Dear all,

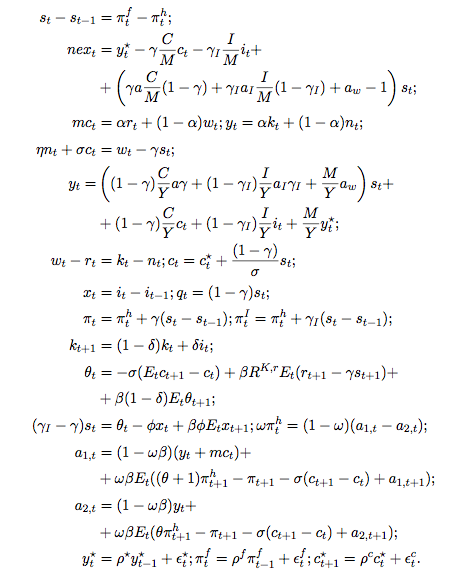

I just started using Dynare for my master thesis where I need to replicate the model of the paper “ OVERVALUED: SWEDISH MONETARY POLICY IN THE 1930s ” (for a small open economy,). In the appendix, the authors show the equilibrium equations for the level model and the log linear one. I decided to use the log-linear model equations and tried to compute the steady state (First I try to calibrate my model using the authors parameters values in order to see how it performs, later on I will estimate my own parameters). I am however confused at that point. I am not sure exactly how I should compute it. In the log-linear model, there are some variables that are at the steady state level (Y,M,I,C,R) and I am not sure exactly how I have to deal with it. I read many discussions in this forum but I am still unsure/ confused about what I should do.

Should I create a steady_state.m file with the level model equations ? Or should I implement the level model inside a model block ? Can anyone help me here?

I attach the thesis.mod file (where I started implementing my model) and the log-lin model of the paper I try to replicate.

Thank you in advance.

thesis.mod (2.1 KB)