Hi everyone,

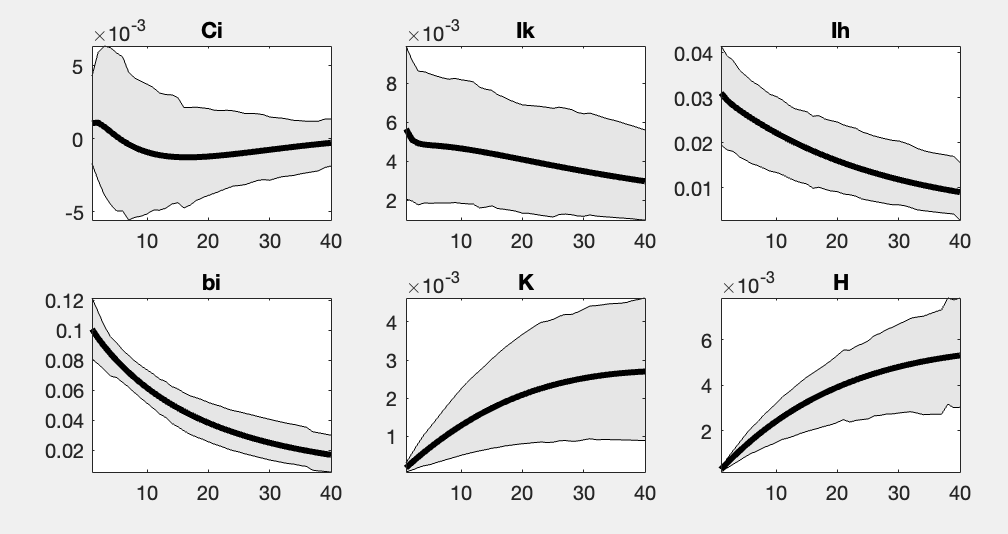

I am estimating a DSGE model using Bayesian methods, and I find that for some variables (for example, Ci in the attached figure), the impulse response function (IRF) often crosses the zero axis — meaning that the 90% credible interval includes zero for most horizons.

I have two questions:

- Interpretation of statistical significance In this case, should I conclude that the response of Ci to the shock is statistically insignificant?Or, in Bayesian IRFs, is it acceptable to give an economic interpretation even if the credible interval includes zero?Are there any common rules of thumb for deciding whether a Bayesian IRF is “significant”?

- Why many papers do not report Bayesian IRFs.I notice that many DSGE papers, even those using Bayesian estimation, only report point-estimate IRFs (often based on the posterior mode) without showing the posterior distribution bands.Does this mean that their results might be less robust ( the credible intervals could cross zero)?Or are there other academic reasons for this choice, such as journal space constraints or tradition?

I attach an example figure (IRF ) for reference.

thanks!