I estimated my DSGE model for the period 1995-2017 with the aim to perform historical decomposition of GDP growth.

For simplicity I assumed that domestic interest rate is determined according to the modified UIP condition:

R = R_star + risk premium.

for the whole period. I neglected the fact that there were two different monetary policy regimes in this period: before euro adoption and after euro adoption. What are the consequences of neglecting this when estimating the model?

That is very hard to tell. You did not say which country you are considering and what the regimes are. If the foreign interest rate is exogenous and you are considering a small open economy without any structural break, then it does not matter what gave rise to the observed interest rate path.

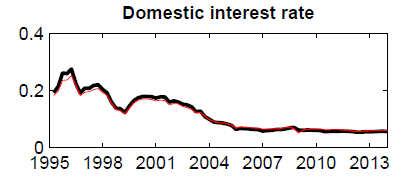

The model I used is that of Adolfson et al. (2007). This is a medium-scale small open-economy model. The model was estimated using quarterly data for Slovenia.

Regarding the monetary policy regime, Slovenia adopted the euro in 2007. During the period 1992-1995 the Bank of Slovenia had the control of base money as its operating target and the growth rate of money aggregate M1 as its medium term target. The target rates on M1 remained, however, unannounced. The Bank of Slovenia announced its money target for the first time in 1997, by setting the target rate on M3. From 2001 the main objective of the Bank of Slovenia became the reduction of inflation to the levels compatible with Maastricht requirement by the entry to the ERM 2 system of exchange rates. The official target rate on inflation has never been officially published.

As I wrote above, in the estimation, I assumed that:

R = R_star + risk premium for the whole estimation period 1995-2017.

From what I can see, you are not modeling any endogenous component of the interest rate process. So any breaks in the conduct of monetary policy should not matter, because you are not modeling them in any case.

thank you very much for your help. But what do you think:

should I model the break in the conduct of monetary policy? And what are the possible consequences (e.g. for the general parameter estimates) of not modelling modeling this break in a proper way? Are my estimation results wrong?

Or is my simplified approach that I followed (i.e. UIP condition without any special modelling of monetary policy process) still ok? My focus is not on monetary policy but on historical decomposition of GDP dynamics.