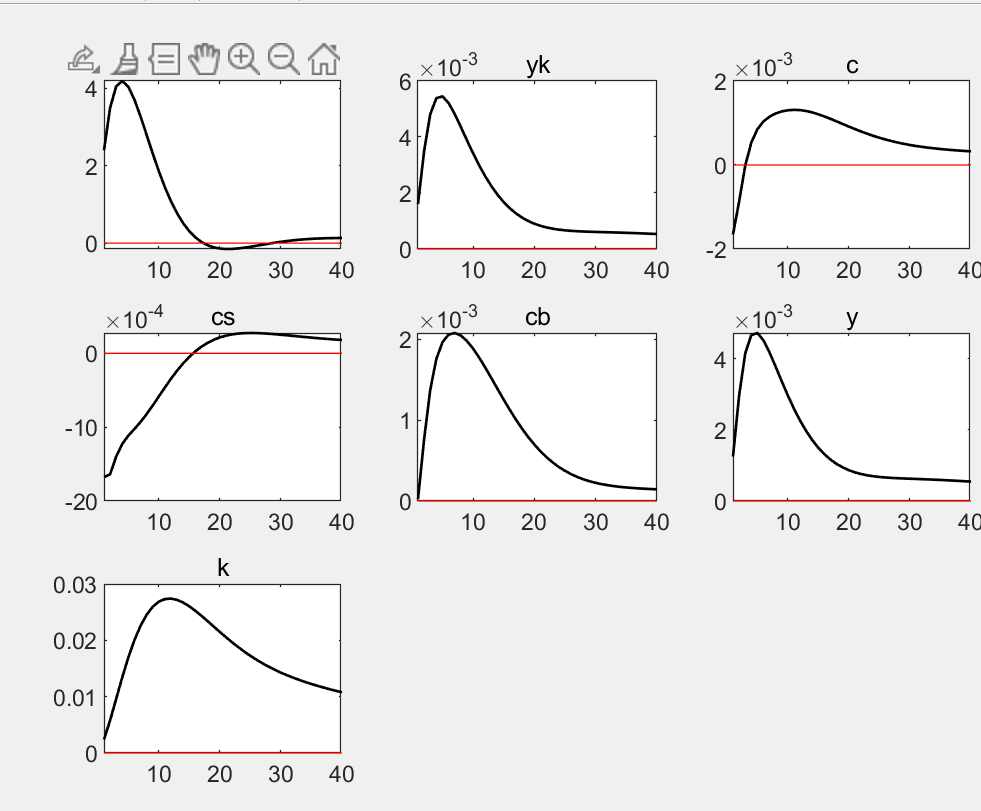

I begin a model with two types of households and two sectors. After solving the steady state, I run the model, I find it can figure out the impulse response. However, the Monetary policy shocks appear to be contrary to normal, with positive shocks causing output to increase.

So I use the model_diagnostics(M_,options_,oo_), and it indicate:

“MODEL_DIAGNOSTICS: The Jacobian of the static model is singular

MODEL_DIAGNOSTICS: there is 1 colinear relationships between the variables and the equations

Colinear variables:

ch

ds

bb

bk

nbk

yk

hs

hb

k

r

eta_h

lamda_b

lamda_h

lamda_k

Pi

Colinear equations

列 1 至 20

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

列 21 至 32

21 22 23 24 25 26 27 30 31 33 34 36

MODEL_DIAGNOSTICS: The presence of a singularity problem typically indicates that there is one

MODEL_DIAGNOSTICS: redundant equation entered in the model block, while another non-redundant equation

MODEL_DIAGNOSTICS: is missing. The problem often derives from Walras Law.”

Actually, I check my equations, and I make sure I omit one budget constraint condition for the Walras Law, so the number of vars is equal to equations, and not a redundant equation.

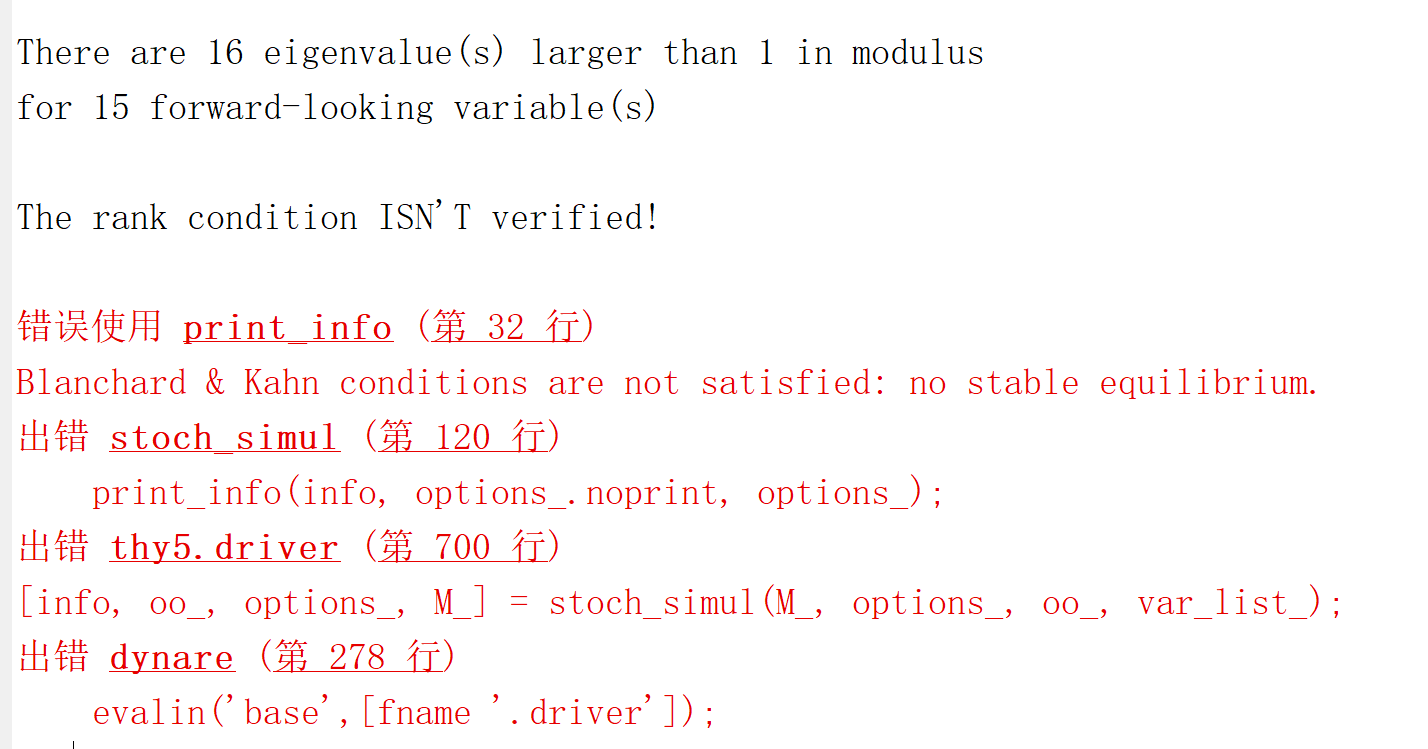

What also makes me confused is when I increase the parameter of interest rate matching

targeting coefficient of the inflation target in the Taylor Rule, then it can not run with the error:

Dr.jpfeifer, thank you for the suggestion! I have run a simple model that doesn’t consider the consumption inertia. And the model runs well. In order to have a hump-shape impulse response, I consider the consumption inertia, just introducing some Lagrange operators. Then the model meets these errors, what can I do next ?

Then you need to find out why that creates an issue. Sometimes it’s just a numerical thing with steady state Lagrange multipliers having to large a value in steady state so that numerical overflow happens. In that case, you can often ignore the singularity warning.

Thank you very much, Dr.jpfeifer! I still have other two problems:

I find I can not set the parameter of interest rate matching

targeting coefficient of the inflation target in the Taylor Rul (rho_PI) over a number (approximately 1).

I find the positive shock of em causes output (y) consumption (c) to increase, which contradicts the normal impulse response.

Dr.jpfeifer, what may cause these problems and what can I do for it?