Dear sir,

I am estimating my model but encountering a problem as ‘Log data density is -Inf.’ I have looked up the related topics to find the possible reason to cause that problem,but my problem may be a little bit different from what i found in those topics.I have some question about this problem.Hope I can get your

kindly help.

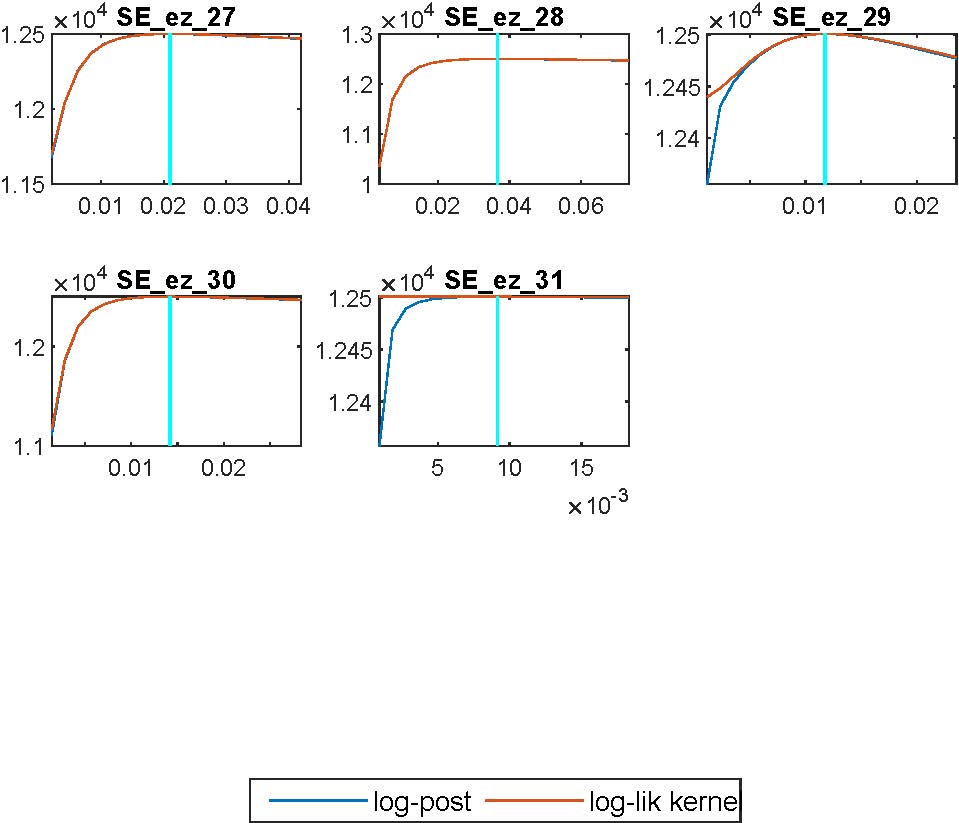

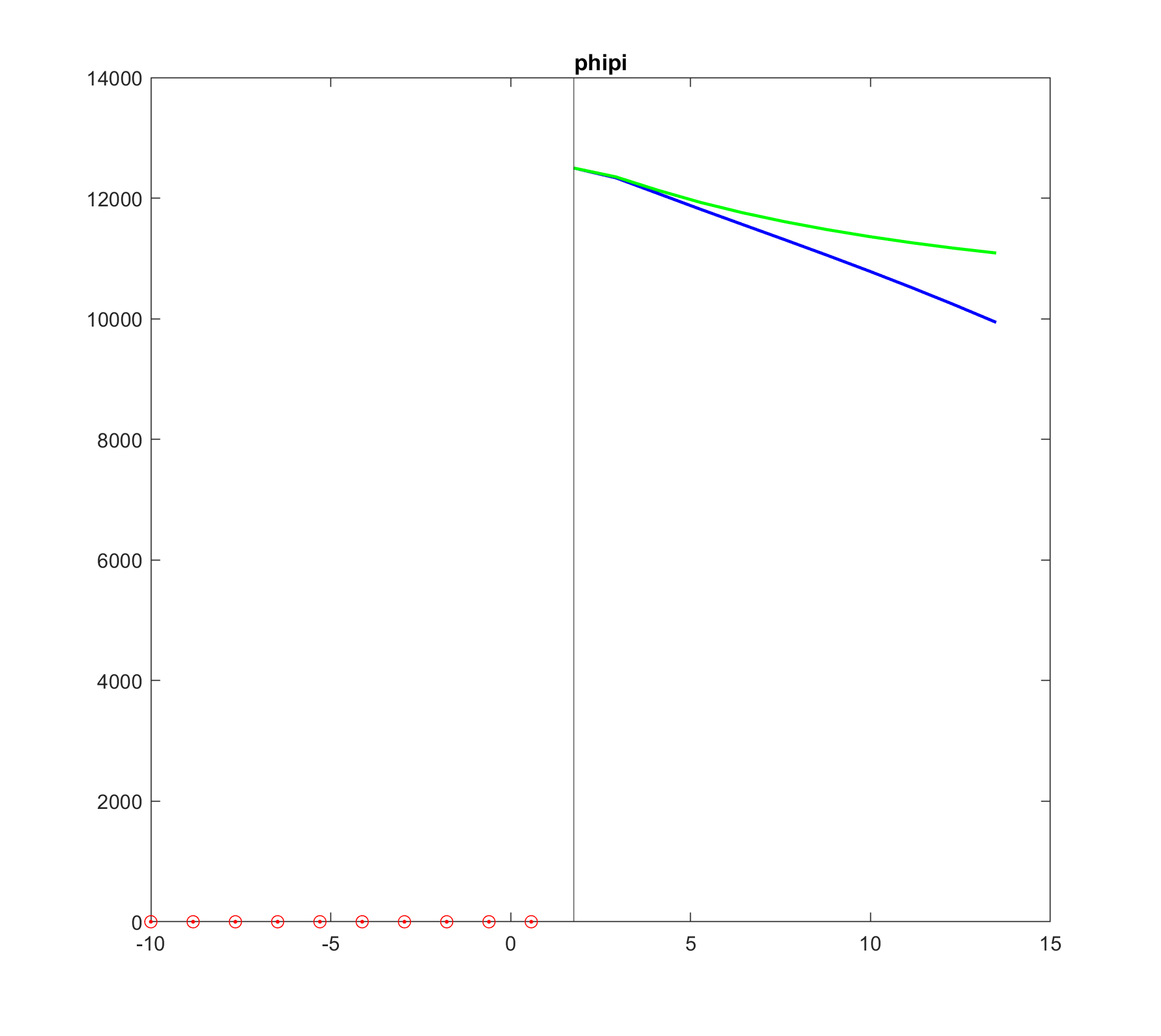

The plots I attached indicate that the prior distribution of ez_31 contributes no information.The coefficient of inflation and total output in taylor rule seem very close to the boundary to instability.My observation euqations include nominal interest rate and sectoral comsumption growth.Before estimation,I ran the identification command and made sure that all the parameters in my model are identified.Is this caused by data problem? and will it cause the infinity of log data-density?(Sorry about the phipi plot, the original graph is lost and i plot it myself using check_plot_data)

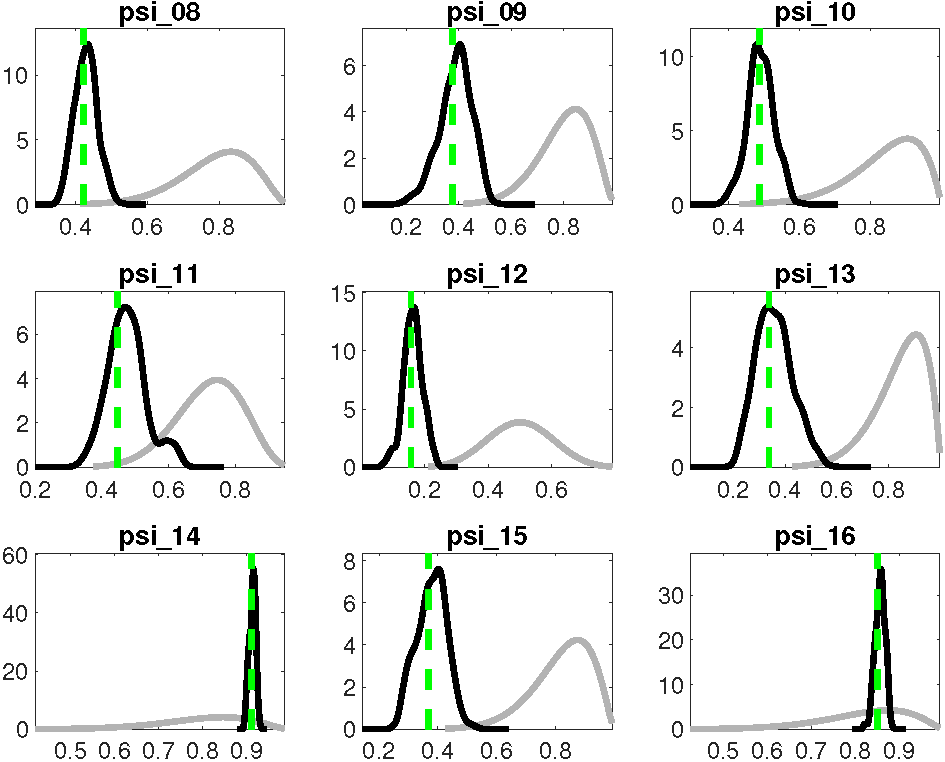

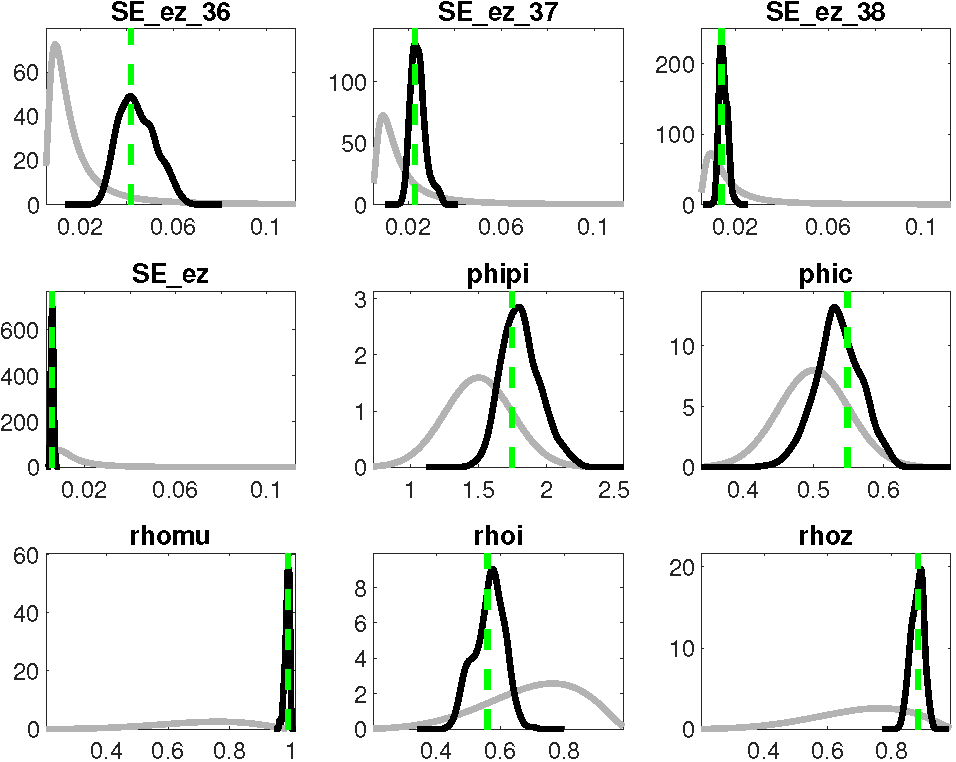

2.Looking at the Prior-Posterior plot,i find that in some graphs,the vertical green line is not at the mode of posterior distribution.I first used the mode_compute =4 to obtain the mode and used another optimizer (mode_compute=7) starting from the mode obtained in the last procedure to find the global mode.Is this problem caused by small number of replic of MCMC chains(20000)? or should I continue using different optimizer to find mode ? I tried to use mode_compute=9 but it didn’t work .Running fminsearch after csminwel didn’t make any change.

The error message is listed below:

Estimation::mcmc: Number of mh files: 1 per block.

Estimation::mcmc: Total number of generated files: 2.

Estimation::mcmc: Total number of iterations: 20000.

Estimation::mcmc: Current acceptance ratio per chain:

Chain 1: 21.03%

Chain 2: 22.02%

Estimation::mcmc: Total number of MH draws per chain: 20000.

Estimation::mcmc: Total number of generated MH files: 1.

Estimation::mcmc: I’ll use mh-files 1 to 1.

Estimation::mcmc: In MH-file number 1 I’ll start at line 10001.

Estimation::mcmc: Finally I keep 10000 draws per chain.

Estimation::marginal density: I’m computing the posterior mean and covariance… Done!

Estimation::marginal density: I’m computing the posterior log marginal density (modified harmonic mean)…

Estimation::marginal density: The support of the weighting density function is not large enough…

Estimation::marginal density: I increase the variance of this distribution.

Estimation::marginal density: Let me try again.

Estimation::marginal density: There’s probably a problem with the modified harmonic mean estimator.

ESTIMATION RESULTS

Log data density is -Inf.

I attached my mod file here.My model is very large so estimation will be very time-consuming.

I thank you in advance for your help.

jason