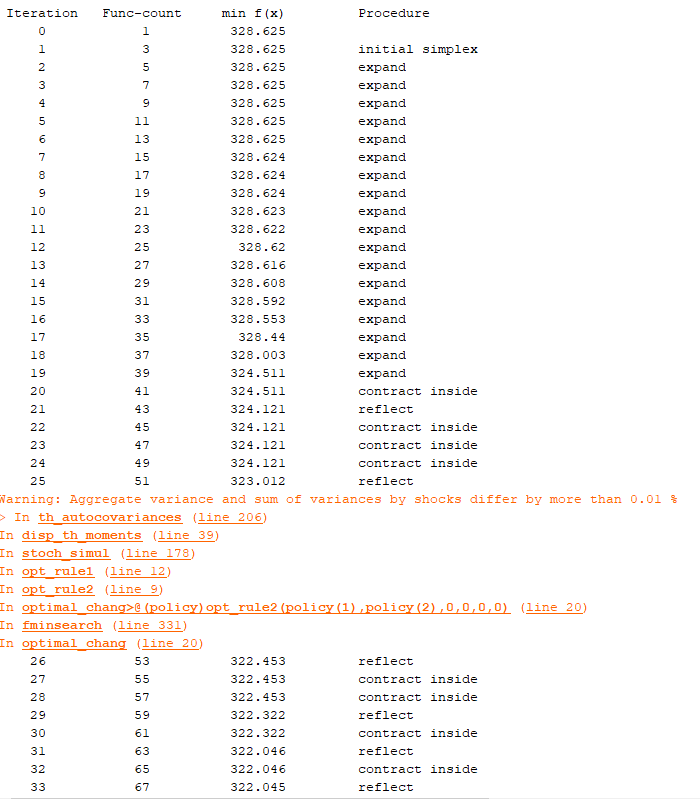

For fminsearch, my first run is to optimize only 2 params, the code work well using dynare 4.5 and matlab 2021a. However, from some point, the welfare value drops significantly and at the end reach a very small number (around zero) which suggest something wrong during optimization (I expect the changes in welfare value but not zero of -welfare). I attach the picture later. However, when I optimize with 4 parameters (2 in policy rule and 2 in tax rule), this does not happen and report reasonable results. Can anyone have any idea if something is wrong, or the algorithm problem or some models cannot be solved? Is there any way to set up the bound for params. I upload the code below but I cannot provide the mod file.

-

I tried with csminwel, following dynare forums, this is straightforward and the calculation time is much faster ( which may be a problem), I use dynare 4.6 for this run and the file in the attachment. My question is that the result seems to be extremely sensitive to initial point and the bound of params which raise the concern of accuracy, is there any way to improve this? Sometimes the algorithm failed to at some iterations also, is this because we go out of steady-state ?

-

I plan to optimize about 10 params, is it possible to do so (i know it may take really long time)? If it is possible, I am extremely grateful if someone can suggest more methods to do optimal analysis.

Thank you so much for everyone help.

optimal_rule_fminsearch.m (816 Bytes)

opimal_part.mod (541 Bytes)

welfare_objective.m (1.1 KB)