Hello to all,

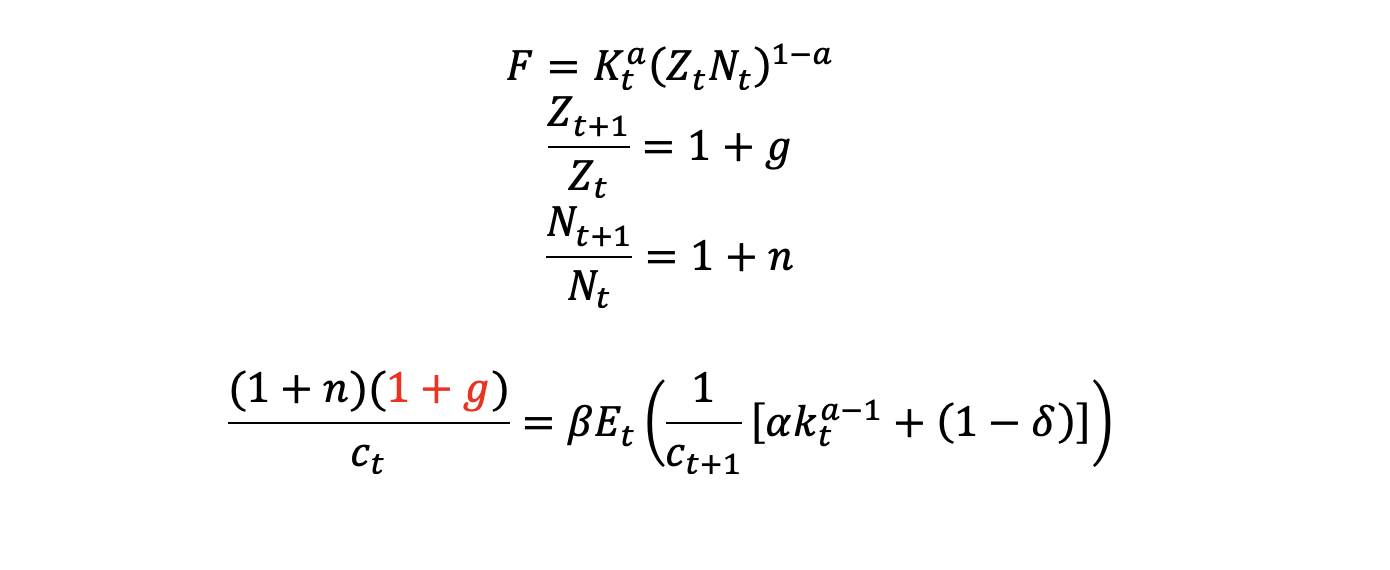

I wanted to ask how to match observed and Dynare-specified variable. While reading the excellent Guide to Specifying Observation Equations for the Estimation of DSGE Models, I was wondering how can we abstract from growth in per capita variables if specifying the Euler equation and the law of motion for capital in an stationary form implies that other parameters enter the equations. That is, making the dynare specification stationary requires acknowledging labor augmenting productivity growth. I upload a example with log-utility inspired on

Thank you very much,