Hello everybody,

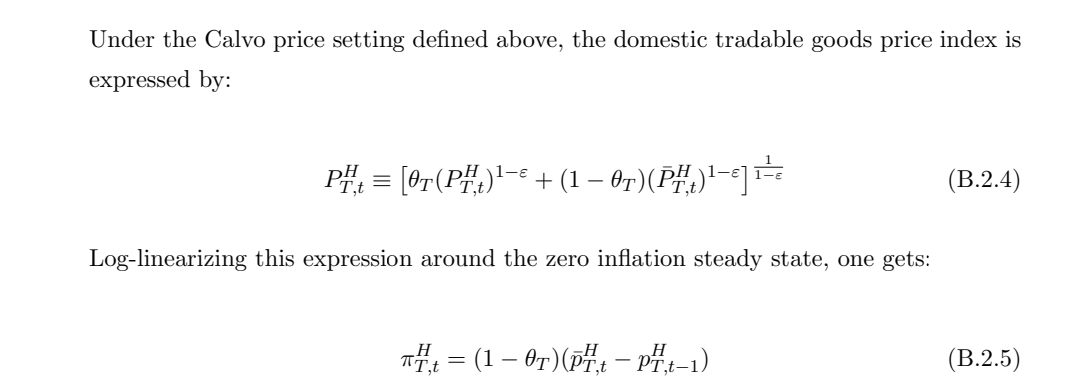

Can anyone please provide a step by step derivation of the log-linearized form of the following equation. I’ve tried to get from the first equation to the second but to no avail.

Thanks in advance.

Are you sure B.2.4 is correct. Usually it’s

P_{^{T,t}}^H = {\left[ {\theta {{\left( {P_{T,\textcolor{red}{t - 1}}^H} \right)}^{1 - \varepsilon }} + \left( {1 - \theta } \right)\left( {{\bar P}_{T,t}^H} \right)} \right]^{\frac{1}{{1 - \varepsilon }}}}

1 Like

Ah yes, that’s true! It’s an error in the document I was reading.