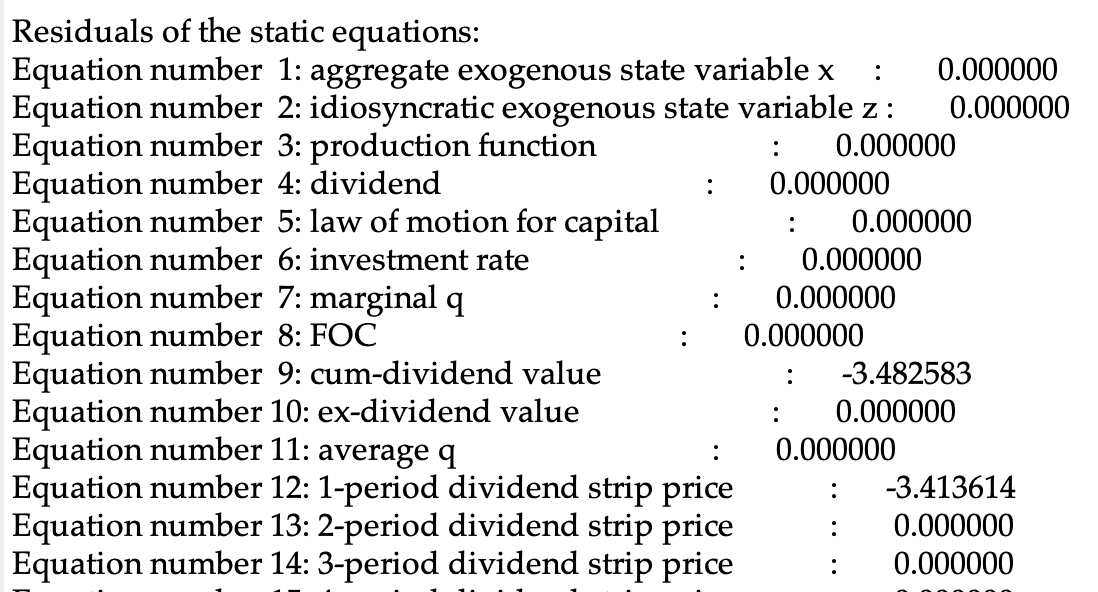

seems like the following works:

[name='1-period dividend strip price']

vd1 = exp(m)*d(+1);

[name='2-period dividend strip price']

vd2 = exp(m)*vd1(+1);

[name='3-period dividend strip price']

vd3 = exp(m)*vd2(+1);

seems like the following works:

[name='1-period dividend strip price']

vd1 = exp(m)*d(+1);

[name='2-period dividend strip price']

vd2 = exp(m)*vd1(+1);

[name='3-period dividend strip price']

vd3 = exp(m)*vd2(+1);