Hello everyone.

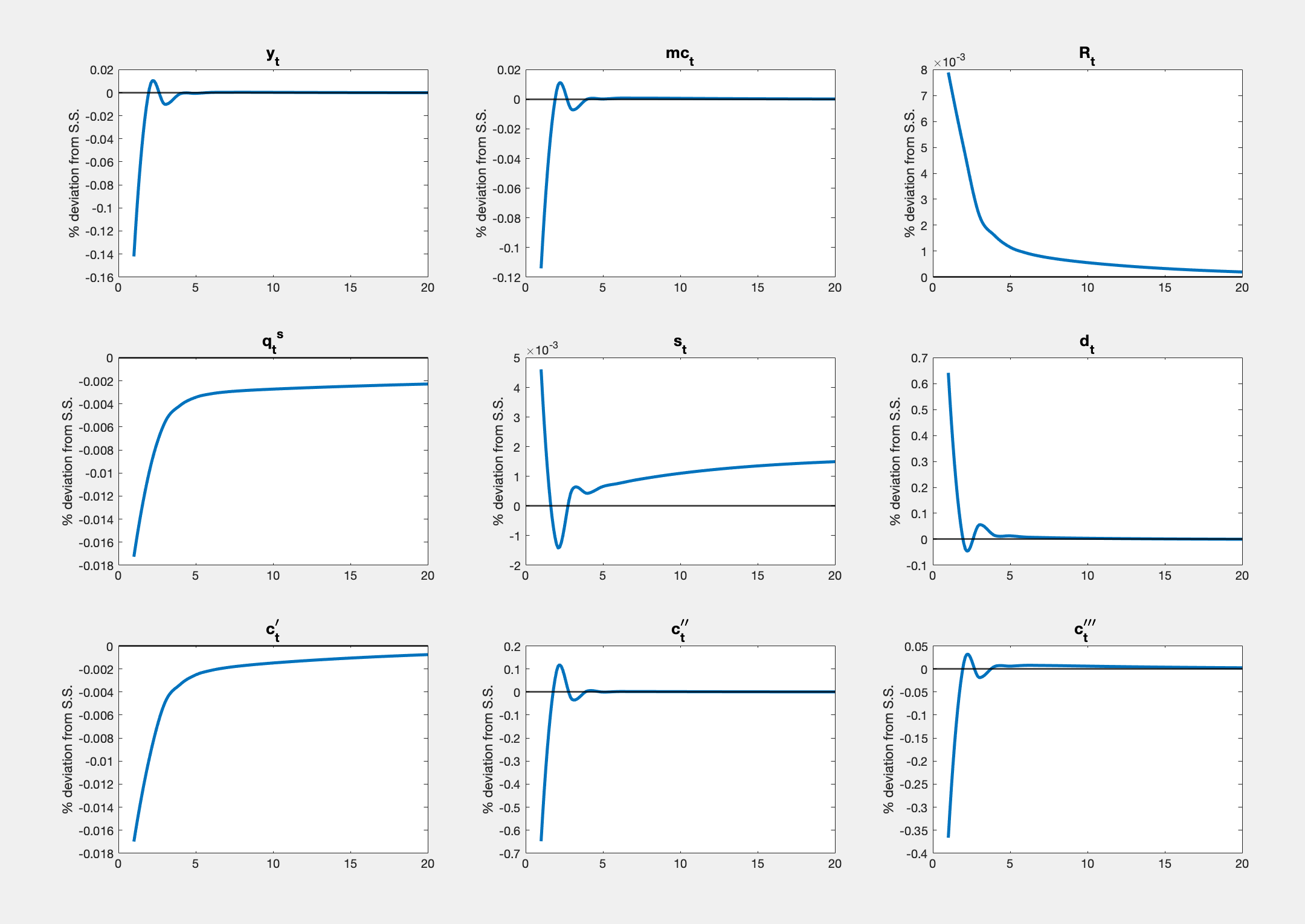

I construct a DSGE model with three types of households to observe the impact of interest rate changes on individual households consumption, where R is the interest rate. I log-linearize the model and use dynare for Bayesian estimation, and the posterior IRFs are shown in the figure.

Some variables regress slowly to steady state, while others regress quickly to steady state in the second period and produce a small fluctuation.

Why does my posterior IRFs look like this? Is there any way to fix it?

Thanks.