I have a model that incorporates a normalized production and consumption CES function à la Klump et al. (2007).

For my production function (capital-labor bundle), when I do the rescaling and try to find the parameter of the non-normalized form, such as Cantore et Levine (2011), I end up with a distribution parameter of capital of 1.05. So the two distribution parameters, alpha(K) and alpha(L), do not sum up to 1. I know that from de Jong and Kumar (1972) that both parameters do not necessarily sum up to 1.

Here is my question: can I assume that the two distribution parameters of my production function do not sum up to 1, but the two distribution parameters of my consumption function sum up to 1 (for feasibility issues) ? Or should I make the same hypothesis for all my CES functions ?

My understanding is that it has nothing to do with a hypothesis. There are two ways of writing down the normalized CES, once with two coefficients that need to sum up to 1, i.e. \alpha and 1-\alpha and once with two general coefficients, \alpha_l and \alpha_k. You can of course mix both versions as long as you fix the parameters consistently within each specification you use.

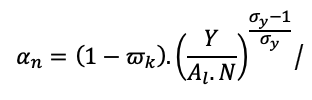

When rescaling the labor distribution parameter I have to following equation according to Cantore et Levine (2013):

with omega_k being the capital factor share, Al the labor-augmenting TP at point of normalization (=1), N total hours worked (employmentxhours) at normalization point, and Y value added at normalization point.

In my model I assume that time endowment is normalized to 1 so that alone the BGP hours worked are 1/3, and employment is normalized to 1 -> N= 1*1/3.

In order to rescale the labor distribution parameter alpha_n, can I take the value added per hours worked at point of normalisation as provided by national account ?

Or should I fix this alpha_n taking into account BGP values such that N=1*1/3, and Y is somewhat near 1 ?