Dear community!

Ive been working on replicating the model of Erceg & Levin (2003) for a while now with no success.

The core of the programming problem is given by their inflation targeting scheme, composed of 4 equations:

- \pi_t^T = \pi_t^p + eps_q

- \pi_t^p = \rho_p \pi_{t-1}^p + eps_p

- E_t \pi_t^p = \rho_p E_{t-1} \pi_{t-1}^p + K( \pi_{t-1}^T - E_{t-1} \pi_{t-1}^p)

- E_t \pi_{t+1}^T = rho_p E_t \pi_t^p

Where \pi_t^T is the inflation target, \pi_t^p is the permanent comp. of the target, and E_t \pi_t^p is the optimal Kalman filtered value for the perm. component (treated as a variable on its own).

Note that private agents only see the value of the target at t using the taylor rule. Future values of the target are expected to be formed using equation 4. The mentioned equation, 4, is the key to transmit shocks from \pi_t^p to the rest of the models equations.

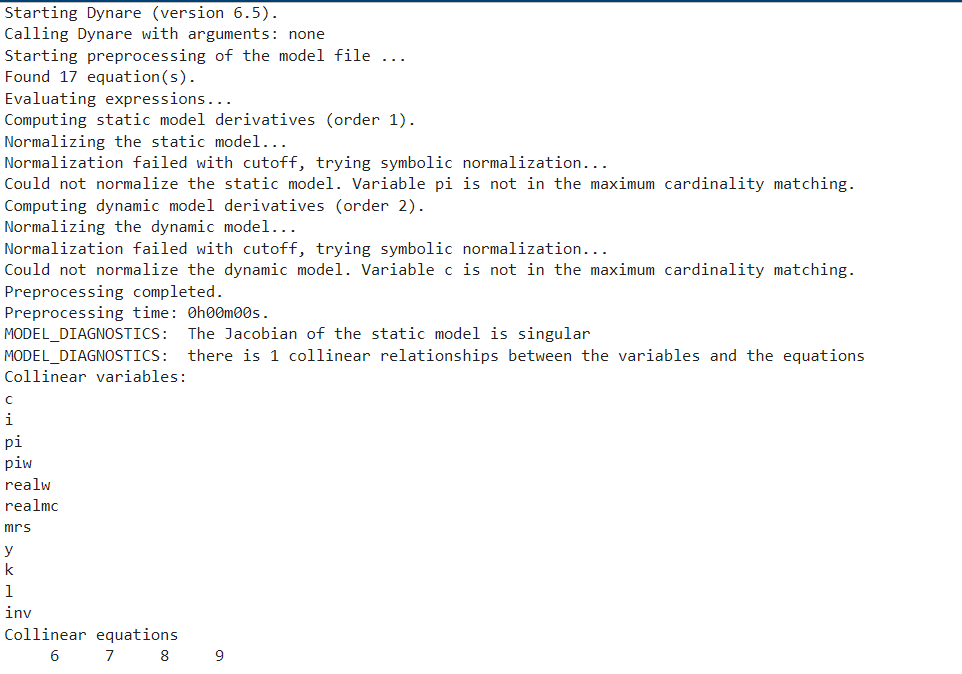

As said, the problem is this block of equations. After programming the model, I obtain a singular jacobian and get the message that these equations are collinear. In addition to that, I get some errors regarding cardinality matching of two variables (c and pi). Obviously, the programm is unable to perform the Schur decomposition.

The problem is derived from equation (4), but without it, the Kalman filtering equation does not have an impact on the rest of the variables. As said in the paper, this equation is part of the [estimated] model. Additionally, the authors use the Anderson Moore Algorithm (I already tried to program it with the Fred codes, with no success haha), but as I have read, given that the model is a rational expectations one, it shouldnt be a problem to program it on dynare.

Any help would be amazing. I’m attaching the dynare code I’m using and the reported problems.

Thanks,

Emiliano

el2003.mod (2.9 KB)

Notes:

(1) For equation (3) I’m using the approximation used in Céspedes & Soto (2005).

(2) For the equations for the Price Phillips and Wage Phillips I’m using the codes for Erceg, Henderson, Levin (2000) available in the forum. This set uses a unit root to define the real wages (realw = realw(-1) + piw - pi)

(3) For the so called “Euler Equation for Investment” I’m replacing the author’s (K_{t+1}-K_t)/K_t with (I_t/K_t)-\delta. This equivalence is derived from the Capital Law of Motion.

Citations:

Luis F. Céspedes and Claudio Soto. Credibility and inflation targeting in an emerging market: Lessons from the chilean experience. International Finance, 8(3):545–575, 2005.

Christopher J. Erceg and Andrew T. Levin. Imperfect credibility and inflation persistence. Journal of Monetary Economics, 50(4):915–944, 2003.