The problem is known as “stochastic singularity”, which happens if a linearized model implies an exact linear combination between observables. That in turn means that the density of observing that variables is either 1 (the exact linear combination in the model holds in the data; rarely the case) or 0 (the exact linear combination does not hold; the typical case). As you can imagine with a log density of minus infinity, estimation will not work.

You have in your model

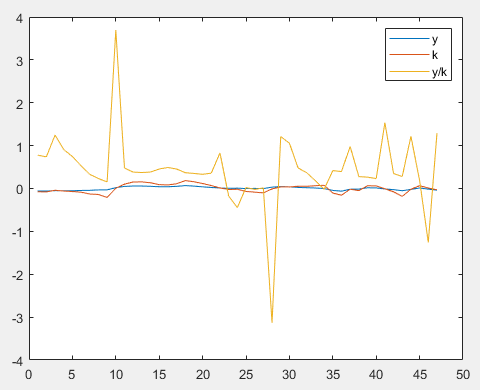

exp(y_tilde) = exp(k_tilde)^(alph);

But you observe k and y. That’s where the problem comes from. The model says that the ratio of y and k is a constant \alpha. Plotting the ratio shows that this is not the case in the data: