I am trying to replicate the paper Aoki Benigno Kiyotaki (2016) Monetary and Financial Policies in Emerging

Markets. My code works properly, but the impulse curves do not coincide with those in the paper (screen attached). Above this, the impulse curves for one of the shocks are not curves but rather short straight lines (attached).

What could be the problem? I checked many times that all equations are OK.

Thank you a lot.

If someone has a similar problem, it works when the order of approximation is set to 1 and all variables are replaced with exp(x) instead of x to linearize the model (do not forget to log the steady-state values).

If you don’t use higher order with pruning, the exp()-substitution inducing a loglinearization instead of linearization may actually help to prevent explosive simulations.

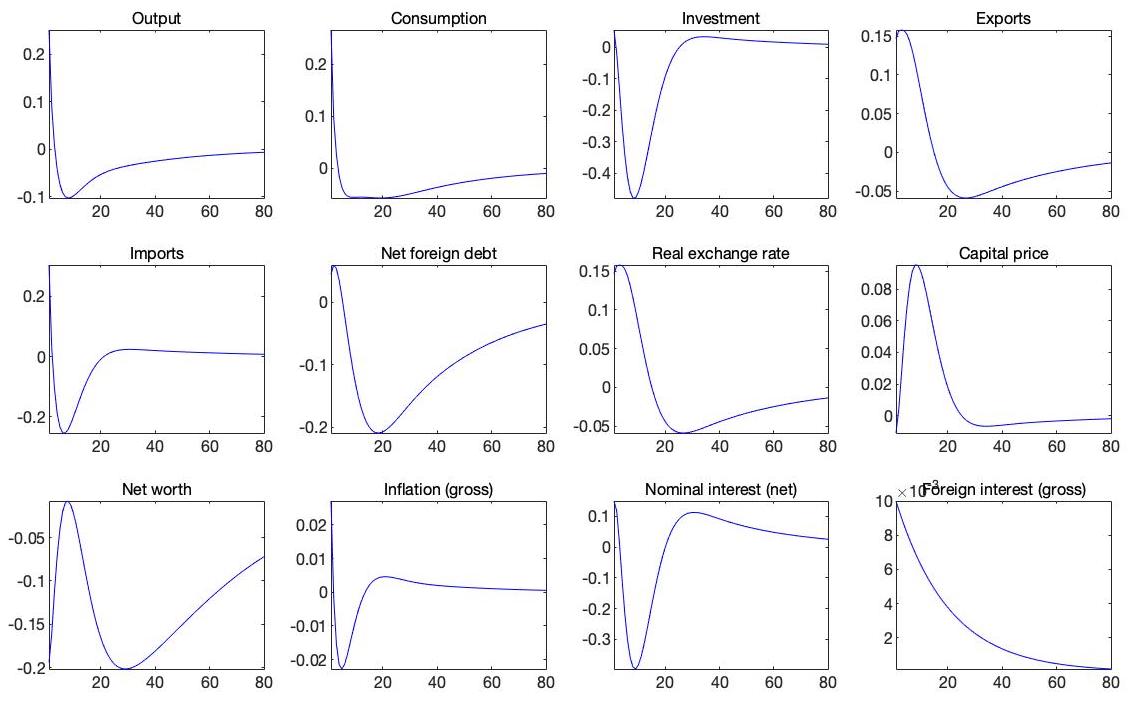

Apologies in advance for bumping this old topic, but I had a couple questions about the replication of ABK (2016) as well.

For most of the variables I get well behaved IRFs, but I’m struggling to replicate the IRFs of the [domestic] nominal interest rate as in the paper. In the 2018 version of the ABK paper, the nominal interest rate responds in a hump-shaped pattern. However, I’m getting an initial drop in the nominal interest rate for the first 20 periods, before seeing a small increase.

I suspect there’s an issue with my interpretation of the Fisher equation, or the steady state net nominal interest rate.

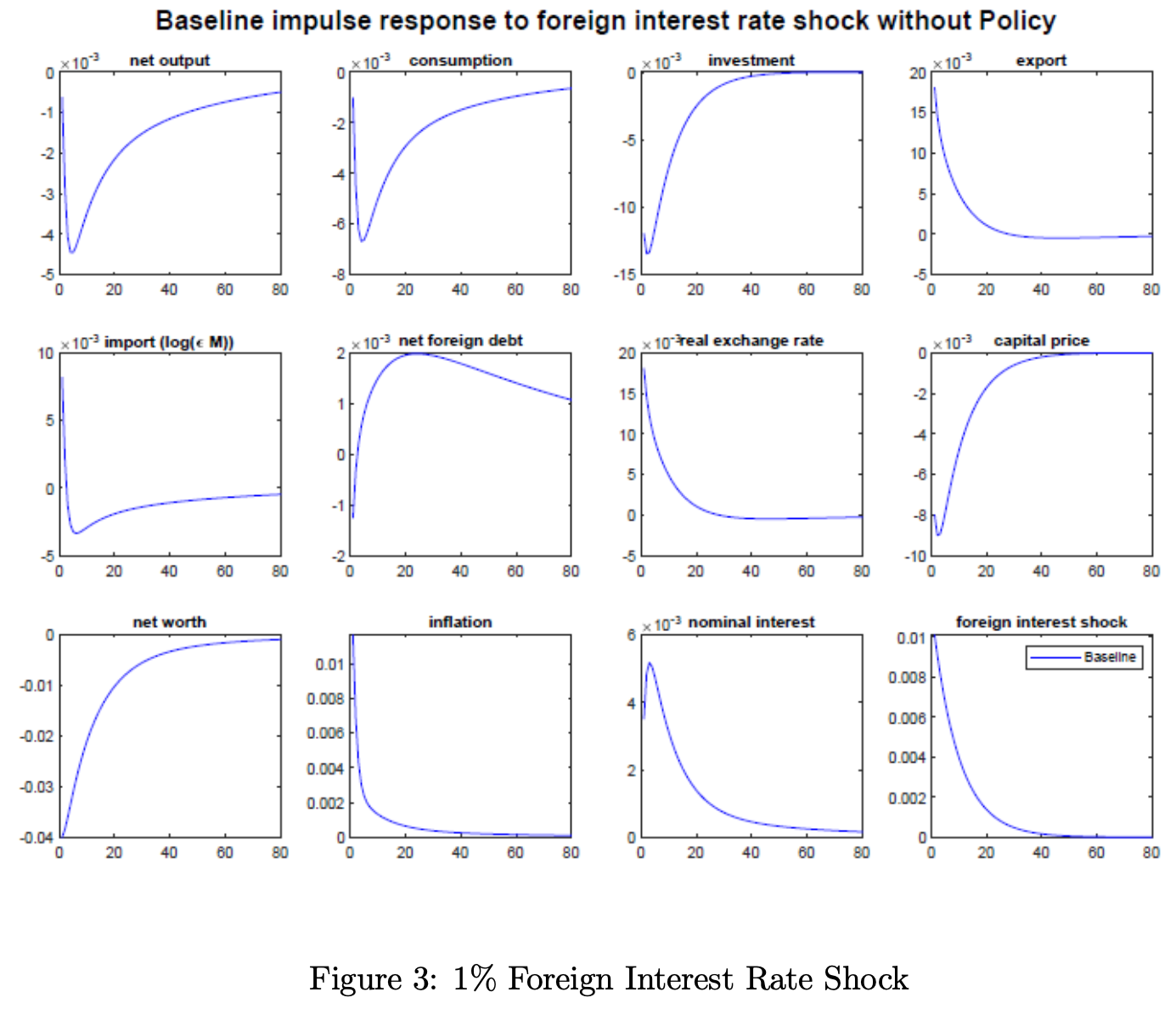

I just wanted to provide an update: I managed to replicate the results in the ABK paper, and would like to share the code on here – I’ve noticed quite a lot of people on the net struggling with this paper, so hopefully this helps.

Note that this only covers the baseline foreign interest rate shock experiment (figure 3 in the ABK paper).

{kind=link}