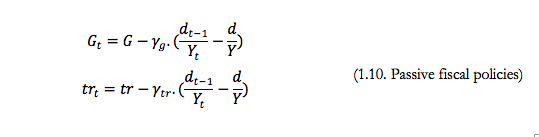

I would like to know how one fixes the reaction parameters of passive fiscal instrument to the deviation of debt. I have three instruments: taxes, which are exogenous (active policies), and public spendings and social transfers, which are the passive policies. My issue is with gamma(g) and gamma (tr). I cannot find any literature on these. Is there a simple way to define passive policies?

I would rather take a different approach that consists in separating the fiscal stance (i.e. the size of the public deficit) from the instruments of that policy (the tax rates and public spending).

You would have a single γ parameter appearing in the equation determining the fiscal deficit. For a eurozone country, there’s a natural value for this parameter, given by the debt criterion of the Stability and Growth Pact. It is equal to 1/20 (in annual frequency), assuming the steady state debt is 60% of GDP (in reality, the criterion states that it’s the 3-year moving average of debt-to-GDP that should be diminished by 1/20th of its distance to the 60% target).

Then you need to decide how to implement that policy. There are many options. One is to have all instruments constants, save one which will bear all the adjustment. Another option is to have the share of all taxes constant in the total tax revenue (and probably keep spending constant).

It is always hard to transplant fiscal rules from other papers, because specifications often differ. One reference that always shows up in this context is Leeper/Plante/Traum (2010)

Of course, if you want to introduce a permanent shock on τₗ, you have to declare that variable as an exogenous (I’m assuming you’re doing a perfect foresight simulation).

I’m getting back at you on this subject because I have a hard time finding the steady state. If public spendings do the adjustment, that means they are endogenous, as well as debt. But If I do not fix public spendings when I want to solve analytically my SS, I end up in a dead end.

Indeed, consumption is determined from the resource constraint that depends also on investment and public spendings. But public spendings are not known here. I can’t find them from the government’s budget constraint because that constraint depends on consumption as well and debt. Two unknowns.

What would you do in that context? Declare public spendings as an exogenous variables even though they bear the fiscal adjustment such as your paper https://www.ofce.sciences-po.fr/pdf-articles/actu/Viennot-al-NK-DSGE-SD.pdf ? I think the main problem is that I did not specify a function form for the reaction of public spendings.

Typically, in steady state:

— the level of debt is equal to the debt target level.

— the primary surplus is equal to the the interest payments on that steady-state debt level (assuming no steady-state growth). Said otherwise, the total budgetary surplus is zero.

— in turn, the fiscal policy instruments are determined by this steady-state primary surplus

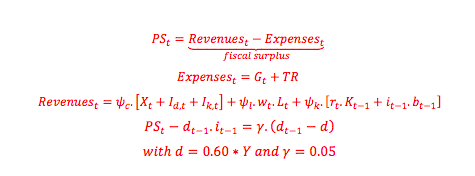

Going back to the equations in your message from Apr 2019, I think there is a missing equation: the law of motion of debt, that says that debt tomorrow is equal to debt yesterday plus interest payments minus primary surplus. This equation will determine the primary surplus in steady state.

Thank you @sebastien. I indeed incorporated the government’s budget constraint (the law of motion of debt). What if I have a BGP and not a steady state?

If I provide in the initval block a debt far from it’s steady state, should I write an endval? Or can I just let my code run given initial values and Dynare will compute itself the convergence ti steady state ?

Regarding the low-interest rate environment that is facing the EU zone, would you calibrate the discount rate with a low interest rate? Because, when I calibrate my economy based on long run values, I get an interest rate of 4.3%, which is far from what is observed in reality.

There is no obvious answer to your question. Everything depends on your assessment of the situation of the world economy.

On one hand, if you consider that the very low real interest rates that we have been witnessing for more than a decade are a transitory phenomenon, compatible with an infinitely-lived representative-agent model, then it makes sense to calibrate a long-term steady state with a nominal interest rate of about 4%. In this case, the challenge is to identify the shocks that have pushed rates so low for so long, and to ensure that your economy does not return too fast to the steady state (since long-term rates observed today are also very low).

On the other hand, you can embrace the secular stagnation hypothesis, and assume that we are now in one of the “bad” equilibria identified in this literature (see e.g. Eggertson, Mehrotra and Robbins, AEJ-Macro 2019). This literature typically uses overlapping generations models, often coupled with a decreasing population growth rate, to reconcile “normal” individual discount rates with (quasi-)zero nominal interest rates in the long run.