Hello everyone, I’ve been recently replicating the GK-2011 paper and encountered some confusion when dealing with nominal interest rates and interest rate rules.In his paper, the nominal interest rate is net,

i_t=(1-\rho)\left[\frac{1-\beta}{\beta}+\kappa_\pi \pi_t+\kappa_y\left(\log Y_t-\log Y_t^*\right)\right]+\rho i_{t-1}+\varepsilon_t\\

1+i_t=R_{t+1} \frac{E_t P_{t+1}}{P_t}

If we define $i_t$ is gross nominal interest rate , then

i_t=(1-\rho)\left[\frac{1}{\beta}+\kappa_\pi \pi_t+\kappa_y\left(\log Y_t-\log Y_t^*\right)\right]+\rho i_{t-1}+\varepsilon_t\\

i_t=R_{t+1} \frac{E_t P_{t+1}}{P_t}

If we further define i_t as log gross nominal interest rate, then

e^{i_t}=(1-\rho)\left[\frac{1}{\beta}+\kappa_\pi e^{\pi_t}+\kappa_y\left( Y_t- Y_t^*\right)\right]+\rho e^{i_{t-1}}+\varepsilon_t\\

e^{i_t}=e^{R_{t+1}} e^{\pi_{t+1}}

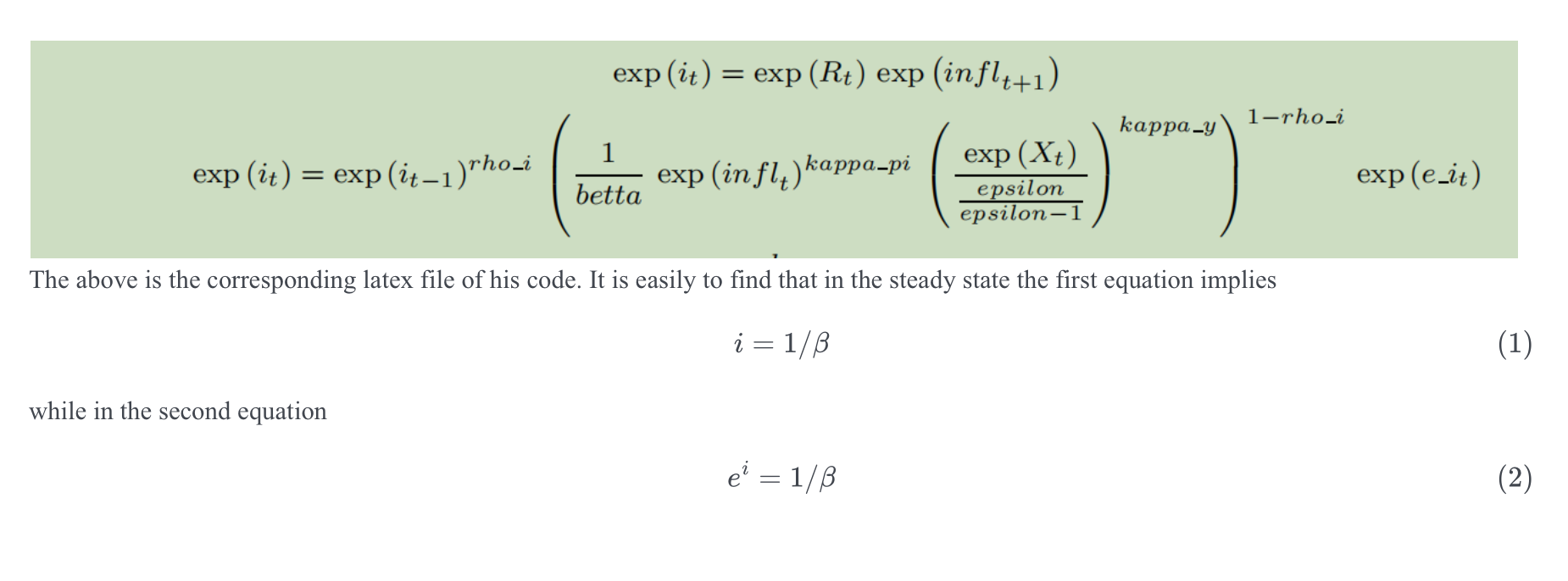

However, it is not same with the interest rule in his FA.mod file. Actually, I think in his mod file the definition of i_t is different between these equations, where in interest rule i_t is gross nominal interest rate and in fisher equation it is log gross nominal interest rate.

Thanks in advance!