Hello everyone,

I am trying to replicate the Semi-Structural Multivariate Filter (FMV) used by the Chilean Ministry of Finance to estimate the non-mining output gap, as described in official budget and technical documents. However, I am encountering persistent issues during estimation.

Software versions

-

MATLAB: R2025a

-

Dynare: 6.5

I have also tested Dynare 6.1 and 6.4, but the problem remains unchanged across versions.

I am attaching:

-

The

.modfile -

The data file

-

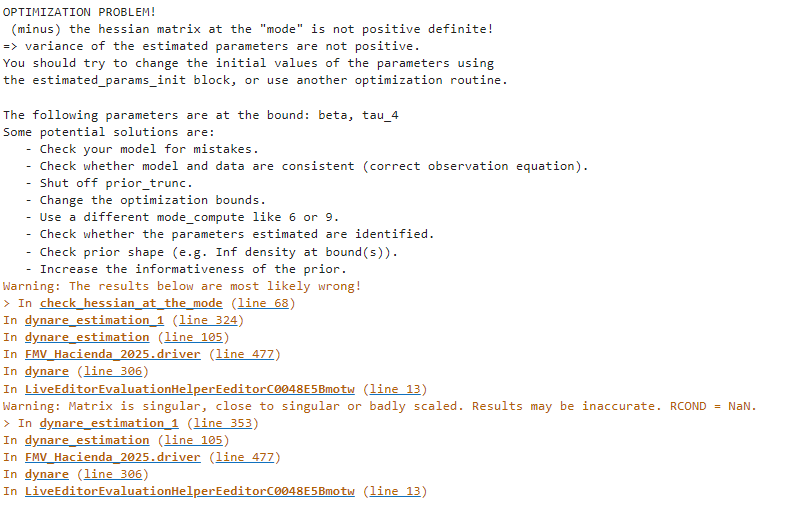

A screenshot of the error message

Any guidance or suggestions would be greatly appreciated.

FMV_Hacienda_2025.mod (2.5 KB)

FMV.xlsx (14.4 KB)

run.m (437 Bytes)