Dear all, I have the following equation

, but do not know how to express it in dynare. Is there anyone could help me. Thanks.

That is a nonstationary model. I would need more context what you are trying to achieve.

Hi, if your model includes terms like \alpha^t, you can rewrite it recursively by introducing an endogenous state variable, say a, defined as:

The general solution to this geometric sequence is a_0\alpha^t, so you only need to choose an initial condition such that a_0=1 (i.e. not the steady state). But

If |\alpha|<1 the sequence converges to zero, which may cause issues for your steady state.

If |\alpha|>1 then, your model is nonstationary. Unless you use the Dynare interface to associate trends to the endogenous variables, you will have to stationarize the model yourself and in the process the terms like \alpha^t should vanish.

Best,

Stéphane

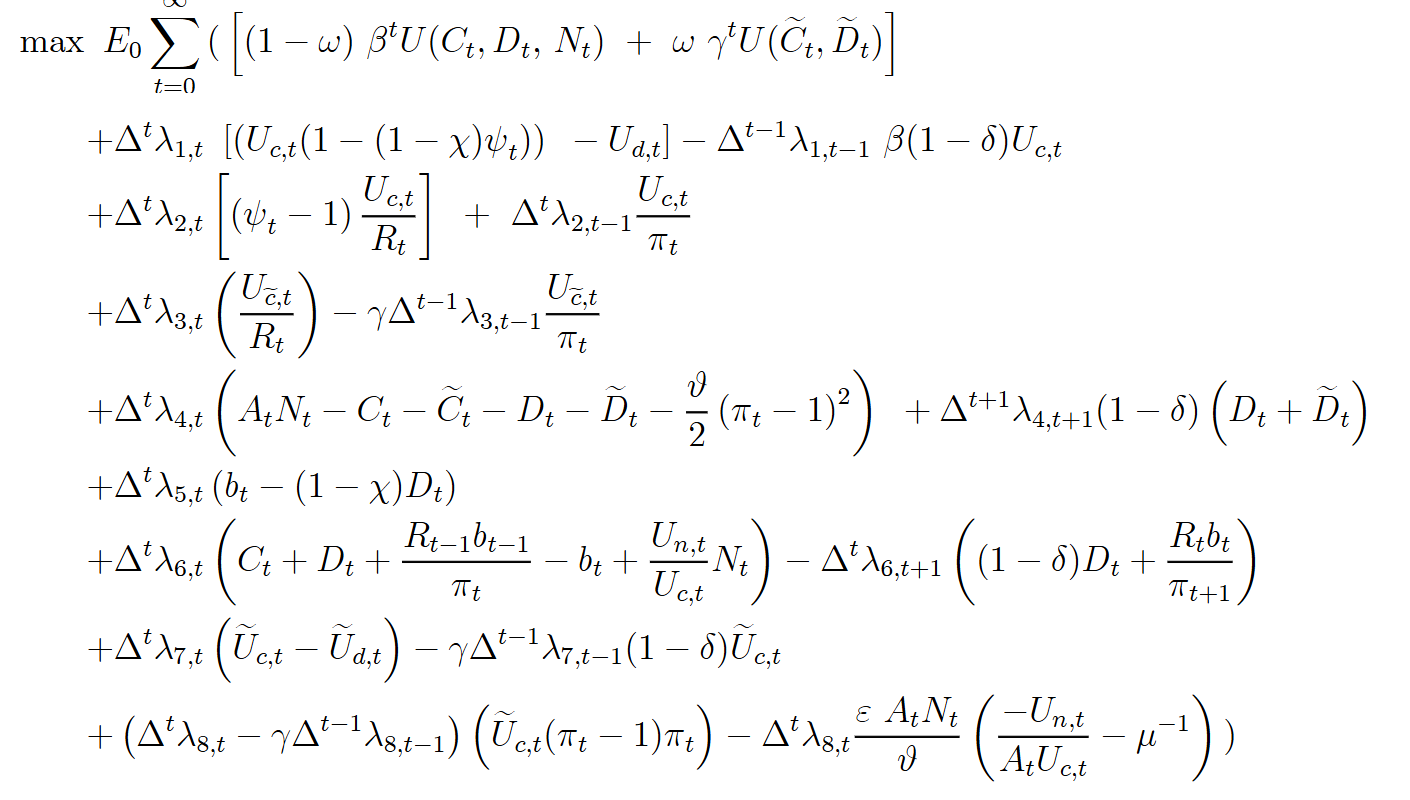

Dear Pfeifer and Stepan, thanks for your replies. Recently, I am reading Monacelli’s paper “Optimal Monetary Policy with Collateralized Household Debt and Borrowing Constraints”(Optimal Monetary Policy with Collateralized Household Debt and Borrowing Constraints | NBER).

The discount factors for households are different, \beta is for borrowr, and \gamma for saver, \gamma>\beta.

The objective for Ramsey Problem is given by

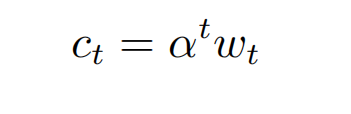

I am not sure I am following. The model would not be well-defined if you really end up with

c_t=\alpha^tw_t if \alpha is a constant. You almost always end up with a recursive formulation that is stationary.