i want to reproduce the result of below article (cox and harvie, 2010):

(Resource price turbulence and macroeconomic adjustment for a resource exporter:A conceptual framework for policy analysis)

i write the final equation (20 equation) in dynare and i want to do simulation analysis, but harvie said in his article that:

"In this case, there are eight differential variables in the model: kp, kg, m, b, w, f, q and e; twelve algebraic variables: r, Nod, Nos, T, wp, y, yp, R, one, c, l and B; and ten exogenous parameters that are used to derive a solution for the long run steady state: mbar, rstar, kgstar, oa, pres, op, Nosp, c̄g, pstar and ystar

he said: **Of the eight differential variables, the first six are predetermined non-jump variables that adjust only gradually. The last two differential variables, q and e, are assumed to be non-predetermined or jump variables. **

For dynamic stability, the system must generate six negative and two positive eigenvalues.

i guess it means that six variables(kp, kg, m, b, w, f) is predetermined an others(q, e) is jump variable.

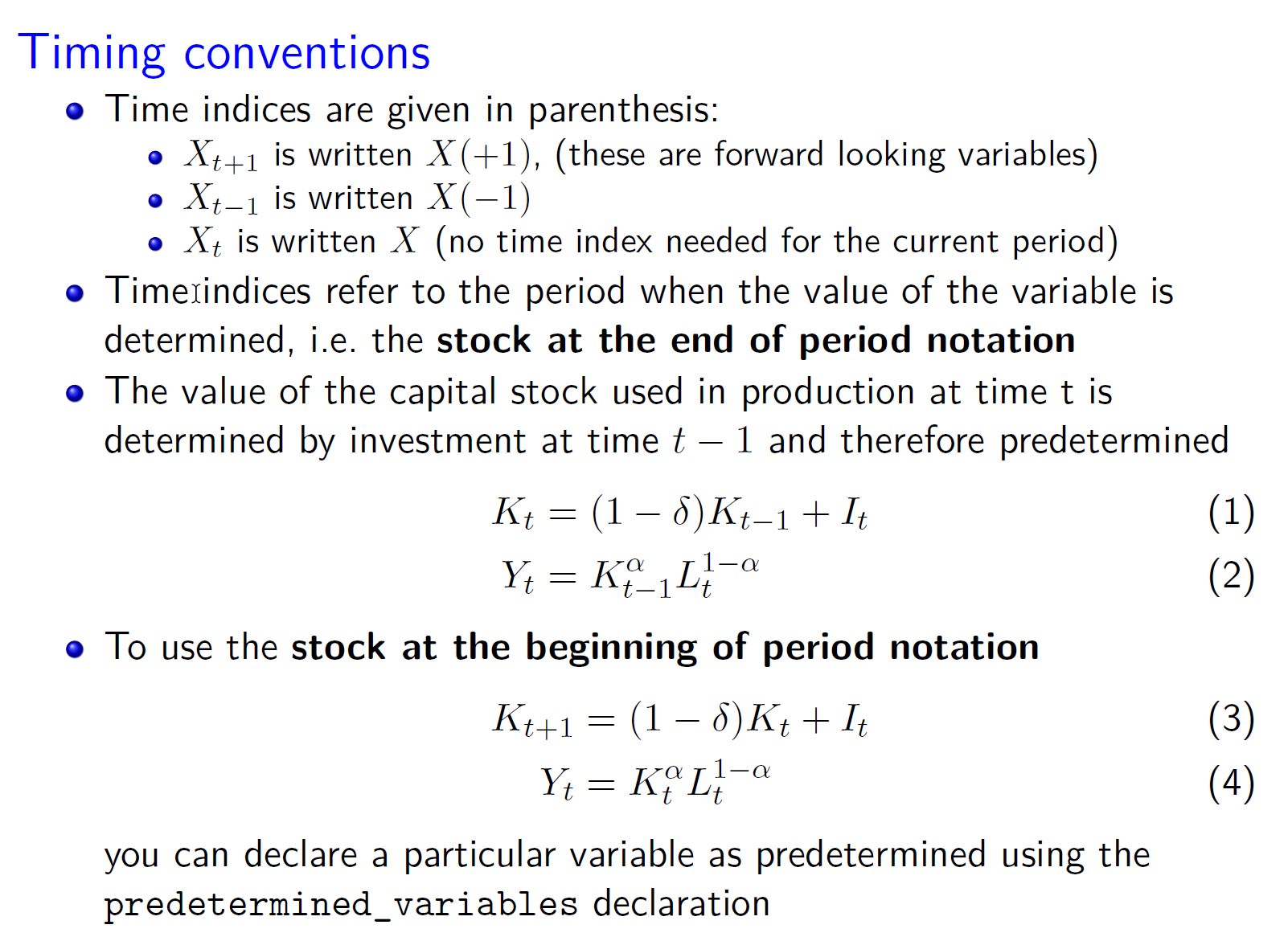

my question is how can i tell Dynare which of my variables are predetermined (backward looking) and non predetermined (forward looking)?

i write predetermined variable in this format, for example:

kp(+1)-kp = eta*q;

an i write jump variable in this format, for example:

q-q(-1) = (1/delta3)*q +(delta2/delta3)*r -(delta1/delta3)R -(delta2/delta3)(m(+1)-m);

as you see in second equation we have one jump variable(q) and one predetermined variable(m)

my dynare is correct or not?

I’m looking for your kindly response.