Hello everyone,

I am trying to replicate the IRFs of the closed economy (US) block of the following paper: Understanding the natural rate of interest for a small open economy - ScienceDirect

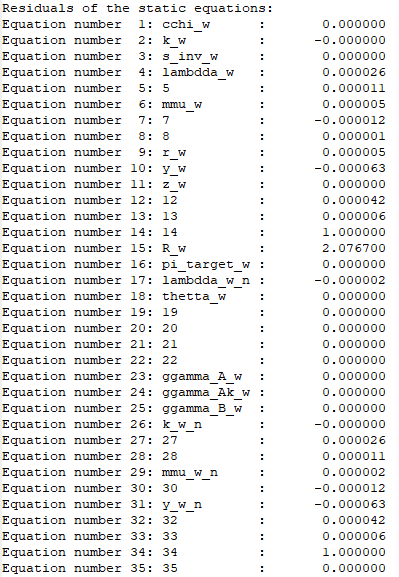

And I’m running into some issues with equation (14) and (15), specifically in the residuals of the static equations:

Keep in mind equation (34) is supposed to be a flexible-price version of equation (14), so the problem is roughly the same. I’m feeding steady state values through the initval section, values that I’ve computed in the attached file below. As I’ve been struggling with these problems for days on end now, I figured it would be worth it asking if anyone has had similar problems before.

solve_steady_state.m (329 Bytes)

us_block_steady_state.m (4.0 KB)

model.mod (9.1 KB)