Hello,

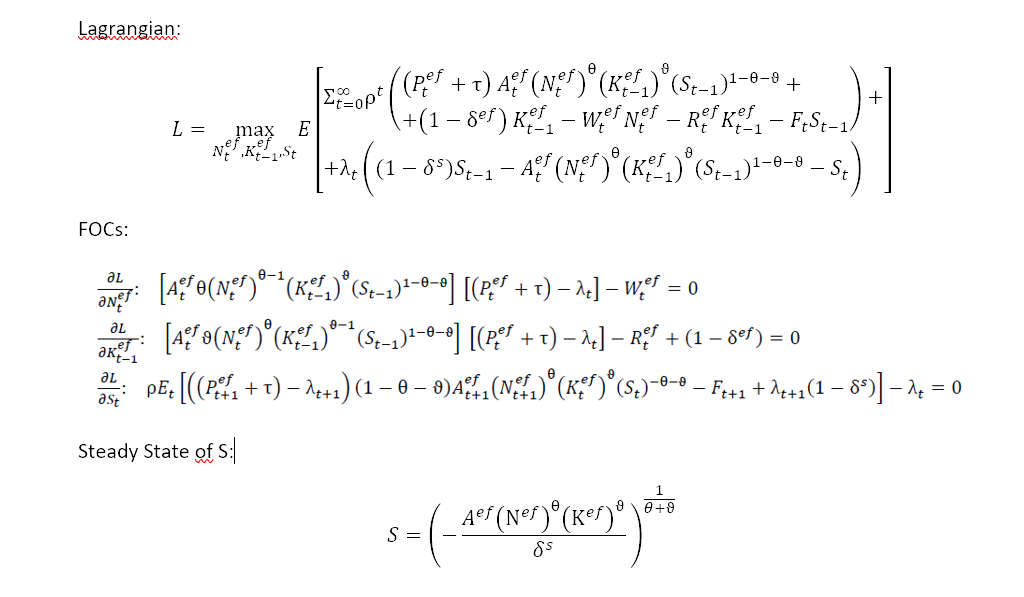

I am trying to replicate a paper that estimates a DSGE model about renewable energy policies. The model contains four types of firms, one of those produces energy from a non-renewable fossil fuels stock. See the Lagrangian of the firm in the image at the end.

Where the equation multiplied with lambda is a constraint, that says that future resources are the depreciated past resources less the energy production. The FOCs are also depicted in the image at the end. The constraint is omitted there.

Eliminating lamda allows for the first two FOCs to be combined neatly, but when eliminating lambda in the third equation, this yields a long additive equation with expectations.

I tried two things:

a) Put the model in levels into dynare and trying to solve for the steady state. However, quickly it dawned on me, that if I try to get the steady state of S, the constraint yields an imaginary number (see last part of image below).

b) I was advised to log-linearize the model, such that all steady state variables are zero, but then for such additive equations, still many orignial steady state values are required. The next advice was then to calibrate these steady state values instead of computing the steady state.

My first question is, given the steady state equation for the stock of non-renewable resources, can the model still work while containing such an equation? Maybe with a restriction that the stock may only drop to zero?

If it can, how do I implement this in dynare? Do I take additional steps such that the steady state becomes computable or do I indeed calibrate the steady state values?

Any help would be greatly appreciated.