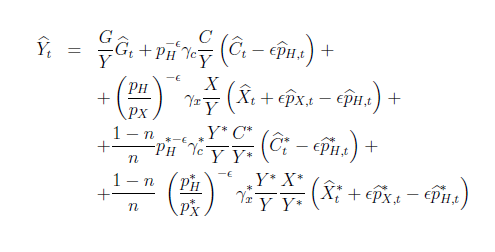

I am currently working on a DSGE model of two economies and I am having a trouble in specifying following market clearing log linearized equation in Dynare.

Could you please suggest me a solution how to specify the steady state fractions of prices? Which data should be appropriate for this? I am adding that X are investments.

The model is taken from http://epub.wu.ac.at/558/1/document.pdf

I am adding that in log linearized system, the variables P_hat do not occur, only inflations - for producers and importers. Therefore I am confused how to link the prices to the model as well.

The price objects in this equation are not price levels but relative prices (define by division by the CPI as far as I can see). You have to keep those in the model. They are of course linked to the respective inflation rates, i.e. not all equations you need are given in the paper. Rather, there are identities missing that link the price “levels” to inflation rates.

Thank you very much for your message.

I see, so, the ratios of relative prices should be calibrated from data?

And also, I am able to link the price levels to inflations, but I am not sure how to link the price levels of investment P_X to the inflation rate? I have not defined any separate inflation for this.

I am sorry for very simple explanations, but I am a very beginner in this area.

Thank you very much again.

Now I see that the equation is not linear, as price levels are multiplying another variables. Therefore, did you mean that all relative prices, including the ratios should be normalized to 1?

Your equation is linear in the variables with hats. The rest is parameters and steady state values, which are constant. I am not familiar with the particular model, but it is quite common to normalize all the ratios of prices to 1. As an alternative, sometimes in these models the shares of e.g. foreign and domestic inputs into the CES function are set in steady state. The price ratios can then be computed to satisfy these targets.

The ratios of prices will be normalized to 1. Then, what will be the value of steady state prices that occur in the equation?

Second question, after linking the prices to the inflation rates:

pi_H = P_H - P_H(-1);

pi_F = P_F - P_F(-1);

pi_Hstar = P_H_star - P_H_star(-1);

pi_Fstar = P_F_star - P_F_star(-1);

pi_X = P_X - P_X(-1);

pi_Xstar = P_X_star - P_X_star(-1);

There are no prices in your model, only ratios of prices as everything was relative to the domestic CPI. For example, p_H=\frac{P_H}{P}. That ratio is then normalized to 1.

Yes, there may be unit roots in your model as a consequence, but here that is a feature, not a problem.

Now I see it all, thank you very much for explaning and very useful help.

I am estimating the model with unit root feature, however I am getting an error for indeterminancy. Am I specifying the unit root incorrectly? unitrootmodel.zip (23.4 KB)

No, Error in computing likelihood for initial parameter values

Error using print_info (line 45)

Blanchard Kahn conditions are not satisfied: indeterminacy

Thank you very much for this link. I think there is a problem with timing due to the error of indeterminancy.

After adding predetemined variables, the model works. However, do you have any suggestion for me which variable may be predetemined in this case? I was thinking it may be employment.

Thank you very much, finally I found I used wrong sign in one equation and that was the problem, timing is ok. Thank you again for very helpful advices, I very appreciate this.